Farm Machinery Costs and Custom Rates

Numerous farms that are either hiring a custom operator or providing custom rate services to other farms use published custom rate surveys. Though this information is very useful when establishing custom rates, it is prudent to compare your farm machinery costs per acre to custom rates. If your machinery cost per acre is relatively high, then a farm should consider using a custom operator rather than replacing their own machine. Similarly, if a farm is providing custom rate services and has a higher cost than the published survey rates, it either needs to charge more or try to figure out how to lower costs per acre. This article compares machinery costs per acre for a case farm to custom rates associated with a field cultivation operation and a self-propelled sprayer operation.

Machinery Cost Computation

Several cost items should be included when computing total machinery costs per hour and per acre. It is common to divide farm machinery costs into two categories: annual ownership costs and annual operating costs. Ownership costs include depreciation, interest, and insurance and housing. Operating costs include repairs and maintenance, fuel, lubrication, and labor.

Depreciation results from wear, obsolescence, and machine age. Here, we are talking about economic depreciation rather than tax depreciation. Depreciation for tax purposes is often accelerated compared to economic depreciation. To compute economic depreciation, information pertaining to economic useful life, list price, and salvage value are needed. Economic useful life is not necessarily the same as service life. Many farms trade machines before they are completely worn out. Salvage value is an estimate of the sale value of the machine at the end of the economic useful life. Interest should be included in ownership costs regardless of whether debt is incurred when purchasing a machine. Interest represents the opportunity cost associated with using scarce funds to purchase a machine.

Repair and maintenance costs for a particular machine can vary substantially among farms. It is best to use a farm’s actual repair records to estimate these costs. If this level of detail is not available, it is common to use annual hours of use and machine age to estimate repair and maintenance costs. Labor cost reflect machine time, time required to lubricate and service machines, and travel time. When comparing total machinery costs to custom hire charges, it is particularly important to include labor costs.

Several data sources were used to create the two examples below. First, a case farm in north central Indiana with 3000 acre of corn and soybeans was assumed. Acres farmed, annual hours, useful life, and interest rate represent those of the case farm. Second, purchase prices, insurance and housing, and repair costs were adapted using information contained in Edwards (2015) and Lattz and Schnitkey (2017a; 2017b). Third, custom rate comparisons were derived from Langemeier (2017) and Plastina and Johanns (2017).

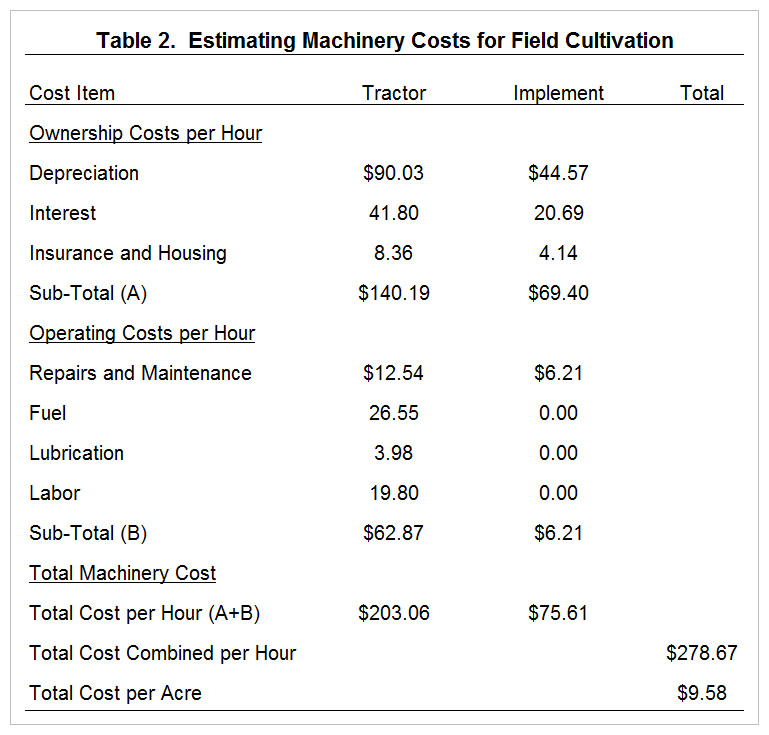

Field Cultivation

Tables 1 and 2 present machinery costs for a field cultivation operation on the case farm. Table 1 illustrates the computation of depreciation, interest, insurance and housing, and repairs. Salvage values for the tractor and implement were assumed to 30 percent of the purchase prices. The computations of interest, insurance and housing, and repair costs assumed that the tractor and implement had one-half of their useful life left. Interest, insurance and housing, and repair cost rates were assumed to be 5 percent, 1 percent, and 1.5 percent, respectively. These costs are heavily dependent on annual hours of use and useful life. If annual hours of use or the useful life were lower, the cost rates for interest, insurance and housing, and repairs would be higher.

The information in table 1 was used to help compute the total machinery costs for field cultivation on the case farm in table 2. In addition to the costs outlined in table 1, the costs in table 2 include fuel, lubrication, and labor costs. Fuel costs are based on a $2.25 per gallon price for diesel fuel. The total costs per hour for the tractor and implement were estimated to be $203.06 and $75.61 for a total combined cost per hour of $278.67. According to Lattz and Schnitkey (2017b), the field cultivator represented in tables 1 and 2 can cover 29.1 acres per hour. Using this information, the total machinery cost per acre was $9.58.

Langemeier (2017) and Plastina and Johanns (2017) indicate that the custom rate for field cultivating is approximately $12.75 to $15.25 per acre. The total machinery cost per acre ($9.58 per acre) for the case farm is under these custom rates, indicating that it is economical for the case farm to own a field cultivator. It is important to note that other factors such as timeliness, liquidity, solvency, and tax management may affect a farm’s decision to own machines or custom hire certain field operations.

Self-Propelled Sprayer

Tables 3 and 4 present machinery costs for a self-propelled sprayer operation on the case farm. Table 3 illustrates the computation of depreciation, interest, insurance and housing, and repairs. The salvage value for the self-propelled sprayer is assumed to be 30 percent of the purchase price. The computations of interest, insurance and housing, and repair costs assumed that the self-propelled sprayer had one-half of its useful life left. Interest, insurance and housing, and repair cost rates were assumed to be 5 percent, 1 percent, and 3 percent, respectively. These cost rates are dependent on annual hours of use and useful life. If annual hours of use or useful life were lower, the cost rates for interest, insurance and housing, and repairs would be higher.

The information in table 3 was used to help compute the total machinery costs for spraying on the case farm reported in table 4. In addition to the costs outlined in table 3, the costs in table 4 include fuel, lubrication, and labor costs. Fuel costs are based on a $2.25 per gallon price for diesel fuel. The total cost per hour for the self-propelled sprayer is estimated to be $314.57. According to Lattz and Schnitkey (2017b), a self-propelled sprayer can cover 80.6 acres per hour. Using this information the total machinery per acre was $3.90.

Langemeier (2017) and Plastina and Johanns (2017) indicate that the custom rate for using a self-propelled sprayer is approximately $6.70 to $7.65 per acre. The total machinery cost per acre ($3.90) for the case farm is under these custom rates, indicating that it is economical for the case farm to own a self-propelled sprayer. Again, other factors such as timeliness, liquidity, solvency, and tax management affect a farm’s decision to own the sprayer or use a custom operator to spray the farm’s crops.

Conclusions

Farms that use custom operators or provide custom operations to other farms need to compare machinery costs per acre with published custom rate survey values. This article outlined the conceptual framework needed to estimate machinery costs per acre. Examples pertaining to field cultivation and a self-propelled sprayer were used to illustrate the conceptual framework.

It is important to note that machinery costs per acre vary widely among farms. Thus, it is imperative that farms compute their own machinery costs per acre when making comparisons with custom rate survey data.

References

Edwards, William. "Estimating Farm Machinery Costs." Iowa State University Extension and Outreach, Ag Decision Maker, A3-29, May 2015.

Langemeier, Michael. 2017 Indiana Farm Custom Rates." Purdue University, Center for Commercial Agriculture, May 2017.

Lattz, Dale and Gary Schnitkey. "Machinery Cost Estimates: Field Operations." University of Illinois Extension, Farm Business Management, June 2017 (a).

Lattz, Dale and Gary Schnitkey. "Machinery Cost Estimates: Tractors." University of Illinois Extension, Farm Business Management, June 2017 (b).

Plastina, Alejandro and Ann Johanns. "2017 Iowa Farm Custom Rate Survey." Iowa State University Extension and Outreach, Ag Decision Maker, A3-10, March 2017.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.