Assessing the Profitability of U.S. Commercial Banks Participating in Agricultural Lending

In this article, we continue our series on U.S. Commercial Bank participation in agricultural lending. In our previous article (farmdoc daily, June 14, 2024), we looked at how the composition of commercial banks has changed since 2007. As of the fourth quarter of 2023, commercial banks specializing in agricultural lending have increased their loan volumes and market share. We extend this analysis by examining the differences in profitability between agricultural and non-agricultural commercial banks. We limit our analysis to FDIC-insured commercial banks that have outstanding farm real estate and farm operating loans on their balance sheets as of the fourth quarter of 2023. Two lending specializations are defined. Commercial banks whose sum of farm real estate and farm operating loans exceeds 25% of their net loans and leases are defined as agricultural banks, while all others are defined as non-agricultural banks. 1,022 commercial banks were categorized as agricultural banks, while 2,518 were categorized as non-agricultural banks.

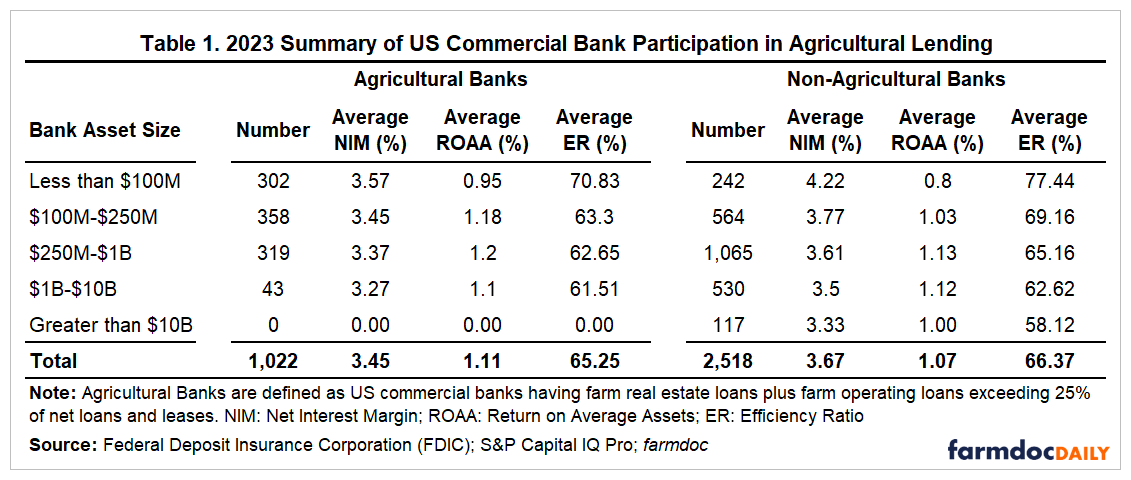

Table 1 shows the distribution of commercial banks by bank asset size and lending specialization in 2023. For each lending specialization, three profitability measures are reported. Net interest Margin (NIM) is defined as the difference between a bank’s net income generated from lending and investments and the interest expense paid on borrowed funds[1], relative to its average interest-earning assets. It measures the profitability of a bank’s lending activities. Return on Average Assets (ROAA) is a profitability ratio that compares a bank’s net income to its average total assets. It measures how efficiently a bank uses all of its assets to generate income. The Efficiency Ratio (ER) measures how cost-efficient a bank is and is defined as the ratio of its non-interest operating costs relative to the sum of its net interest income and non-interest income less provisions for credit losses. A bank with a lower ER is interpreted as operating more efficiently.

On average, compared to non-agricultural banks, agricultural banks reported a lower NIM in the fourth quarter of 2023. When bank asset size is considered, within both specializations, commercial banks with total assets less than $100 million reported the highest NIM; the average NIM for agricultural banks was 3.57% compared to 4.22% for non-agricultural banks. Additionally, the reported NIMs decrease for both specializations as the bank asset size increases. The Federal Reserve Bank has kept the target rate of the Federal Funds Rate (5.25-5.50%) at a 23-year high for almost a year and has increased interest rates 11 times since March 2022. Although one would expect a higher interest rate environment to benefit bank profitability, the effect of short-term interest rates on a bank’s NIM is theoretically ambiguous since its cost of funds may rise faster or slower than the yield on its earning assets, and the NIM is also influenced by many banking and economic conditions (FDIC Quarterly, 2021).

On average, agricultural banks reported a slightly higher ROAA (1.11%) compared to non-agricultural banks (1.07%). Although no agricultural bank had a bank asset size of greater than $10 billion, they reported higher average ROAA ratios across all bank asset sizes except for the $1 billion to $10 billion category. Within their specialization, agricultural banks with an asset size of $250 million to $1 billion had the highest average ROAA at 1.20%. Similarly, non-agricultural banks of the same asset size had the highest average ROAA at 1.13%. Agricultural and non-agricultural banks with less than $100 million in assets had the lowest average ROAA ratios at 0.95% and 0.80%, respectively.

Lastly, relative to their non-interest operating costs, agricultural banks demonstrated a better operating ability to generate income than non-agricultural banks in the fourth quarter of 2023. The average ER for agricultural banks was 65.25%, compared to 66.37% for non-agricultural banks. Within both specializations, commercial banks with assets less than $100 million reported the highest ER; agricultural banks reported an average ER of 70.83%, while non-agricultural banks reported an even higher ER of 77.44%. This size category was the least-cost efficient in both lending specializations. However, as the bank asset size increases, the reported average ER decreases. This is likely due to larger banks having a more diversified portfolio of interest-earning assets and services compared to their smaller counterparts.

Conclusion

In the fourth quarter of 2023, on average, commercial banks specializing in agricultural lending reported higher Return on Average Assets (ROAA) and were more cost-efficient than non-agricultural banks. However, non-agricultural banks reported a higher average Net Interest Margin (NIM). Within both lending specializations, the average NIM and Efficiency Ratio (ER) decrease as the bank asset size increases. Overall, the banking sector remains resilient in the US. However, in the most recent Federal Open Market Committee announcement, Jerome Powell added that “the economic outlook is uncertain, however, and we remain highly attentive to inflation risks.” In our next farmdoc article, we will assess the capital adequacy and condition of commercial banks issuing agricultural loans.

Note

[1] Borrowed funds consist of deposits and borrowings from other banks.

References

Federal Deposit Insurance Corporation. (2021). The historic relationship between bank net interest margins and short-term interest rates. FDIC Quarterly, 15(2), 31-41. https://www.fdic.gov/analysis/quarterly-banking-profile/fdic-quarterly/2021-vol15-2/article1.pdf

Mashange, G. "How the Composition of U.S. Commercial Banks Participating in Agricultural Lending has Changed Since 2007." farmdoc daily (14):112, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, June 14, 2024.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.