Farmer Balance Sheets Given Farmland Price Decreases

In the 1980s, farmland price decreases contributing to farm financial stress. Today, some concern exists that farmland price decreases could cause financial stress in the next several years. While large price decreases would cause large net worth reductions, it is unlikely that farmland price decreases in and of themselves will lead to solvency problems on most farms. However, continuing negative cash flows from operations could lead to financial difficulties. A balance sheet of a typical grain farmer in Illinois is used to illustrate impacts of farmland price decreases and continuing losses from operations.

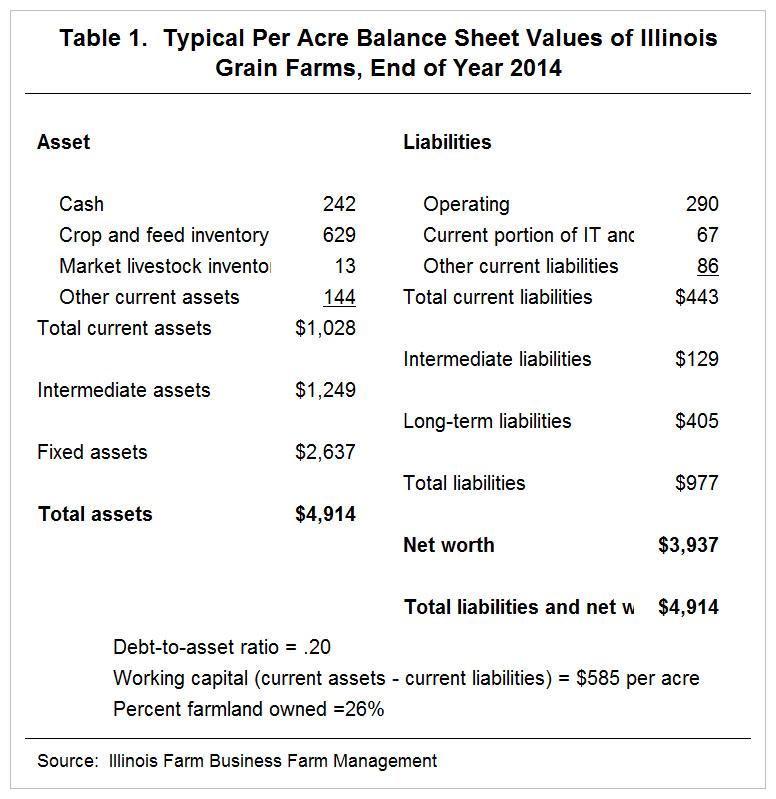

Typical Grain Farm Balance Sheet

Table 1 shows a typical balance sheet for an Illinois grain farmer, with values stated on a per acre basis. This balance sheet would be for a well-established farmer. Beginning farmers likely will have more debt relative to assets, less working capital, and fewer acres owned. Items to note on the balance sheet are:

- Total current assets equal $1,028 per acre. On grain farms, crop inventories account for $629 per acre, representing 61% of current assets. The next largest item is cash, totaling $242 per acre. Over time, cash has increased from $95 per acre in 2003 up to $317 per acre at the end of 2012. Cash balances have declined in each of the last two years. Other current assets of $144 per acre include projected government payments and prepaid expenses.

- Intermediate assets total $1,249 per acre. Major items in intermediate assets are machinery inventories and retirement accounts.

- Fixed assets average $2,637 per acre. Fixed assets are predominately farmland, with the remainder including buildings. The average percent acres owned for the average shown in Table 1 is 26%. That is, there is .26 owned acre for each tillable acres. Fixed asset values will increase with higher percent acres owned, and vice versa.

- Total liabilities equal $977 per acre, giving a debt-to-asset ratio of .20 ($977 of total liabilities divided by $4,914 of total assets). Over time, the average debt-to-asset ratio has decreased from an average of .30 in 2001 and 2002.

Overall, the balance sheet of the typical farmer is strong. Total assets are $4,914 per acre, liabilities are $977 per acre, and net worth is $3,937 per acre.

Farmland Price Reductions

One concern is that farmland prices will decrease, leading to reductions in net worth, and perhaps solvency problems on grain farms. As is discussed in an October 20th article, the concerns of impending farmland price decreases may be misplaced. However, even if large farmland price decreases occur, typical farmers in Illinois will be solvent.

Take the balance sheet in Table 1 and suppose that fixed assets decreased in value by 50%. This decline simulates a farmland price decrease of 50%. A 50% price decrease would be larger than the 42% price decrease that occurred in average Illinois farmland values between 1981 and 1987 in the midst of the 1980s farm crisis. A 50% decrease would result in the following balance sheet changes:

- Total current

- Fixed assets would fall from $2,637 per acre to $1,319 per acre, a decrease of $1,318 per acre.

- Total assets would fall from $4,914 per acre to $3,596 per acre, a decrease of $1,318 per acre.

- Net worth would fall from $3,937 per acre to $2,619 per acre, again a decrease of $1,318 per acre.

- Debt-to-asset ratio would increase from .20 to .25.

Obviously, this price decline would have profoundly negative impacts, reducing net worth by one-third. However, this typical farm still would be solvent with a .26 debt-to-asset ratio. A .25 debt-to-asset ratio is less than the average debt-to-asset ratio of .30 during the early 2000s.

Somewhat ironically, those farms more vulnerable in today’s economic environment are less vulnerable to farmland price changes. Those farmers renting over 90% of the farmland are most vulnerable (see farmdoc daily October 29, 2013). Since these farmers own less of their farmland, a farmland price decrease will have less of an impact on their net worth and solvency positions.

Working Capital Reductions

The financial concern in today’s environment is negative cash flows, leading to reductions in working capital. Cash flow reductions will vary across farms, depending on the financial and business structure of farms. Estimates of typical reduction are (see farmdoc daily October 6, 2015):

- -$11 per acre for owned farmland

- -$121 per acre for cash rented farmland, and

- -$72 per acre for share rented farmland.

If the farm in Table 1 has 26% of its acres owned, 37% cash rented, and 37% share rented, the farm would have a cash shortfall of -$74 per acre. Working capital would be reduced from $585 per acre down to $511 per acre ($585 per acre working capital at the end of 2014 less $74 working capital reduction).

From a financial standpoint, this farm could absorb this loss and continue operations without much change for another year or two. At some point though, working capital will run out, at which point there may be a desire to refinance debt, moving some short-term debt to longer-term debt, thereby providing more working capital. This refinancing will not solve the cash shortfall problem, as the problem is that costs exceed revenue. This shortfall issue will continue until either commodity prices increase or costs decrease. Even if corn prices increase to the mid-$4.00 price range, cost still need to be cut (see farmdoc daily October 13, 2015). Reducing costs by $100 per acre seem prudent (see farmdoc daily September 1, 2015 and farmdoc daily August 4, 2015).

The balance sheet and discussion above concentrates on a well-established grain farm. There will be farms whose balance sheet will deteriorate faster than that presented above. Those farms will tend to have a higher proportion of their farmland cash rented.

Summary

Large farmland price decreases would reduce net worth, but would not necessarily lead to solvency issues. The larger threat for most farms is dealing with reducing costs so that costs do not exceed expected revenues.

References

Schnitkey, G., B. Sherrick, and T. Kuethe. "2016 Farmland Price Outlook." farmdoc daily (5):194, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 20, 2015.

Schnitkey, G. "Taking Losses on Cash Rent Farmland to Avoid Losing Farmland: A Risky Strategy." farmdoc daily (5):189, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 13, 2015.

Schnitkey, G. "Significant Reductions in Working Capital Likely in 2015 on Grain Farms." farmdoc daily (5):184, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 6, 2015.

Schnitkey, G. "Cutting $100 per Acre in Costs for Corn and Soybeans." farmdoc daily (5):160, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, September 1, 2015.

Schnitkey, G. "Cost Cutting for 2016: Budgeting for $4 Corn and $9.25 Soybeans." farmdoc daily (5):141, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, August 4, 2015.

Schnitkey, G. "Proportion of Farms with High Cash Rent Percentages and Levels." farmdoc daily (3):206, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 29, 2013.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.