Cottonseed and U.S. Oilseed Farm Program Issues

This article describes and assesses the proposal to add cottonseed to the list of “other oilseeds.” The proposal is important due to its potential cost and because it raises other issues, including the generic base program and other oilseed program. These issues are also discussed.

Data Sources

Prices and yields are from U.S. Department of Agriculture (USDA), National Agricultural Statistics Service: QuickStats; and USDA, Office of the Chief Economist: January 2015 World Agriculture Supply and Demand Estimates. Crop program data are from USDA, Farm Service Agency (FSA): ARC/PLC Program and ARC/PLC Program Data, and Price Support Reports.

Background – Cottonseed Proposal

In response to the elimination of direct payments and to Brazil’s successful challenge of the U.S. cotton program at the World Trade Organization (WTO), the cotton program in the 2014 farm bill was based on: (1) crop insurance, including a county insurance program with an 80% subsidy enacted only for cotton and commonly known by its acronym STAX, (2) marketing assistance loans for upland cotton and (3) transition direct payments for the 2014 crop (2015 crop if STAX was unavailable). Insurance protects against losses that occur during a single year’s production period while marketing loans, which date to the 1985 farm bill for cotton, protect against low prices on production. Marketing loan benefits and loan deficiency payments for upland cotton total $372 million for the 2014 crop and over $150 million for the 2015 crop to date. Payments can also be received from ARC (Agriculture Risk Coverage) or PLC (Price Loss Coverage) if a program crop is planted on former upland cotton base (now called “generic base”) and if that crop is due a payment. Many cotton producers are calling for additional assistance against the broad, multiple year decline in crop prices that began after the 2012 drought. A proposal has emerged asking the Secretary of Agriculture to designate cottonseed, a co-product with cotton fiber, as an “other oilseed.” The Secretary was first given this authority in the 1990 farm bill, conditional upon receiving a request. The only oilseed making a request at this time is cottonseed. As a point of reference, for the 2014 crop cottonseed accounted for 16% of the value and 57% of the pounds of cottonseed plus cotton fiber the U.S. produced.

Background – “Other Oilseed” Program

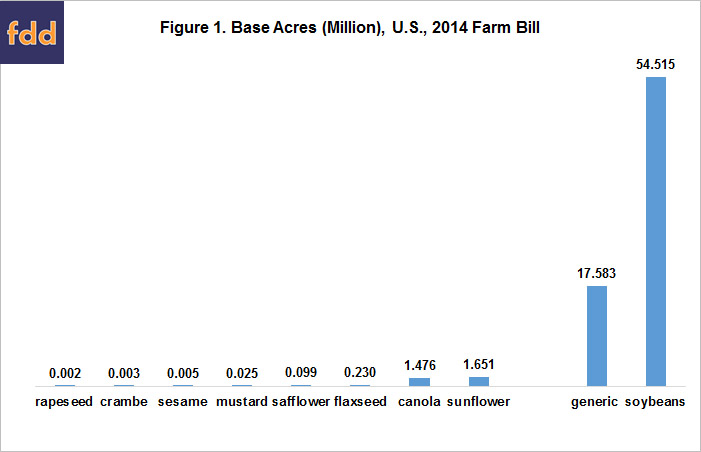

“Other oilseeds” are covered program commodities and eligible for ARC/PLC. They currently are canola, crambe, flaxseed, mustard, rapeseed, safflower, sesame, and sunflowers. Their collective program base totals 3.5 million acres, with 47% and 42% in sunflowers and canola (see Figure 1). Nearly 75% of “other oilseed” base was elected into PLC (see Figure 2). The PLC share ranges from 44% for rapeseed to 97% for canola. In comparison, PLC was elected for only 3% of the 54.5 million base acres of soybeans (see Figures 1 and 2).

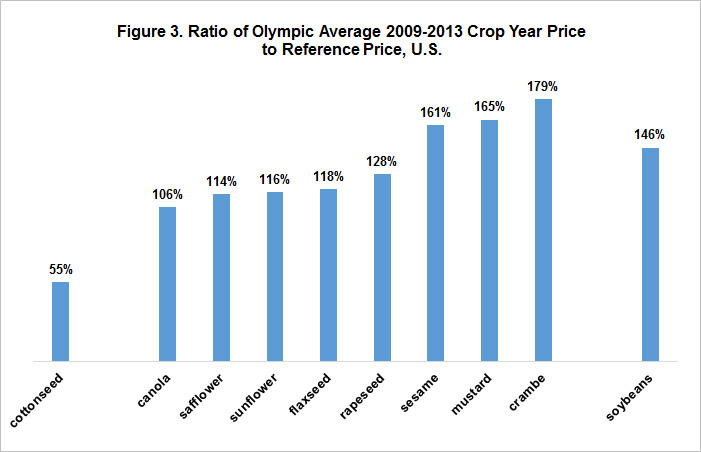

All “other oilseeds” have the same reference price: $0.2015/pound. The relationship of this reference price to market price, however, varies by crop. For example, the ratio the Olympic average price for the 2009-2013 crop years to the “other oilseed” reference price varies from 106% for canola to 179% for crambe (see Figure 3). This large variation between different market prices and a common reference price implies payments by PLC will likely vary among the “other oilseeds.” Canola is the most likely recipient–which explains its 97% participation rate in PLC. Based on data posted December 6, 2015 for the 2014 crop year, canola accounts for 78% of all payments made to the “other oilseeds” by ARC-CO (ARC – county) and PLC, far above its 42% share of “other oilseed” base acres.

Cottonseed Proposal and “Other Oilseed” Program

The price of cottonseed is well below the “other oilseed” reference price, as illustrated for the 2009-2013 crop years in Figure 3. PLC payments for cottonseed could approach $1 billion per year if made on current cotton (generic) base acres. [for example for the 2014 crop year, “other oilseed” reference price of $0.2015/pound minus 2014 crop year cottonseed U.S. average price of $0.0970/pound) times 85% times cotton (generic) base acres of 17.6 million times U.S. cottonseed program yield of 824 pounds/acre calculated using 2014 farm bill procedures]. In comparison, using 2014 farm bill procedures and the same program parameters, ARC-CO payments are estimated to be $0.2 billion, largely because of its 10% cap on per acre payment. PLC thus would likely be elected for most base acres if the Secretary adds cottonseed to the list of “other oilseeds.” Lower payments would occur if a smaller base acreage number was used.

Background – Generic Base Acres

In addition to eliminating the direct and countercyclical programs and not authorizing ARC or PLC for cotton fiber, the 2014 farm bill converted 17.6 million acres of cotton program base acres to generic base acres. These acres receive ARC/PLC payments based on the program crop planted on the FSA farm with generic base acres and on the program elected for the crop. Thus, for generic base, planting decisions are not decoupled from program payments and hence can be affected by expected program payments.

Cottonseed Proposal and Generic Base Acres

If the Secretary adds cottonseed to “other oilseeds” and since the price of cottonseed is well below the “other oilseed” reference price, PLC payments to cottonseed seem likely. The cottonseed payment could be implemented in a number of ways including as a cottonseed payment for generic base planted to cotton or as a cottonseed payment on base acres decoupled from planting decision. Cottonseed planted on generic base acres, as assumed in the above calculation, would seem to be the most straight-forward. The statute provides for the creation of decoupled base acres but little information is available as to how that would work considering that historically those acres were cotton acres and they are currently generic base acres. Additional analysis of the decoupled base acre approach would require more implementing details.

Because generic base planted to a program crop receives payments to that crop from the elected program, the existence of the cottonseed payment could influence planting decisions with more cotton acres planted as a result. Moreover, concern has emerged that the generic base program has encouraged the planting of other program crops, notably peanuts. Another policy question therefore is whether adding cottonseed to “other oilseeds” will discourage crops other than cotton from being planted on generic base? Since it is well established in economics that prices are determined by changes at the margin, to the extent the generic base program encourages the planting of program crops, the resulting lower prices could be increasing farm program payments. Thus, adding cottonseed to “other oilseeds” may reduce the incentive to plant program crops other than cotton on generic base, thus reducing government payments to other program crops and providing an offset for at least some of the cost of any cottonseed payments.

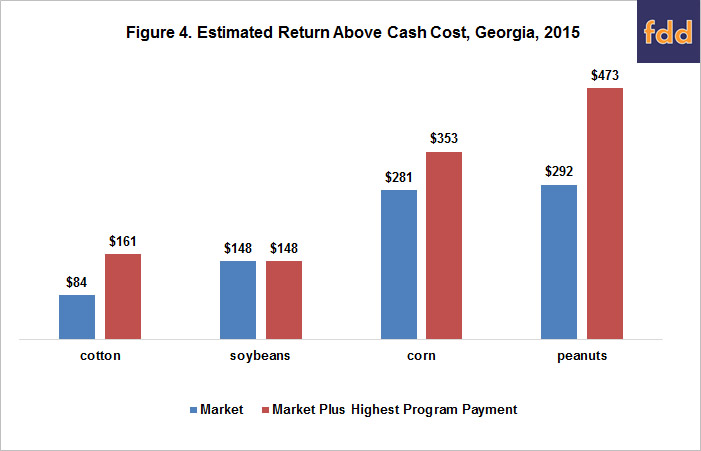

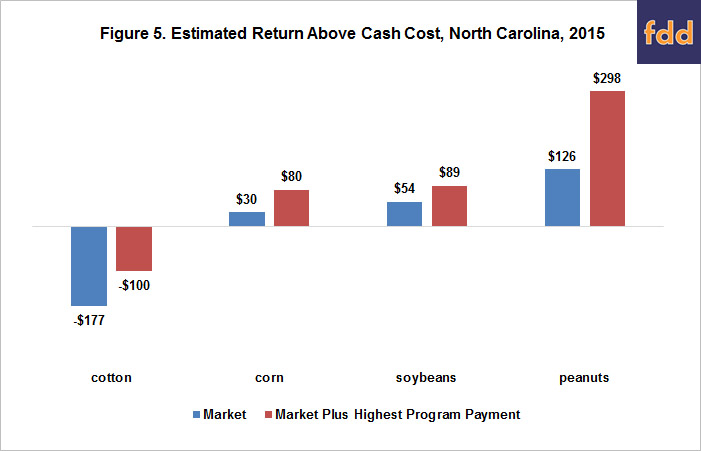

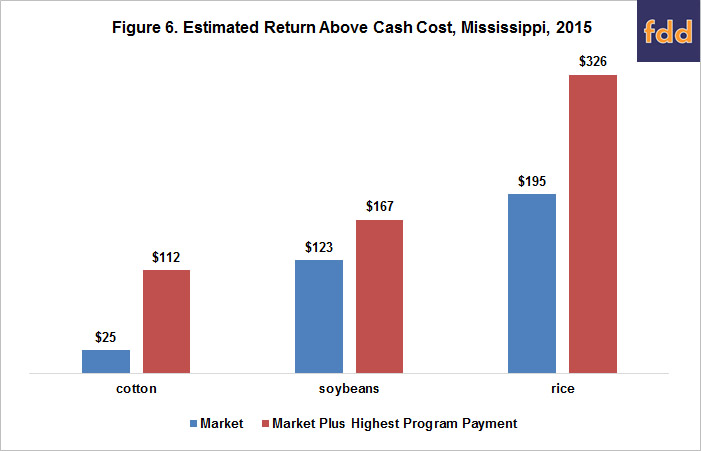

To provide one perspective on these questions, return above cash cost is estimated for selected 2015 crops in the states of Georgia, Mississippi, and North Carolina. Mississippi and Georgia have the second (1.62 million) and third (1.46 million) most generic base acres (after Texas, 7.2 million). Georgia is the largest producer of peanuts, accounting for approximately half of U.S. production. Mississippi is a large producer of long grain rice. Along with peanuts, long grain rice received per acre PLC payments for the 2014 crop that exceeded $100 per acre for many states. North Carolina is a notable producer of corn and soybeans and is located in a different part of the U.S. South. The data used are estimates of 2015 yields per planted acre based on the January 2016 USDA Crop Production report, prices reported so far for the 2015 crop year adjusted to the state level using recent state-U.S. price ratios, program parameters from FSA or estimated based on available USDA data, and cash cost of production from the USDA, Economic Research Cost of Production website for the Southern Seaboard region for Georgia and North Carolina and the Mississippi River Delta or Mississippi Portal region for Mississippi. Cash costs are available for the 2014 crop year and include operating costs, such as seed and fertilizer, plus hired labor, taxes, and insurance. The selected crops are those for which cost of production data are compiled by USDA for the region. While many factors influence planting decisions, including rotational concerns and access to specialized equipment needed for a crop; returns above cash and total cost are useful indicators of future increases or decreases in planted acres.

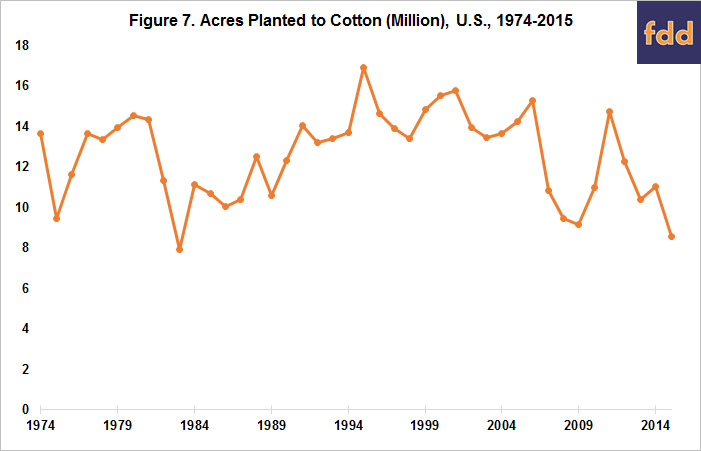

Figures 4, 5, and 6 contain the results for Georgia, North Carolina, and Mississippi, respectively. When examined as a group, the figures suggest that cotton has the lowest return from the market of the crops examined. This finding is consistent with the post-2012 decline in cotton acres, but the decline has longer standing, starting with the 2007 crop (see Figure 7). Adding payments by the cottonseed program as well as the highest projected 2015 program payments for the other crops changed the ranking of cotton only for Georgia and only for soybeans (see Figure 4). Last, cotton’s return, even with the cottonseed payment, remained well below that of peanuts in both Georgia and North Carolina. Using total cost of production did not change these findings. It is also worth noting that return above total cost, including estimated 2015 program payments, exceeded zero for Georgia corn and peanuts and Mississippi long grain rice. The return above total cost was also just negative for North Carolina peanuts (-$5/acre). A positive return above total cost is usually viewed as an incentive to expand acres.

Summary Observations

- Adding cottonseed to the “other oilseed” program is an important proposal because of its potential cost and because it underscores the existence of related policy issues.

- The large potential cost of adding cottonseed to “other oilseeds” raises issues of how to pay for it and what share should cotton bear? For example, should the generic base program be altered?

- The cottonseed payment could be implemented in a number of ways including as a cottonseed payment for generic base planted to cotton and as a cottonseed payment on base acres decoupled from planting decisions. Additional information is needed to analyze the latter approach. For the former approach, while planting decisions are influenced by many factors, a simple analysis for Georgia, North Carolina, and Mississippi suggests the cottonseed payment would not alter planting incentives for generic base acres in most situations and in particular the incentive to plant peanuts on generic base. However, economic conditions could change and cottonseed payments could influence planting decisions.

- The decline in U.S. cotton acres since 2006 raises the issues of’ its competitiveness within the world market for cotton and among alternative crops within the U.S. Considerable disagreement exists on these issues. In this context, it is worth noting that, despite access to farm programs, U.S. acres planted to barley, oats, sorghum, and wheat declined respectively: -59%, -82%, -52%, and -23% from the 1974 to 2015 crop years. For cotton, the decline was -37%.

- Using a common reference price for the “other oilseeds” when market price varies notably across them means that not only potentially cottonseed but also some of the current “other oilseeds,” notably canola, benefit more than others from PLC.

- The disparity noted in the preceding bullet point can be addressed by differentially setting the reference prices for oilseeds using a given ratio of reference price to historical or current market price. A follow-on question is whether the same ratio should apply to soybeans? Both changes would require action by Congress.

- Another issue involves the STAX insurance program for upland cotton. STAX is similar to but also differs in important details to the Supplemental Coverage insurance Option (SCO) that is available to other crop acres in PLC. For example, the subsidy rate is 80% for STAX versus 65% for SCO and the highest coverage level is 90% for STAX versus 86% for SCO. Is it fair that cotton should have access to STAX while other PLC crop acres have access to SCO? Changes to cotton’s access to STAX would likely require action by Congress.

- Last and potentially most importantly, it is not clear how other countries will respond if cottonseed is added to “other oilseeds,” especially when spending by the U.S. on farm programs is increasing and already viewed as high by many countries. This concern likely grows the more spending on U.S. cotton increases above the 2014 farm bill baseline. A WTO case could target not just cotton but the PLC-generic acre program, and perhaps even ARC since the fixed reference price is part of its payment formula and a producer with generic base can elect ARC.

References

USDA, World Agricultural Outlook Board. World Agricultural Supply and Demand Estimates, WASDE-549. Released January 12, 2016. http://usda.mannlib.cornell.edu/usda/waob/wasde//2010s/2016/wasde-01-12-2016.pdf.

USDA/FSA. ARC/PLC Program. http://www.fsa.usda.gov/programs-and-services/arcplc_program/index.

USDA/FSA. Price Support Reports. http://www.fsa.usda.gov/programs-and-services/price-support/price-support-reports/index.

USDA/NASS. QuickStats. http://quickstats.nass.usda.gov/.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.