The Liquidity of Illinois Grain Farms: Current Ratio by Farm Size

In this article, we conclude our liquidity series by examining how the size of gross farm returns relates to the liquidity of grain farms. We will specifically look at the current ratio categorized by farm size, using data from the Illinois Farm Business Farm Management (FBFM). The current ratio is one of several measures used to assess a farm’s ability to meet its short-term financial obligations as they come due. It is calculated by dividing the value of a farm’s current assets by its current liabilities. Essentially, this ratio measures a farm’s capacity to pay off its short-term liabilities with its short-term assets. According to the Farm Financial Scorecard developed by the Center for Farm Financial Management, farms are categorized based on their current ratios as follows: a current ratio of less than 1.3 is categorized as vulnerable; a ratio between 1.3 and 2.0 is categorized as cautionary; and a ratio greater than 2.0 is categorized as strong.[1] Therefore, the higher the current ratio, the more liquid the farm is.

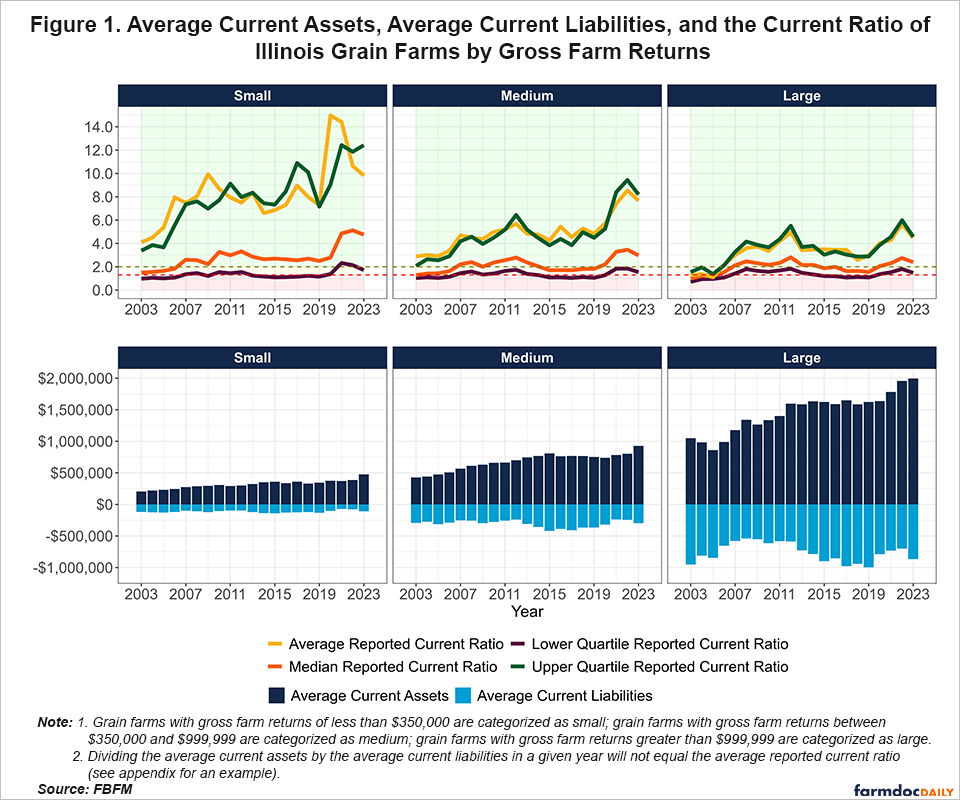

We present the trends of the average, lower quartile, median, and upper quartile current ratios of grain farms in Illinois over a twenty-one-year period from 2003 to 2023, using the current ratios reported by producers. Quartiles divide sorted data into four groups, each containing an equal number of values. In the context of the current ratio, the first quartile (lower quartile) represents the value below which 25% of the current ratio values fall. This indicates that 25% of farms have a current ratio lower than this value. The second quartile is the median of the dataset, meaning that 50% of the current ratio values fall below this point, representing the middle value of the current ratio for all grain farms. Lastly, the third quartile (upper quartile) is the value below which 75% of the current ratio values fall, meaning that 75% of farms have a current ratio less than this value. Additionally, we categorize the current ratio based on the size of gross farm returns: small, medium-sized, and large grain farms. Small farms are defined as those with gross farm returns less than $350,000; medium-sized farms have returns between $350,000 and $999,999; and large farms have returns greater than $999,999. In the top panel of our figure, we use the color-coding system from the Farm Financial Scorecard to indicate the category of each farm’s current ratio. The region shaded in red indicates a vulnerable ratio, yellow represents a cautionary ratio, and green indicates a strong ratio. Finally, in the bottom panel of our figure, we display the trends of the two components that make up the current ratio by calculating the annual average current assets and current liabilities across all grain farms by farm size. It is important to note that calculating the current ratio from these values does not equate to the average reported current ratio in the top panel of the figure. An example is provided in the appendix of this article.

Figure 1 shows the average, lower quartile, median, and upper quartile of the reported current ratio for grain farms in Illinois, along with the average current assets and liabilities. Overall, the current assets of grain farms have increased at a faster rate than their current liabilities resulting in improved current ratios. On average, small grain farms have reported substantially higher current ratios compared to medium-sized and large grain farms. Furthermore, the trend for the average current ratio for medium-sized grain farms has been higher than that of large grain farms. Although the average reported current ratio suggests that grain farms have maintained a strong liquidity position and improved it over time, this trend is more representative of the current ratios among grain farms that fall above the upper quartile across all three size categories.

The distributional differences of the upper quartile, median, and lower quartile reported current ratios are also interesting. As the size of the grain farm increases, the distributional differences get tighter. For example, the upper quartile reported current ratio for small grain farms has consistently been much higher than the median or lower quartile values across time compared to medium and large grain farms. Similarly, the difference across time of the median values compared to the lower quartile values is greatest for small grain farms.

Conclusion

In conclusion, when the size of gross farm returns is considered, our current ratio analysis of Illinois grain farms indicates a substantial improvement in liquidity over the past two decades. The average current assets of these farms have increased substantially, outpacing the growth in current liabilities, which has led to a rise in the current ratio over time. We find that on average, small grain farms have reported substantially higher current ratios compared to medium-sized and large grain farms. Some of the higher ratios for smaller farms can be attributed to a larger portion of household income coming from off-farm sources; thus, more resources are invested in short-term assets (bank and savings accounts, as well as stocks and bonds) and lower short-term liabilities (little to no operating notes, as cash from non-farm income is used to finance the farming operation). Although liquidity increased significantly at the turn of the decade, this trend has since reversed, and liquidity levels have been declining. This concludes our liquidity series. In our next series, we will be examining trends in solvency.

Acknowledgment

The authors would like to acknowledge that data used in this study comes from the Illinois Farm Business Farm Management (FBFM) Association. Without Illinois FBFM, information as comprehensive and accurate as this would not be available for educational purposes. FBFM, which consists of 5,000+ farmers and 70 professional field staff, is a not-for-profit organization available to all farm operators in Illinois. FBFM field staff provide on-farm counsel along with recordkeeping, farm financial management, business entity planning and income tax management. For more information, please contact our office located on the campus of the University of Illinois in the Department of Agricultural and Consumer Economics at 217-333-8346 or visit the FBFM website at www.fbfm.org.

Note

[1] The Farm Financial Scorecard adheres to the guidelines set by the Farm Financial Standards Council

Appendices

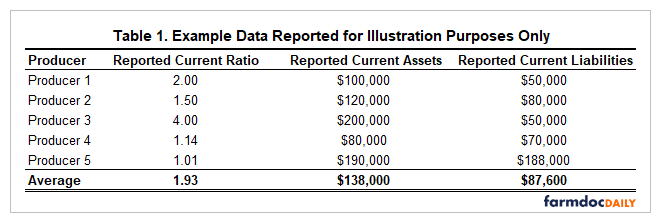

The data presented in Table 1 is fictional and will be used to illustrate how the average reported current ratio, displayed in the top panel of Figure 1, differs from the current ratio that would be obtained by dividing the average current assets by the average current liabilities shown in the bottom panel. Suppose in a given year, we have five producers reporting their current assets and liabilities. The first step is to calculate the current ratio for each producer by dividing their current assets by their current liabilities, shown in the fourth column of Table 1. Next, we calculate the average values of current assets, current liabilities, and the current ratio, shown in the table's bottom row. The average reported current ratio in that year would be 1.93. However, if we try to calculate the current ratio by dividing the average current assets by the average current liabilities, whose values would be shown in the bottom panel of Figure 1, we will obtain a value of 1.58 and not 1.93.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.