Declining Real Cash Cost of Producing Corn, Soybean, and Wheat: Historical Perspective and Potential Implications for the Future

In the June 4, 2015 farmdoc daily article, “Current Corn, Soybean, and Wheat Prices in Long Term Perspective,” (Zulauf, 2015) I wrote that “While historical trends do not always hold, absent strong arguments to the contrary, the default position is that real U.S. crop prices are likely to trend lower. More succinctly, unless general price inflation increases, supply growth declines, or multiple year global supply disruptions occur; the question is not if but when will corn crop year average price average below $3 and push toward $2.” This article extends this examination by looking at the trends in real cash cost per acre of producing corn, soybeans, and wheat since 1975, the first year cost data for the U.S. are available. This cost declined for each of the three crops until the period of farm prosperity began in 2006. Declining real cash costs both cushions the decline in real prices by mitigating its impact on profit margins but also furthers the decline in real prices by mitigating the incentive to reduce supply.

Data: Cost of production and yield are from the U.S. Department of Agriculture, Economic Research Service “Commodity Cost and Return” data. Data exist for the 1975-2014 crop years. A major change in methodology occurred in the late 1990s. Cash costs were reported prior to but not after this change. Cash costs after the change are calculated by adding to operating costs, the cost of hired labor, taxes and insurance, and general farm overhead. Cash costs per bushel are divided, i.e. deflated, by the GDP implicit deflator, which is considered to be the most accurate measure of inflation for a country. Source for the GDP deflator is the FRED data set maintained by the Federal Reserve Bank of St. Louis. The GDP deflator is indexed to its 2014 value.

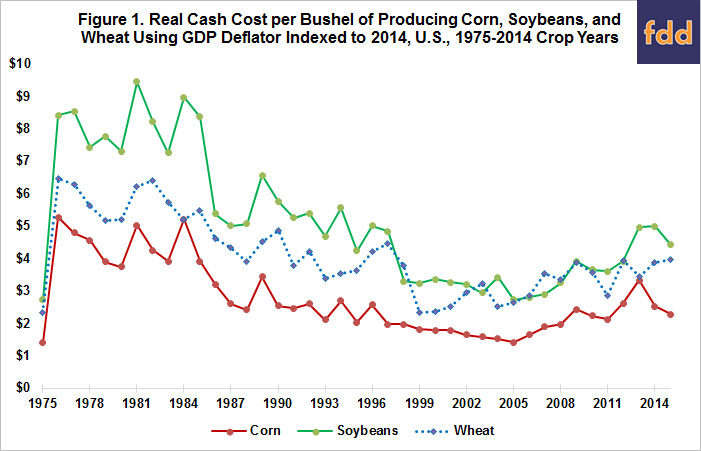

Findings: Corn had the lowest real, i.e. deflated, cash cost per bushel throughout the observation period. In most years, soybeans had the highest real cash cost per bushel. The time path is similar for the three crops. Per bushel real cash cost is highest early in the observation period, declines until the start of the recent period of farm prosperity, then climbs upward. Despite the recent uptrend, real cash cost per bushel is lower now than in the late 1970s. Comparing 2010-2014 with 1975-1979, real cash cost per bushel is 42%, 44%, and 37% lower for corn, soybeans, and wheat, respectively. Because the cash cost per bushel is higher for soybeans and because the percent declines are roughly the same for all three crops, the difference in real cash cost per bushel between soybeans and the other two crops has narrowed by around $1.50 per bushel.

Figure 2 compares average annual percent change in real cash cost per bushel during the periods of decline and increase. Because yields vary, 5 year averages are computed for 1975-1979, 2001-2005, and 2010-2014. Average annual change is then computed using the middle year of each period. During the period of decline, average annual change was similar across the crops, varying from a decline of 1.9% for wheat to a decline of 2.4% for corn. Average annual change differed more during the period of increasing real cost. Annual increase averaged 2 percentage points higher for corn than for soybeans, which in turn averaged nearly 2 percentage points higher than for wheat.

Changes in real cash cost per bushel reflect changes in both real cash cost per acre (Figure 3) and yield per planted acre (Figure 4). Real cash cost per acre decreased during 1977-2003, with the annual percent decrease similar across the crops. Real cash cost per acre increased during 2003-2012, with the percent increase greater for corn than soybeans and especially wheat. The larger percent increase in real cash cost per acre for corn and soybeans during 2003-2012 was reinforced by their slower growth in yield, especially for corn, both relative to 1977-2003 and relative to wheat during 2003-2012. In contrast, during 1977-2003, yield growth favored corn and soybeans.

Summary Observations

Real cash cost of producing a bushel of corn, soybeans, and wheat is lower now than during the late 1970s, even with the increase during the recent period of farm prosperity.

Examination of real cash cost during the period of prosperity lifts up the role of a factor not often discussed about this period, the relatively slow growth in U.S. corn and soybean yields. The slow growth put upward pressure on crop prices and returns, then on input prices and cash cost of production. While it is possible that long term yield growth has slowed, this observation most likely underscores the importance of deviations from long term yield trends that can last several years.

As noted in the June 4, 2015 farmdoc daily article, historical trends may not hold but do suggest a default position absent strong arguments to the contrary. Specifically, history suggests real per bushel U.S. cash cost of producing corn, soybeans, and wheat is likely to trend lower in the future.

Moreover, changes in input prices lag changes in crop output prices (Zulauf and Retting, September 17, 2015). Thus, the sizable decline in crop prices since 2012 is likely to lead to lower input prices and thus cash costs.

In addition, the decline in natural gas prices, both in real and current dollars, (Irwin, November 13, 2015) is likely to put downward pressure on farm input prices, especially nitrogen fertilizer prices.

Lower per bushel cash cost of production allows crop price to decline even more since the lower cost dampens the supply response to lower price. Moreover, if cash costs per bushel decline faster than crop price, supply will expand, further reducing prices, everything else constant.

In a period of declining real prices, a key managerial objective is to reduce real cash cost of production faster than real price declines. The historical evidence in this study suggests a managerial goal of reducing real cash cost per bushel by 2% per year on average, or approximately the decline observed between 1977 and 2003. If prices do not decline, then achieving this goal will leave the farm in even better shape.

In an era of low general economic inflation, such as the current era; the per bushel cash cost of production in current dollars can decline. Thus, the preceding managerial goal would be slightly restated as, decrease current dollar cash cost per bushel by 2% per year.

CAVEAT: This article is not a forecast for near term crop year prices and costs, including 2015/2016. Short term factors, such as weather aberrations both in the U.S. and around the world, can override long term trends. However, long term trends determine the currents in which short term factors operate. Effective management starts with understanding and continually monitoring the longer term currents.

References

Irwin, S. "The Real Price of Natural Gas." farmdoc daily (5):212, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 13, 2015.

St. Louis Federal Reserve, Gross Domestic Product: Implicit Price Deflator. Released October 29, 2015. https://research.stlouisfed.org/fred2/series/GDPDEF

USDA/ERS, Commodity Cost and Return. Released October 1, 2015. http://www.ers.usda.gov/data-products/commodity-costs-and-returns.aspx

Zulauf, C. "Current Corn, Soybean, and Wheat Prices in Long Term Perspective" farmdoc daily (5):103, Department of Agricultural, Environmental and Development Economics, The Ohio State University, June 4, 2015.

Zulauf, C., and N. Rettig. "Have U.S. Farm Input Prices Followed U.S. Crop Prices?" farmdoc daily (5):171, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, September 17, 2015.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.