U.S. Farm Sector Capital Expenditures

U.S. farm sector capital expenditures continue to adjust to declines in net farm income and net cash income since 2013. Real net farm income has declined approximately 51 percent since its most recent peak in 2013, while real net cash income has declined approximately 29 percent since its most recent peak in 2012. Similar to past periods of declining margins, U.S. farms have responded to the declines in income by reducing capital expenditures. This article examines trends in capital expenditures and compares capital expenditures to capital consumption (i.e., economic depreciation).

Trends in Real Capital Expenditures

Figure 1 illustrates real U.S. farm capital expenditures and consumption from 1973 to 2017. Capital expenditures and consumption are expressed in 2016 dollars in figure 1. Capital expenditures include tractors, trucks, autos, machinery, buildings, land improvements, and miscellaneous capital expenditures. Capital consumption represents the declining balance of capital stock or economic depreciation. Using figure 1, two large increases in capital expenditures and two large decreases in capital expenditures have occurred since 1973. The first increase occurred during the 1973 to 1979 period. During this period, real capital expenditures increased from $44.4 billion in 1973 to $56.0 billion in 1979. The 1979 peak represents the highest annual capital expenditures level since 1973. The second increase occurred during the 2009 to 2014 period. During this period, real capital expenditures increased from $26.1 billion to $45.5 billion. The first large decrease in real capital expenditures occurred from 1979 to 1986. Real capital expenditures declined approximately 71 percent from the 1979 peak to the 1986 trough. The second large decrease is currently playing out. Since the 2014 peak, real capital expenditures have declined approximately 36 percent. However, it is important to note that real capital expenditures were similar in 2016 and 2017.

An alternative way to examine trends in capital expenditures and consumption is to compute the ratio of capital expenditures to capital consumption. This ratio is depicted in figure 2. A ratio above 1 indicates that capital is being replaced at a rate higher than economic depreciation. Conversely, a ratio below 1 indicates that economic depreciation is larger than capital replacement. The average ratio over the 1973 to 2017 period was 1.013, which indicates that on average capital replacement exceeded capital consumption. The annual ratio appears to be quite cyclical. The ratio of capital expenditures to capital consumption was above 1 from 1973 to 1980, below 1 from 1981 to 1997, above 1 from 1998 to 2013, and below 1 since 2014. The lowest annual ratios occurred during the 1980s farm financial crisis. As noted above there was a substantial decrease in capital expenditures in the 1980s. At the trough (i.e., 1986), the capital expenditures to capital consumption ratio was only 0.52. The three highest ratios occurred in 2008 (1.73), 2010 (1.46), and 2011 (1.70). Obviously, U.S. farms replaced a substantial portion of their depreciable capital during the 2007 to 2013 period. In the last couple of years, the capital expenditures to capital consumption ratio has dropped below 0.70. Though relatively low, the current ratio is still above the ratios experienced from 1982 to 1986. It is also noteworthy, that the ratio did not continue to drop in 2017, the 2017 ratio is almost identical to the 2016 ratio.

The discussion above applies to total capital expenditures. The changes in expenditures since the most recent peak in 2014 differs among expenditure categories. Data for 2017 is currently not available, so percentage decreases were computed using 2014 and 2016 data. The drop in total capital expenditures from 2014 to 2016 was 34.8 percent. The drop in tractors (38.0 percent), trucks (39.0 percent), autos (37.2 percent), and machinery (40.8 percent) was higher than the drop in total capital expenditures.

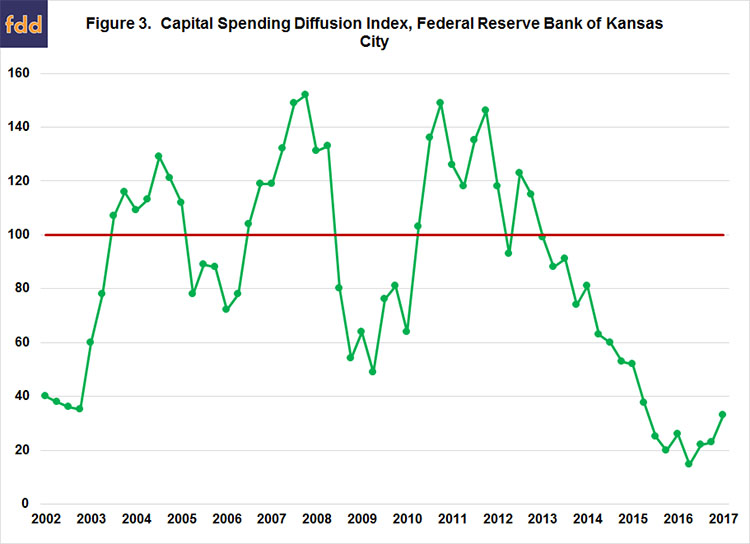

Capital Spending Diffusion Index

The Federal Reserve Bank of Kansas City (here) has reported a capital diffusion index on a quarterly basis since the second quarter of 2002. This diffusion index is computed by asking bankers whether capital spending during a quarter was higher than, lower than, or the same as in the year-earlier period. The index is then computed by subtracting the percentage of bankers who responded “lower” from the percentage who responded “higher” and adding 100. An index below 100 indicates that capital spending is relatively lower than the year-earlier period. Conversely, an index above 100 indicates that capital spending is relatively higher than the year-earlier period.

Figure 3 reports the capital spending diffusion index from the second quarter of 2002 to the second quarter of 2017. The index has been below 100 since the second quarter of 2013. The lowest index since then occurred in the third quarter of 2016 (diffusion index value of 15). Though it has strengthened during the last few quarters, the diffusion index value for the second quarter of 2017 was still only 33.

Conclusions

In response to declines in net farm income and net cash income, capital expenditures on U.S. farms dropped significantly from 2014 to 2016. Projected real capital expenditures in 2017 are similar to those in 2016. Moreover, though still relatively low, the capital spending diffusion index reported by the Federal Reserve Bank of Kansas City has increased slightly during the last few quarters. These trends suggest that capital expenditures have begun to stabilize. Whether this stabilization continues or capital expenditures increase depends on future net farm income prospects. A recent survey suggests that farmers are still reticent about profit prospects and whether this is a good time to make major capital purchases (Mintert et al., 2017).

References

Federal Reserve Bank of Kansas City. "Agriculture and the Economy." Accessed October 11, 2017. www.kansascityfed.org/research/agriculture.

Mintert, J., D. Widmar, and M. Langemeier. "Producer Sentiment Drifts Lower in August as Commodity Prices Weaken." Purdue/CME Group Ag Economy Barometer, September 5, 2017, accessed October 11, 2017. https://ag.purdue.edu/commercialag/ageconomybarometer/producer-sentiment-drifts-lower-august-commodity-prices-weaken/

USDA-ERS. "Farm Income and Wealth Statistics." Accessed September 27, 2017. www.ers.usda.gov/data-products/farm-income-and-wealth-statistics/

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.