The Biofuels Era – A Changing of the Guard?

The increase in corn used for ethanol has been a major driver of crop prices in the New Era that began in the Fall of 2006. In the face of one of the worst droughts of the last century this summer, there have been numerous calls to limit the policy incentives to use corn for ethanol production in the upcoming year. The U.S. Environmental Protection Agency (EPA) is currently considering formal requests for this potential relief. While ethanol has garnered nearly all of the headlines in recent years, its role as the leading driver of crop prices may be nearing an end.

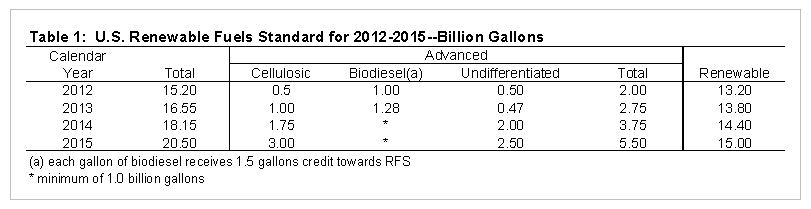

The Renewable Fuels Standards (RFS) established in 2005 and amended in The Energy Independence and Security Act of 2007 plays a central role in this story. Those amended standards are summarized in Table 1 in three categories: Total, Advanced, and Renewable. The renewable standard has been and will likely continue to be met almost entirely by corn-based ethanol. This (implied) standard increases from 13.2 billion gallons in 2012 to 15 billion gallons in 2015, suggesting the need for increasing amounts of corn to meet the standard. However, the actual amount of ethanol production over the next several years depends on a number of inter-related factors. Those factors include the way in which the advanced standards are met; the magnitude of discretionary blending (if any), particularly for bio-diesel; the magnitude of U.S ethanol imports; the size of the export market for U.S. ethanol; the magnitude of the blend wall for ethanol; the use of accumulated blending credits (banked RINS) to meet the RFS; and whether or not the RFS is amended.

We begin our analysis by tracing out the implications for biofuels consumption over the next three years based on one potential scenario involving all of the listed factors. This scenario represents our assessment of the most likely path of these factors. We limit the analysis to the four year period 2012-2015 in order to make the exercise manageable. The expectations and assumptions include:

- The current RFS for total advanced or renewable biofuels will not be amended over the next three years (no waiver in 2013),

- Cellulosic requirements will continue to be written down to be effectively zero each year,

- The minimum biodiesel requirement will remain at 1.28 billion gallons over 2013-2015,

- Each gallon of biodiesel blended receives a credit of 1.5 gallons towards the RFS,

- No discretionary blending of advanced biofuels, and

- Imported Brazilian ethanol is a cheaper way to meet discretionary advanced blending requirements than with biodiesel, but is limited to 830 million gallons per year.

The last assumption is based on current price relationships that suggest that biodiesel blending is uneconomic and will be blended only to the extent required to meet the advanced RFS. The availability of Brazilian ethanol for import is an open question. Annual imports over the past six years have ranged from 16 million gallons in 2010 when high sugar prices limited Brazilian ethanol production to 731 million gallons in 2006 when the U.S. was transitioning away from the use of MTBEs. Availability is dependent on the magnitude of Brazilian production, demand from other importers, and internal policies affecting domestic consumption. Imports are on track to reach 500 million gallons this year. The assumption of 830 million gallons of imports appears to be a realistic cap, but deviations from that amount do not substantially impact this analysis.

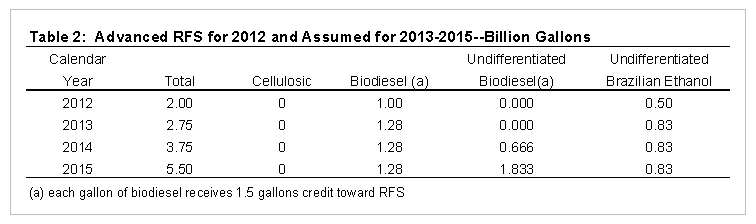

The net effect of these assumptions on the advanced component of the RFS is shown in Table 2. Notice that the combination of 1.28 billion gallons of biodiesel (already proposed by the EPA) and 830 million gallons of imported Brazilian ethanol is assumed to be sufficient to meet the advanced component in 2013. These two numbers add up to 2.75 billion gallons because, as noted earlier, one gallon of biodiesel is equal to 1.5 gallons of ethanol in terms of complying with the RFS ([1.28 X 1.5 = 1.92] + 0.83 = 2.75). With the assumed cap of 830 million gallons of Brazilian ethanol imports, biodiesel production ramps up sharply from 1.28 billion gallons in 2013 to 3.113 billion gallons in 2015. This is the only way the advanced component can be met under these assumptions if the EPA does not write down the total advanced component of the RFS.

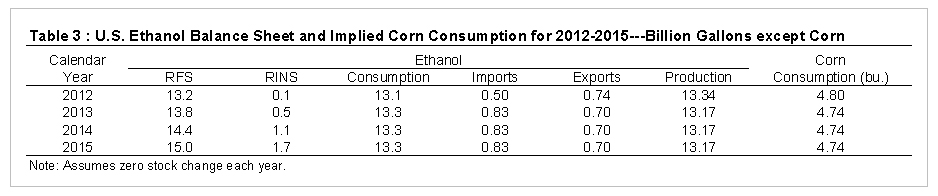

Table 3 extends the analysis to domestic ethanol production and corn consumption over 2012-2015 based on the additional assumptions:

- The ethanol “blend wall” is 13.3 billion gallons per year,

- Ethanol blending margins are favorable and insure that the market demand for ethanol in the U.S. is at least 13.3 billion gallons

- The maximum amount of Brazilian ethanol is imported each year,

- Banked RINS are used only when the RFS for renewable biofuels exceeds the blend wall, and

- Ethanol exports total 700 million gallons per year.

The assumption of a constant blend wall of 13.3 billion gallons is based on the expectation that total U.S. fuel consumption will continue to moderate and that implementation of E-15 will continue to proceed slowly. The actual blend wall could obviously deviate from 13.3 billion gallons, but the implications for ethanol production and corn consumption are straight-forward and easily calculated. Ethanol exports are harder to anticipate. Ethanol was not exported prior to 2009. Exports totaled 398.5 million gallons in 2010, 1.195 billion gallons in 2011, and are on track to reach about 740 million gallons this year. Large exports since December 2010 have been supported by reduced Brazilian ethanol production and are not expected to be sustained. Again, the impact of deviations from the expected level of exports on domestic ethanol production and corn consumption can be easily calculated.

The calculations in Table 3 point to a leveling off of domestic ethanol production at just over 13 billion gallons per year, implying annual corn consumption for ethanol production leveling off at about 4.7 billion bushels, below the recent peak of just over 5.0 billion bushels. The results underscore the importance of the magnitude of the blend wall and the critical importance of the rate at which E-15 is implemented. The calculations also indicate that the inventory of banked RINS (currently estimated at about 2.5 billion gallons) will be exhausted about mid-year 2015.

The biofuel scenario analyzed here has several important market and policy implications. These include:

- Corn consumed for domestic ethanol production will remain at a high, but stable level. As we indicated in an earlier post, the era of rapid growth has likely ended.

- Meeting the RFS for renewable biofuels with ethanol and banked RINS will be very difficult beginning sometime in 2015 if the blend wall is not expanded more rapidly than projected.

- Unless the total RFS is amended, the consumption of biodiesel is likely to expand rapidly beginning in 2014. This was also the subject of an earlier post.

Summary

The biofuels era that began in 2006 helped propel corn and other crop prices to a new higher level that has been sustained for nearly six years. One might be tempted to conclude that this new era is coming to an end as corn consumption for ethanol levels out and corn production begins to catch up. Instead, it actually appears that the new era of higher crop prices could be extended well into the future as a result of the RFS for advanced biofuels that in all likelihood can only be met with a rapid expansion in biodiesel production. To gain some perspective on the potential size of this expansion, consider our projection of 3.113 billion gallons of biodiesel production in 2015. This would require about 23.5 billion pounds of feedstock when total consumption of fats and oils in the U.S. currently totals about 28 billion pounds annually. Consumption of tallow and grease, another biodiesel feedstock, is thought to be near 10 billion pounds per year. At the projected level for 2015, biodiesel would account for over 60 percent of fats and oils consumption from all sources. This compares to about 20 percent in in 2012. The new price era, then, would not be extended by rising corn demand, but by rising vegetable oil demand. Whether this scenario actually is realized depends crucially on the evolution of biofuels policy here in the U.S. and energy policies in Brazil. We will be monitoring these issues closely in the future.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.