Double Trouble Part 2: Producers Impacted by Rising Interest Expenses and Larger Loan Payments

Increases in both interest rates and average loan sizes have led to significant increases in both interest expenses and first-year loan payments faced by FSA farm loan borrowers over the last twenty years. These changes vary by program and loan type. Between 2005 and 2025, guaranteed operating loans faced the largest increase in total first-year interest expenses, increasing 97 percent on average. This contributed to an increase in average first-year loan payment levels for guaranteed operating loans of 91 percent. Similarly, interest rate expenses and first-year payments for guaranteed farm ownership loans increased 76 percent and 66 percent, those for direct farm ownership loans increased 66 and 87 percent, and those for direct operating loans increased 67 and 66 percent.

This article is part of a two-part series addressing how changes in two key components- farm loan interest rates and average loan amounts- have impacted the average interest expense and first-year loan payment faced by borrowers receiving FSA Guaranteed and Direct Farm Loans between 2005 and 2025. The first article (see farmdoc daily article from January 30, 2026) covered changes in interest rates and loan amounts between 2005 and 2025 and potential causes for the rise in loan size. This second article addresses how these changes have impacted interest expenses and first year loan payments and provides potential strategies enabling borrowers to proactively address these challenges.

Background

FSA operates two distinct programs: direct and guaranteed loans. Direct loans are directly obligated and serviced by staff at FSA county offices. Guaranteed loans are obligated and serviced by approved commercial lenders. FSA guarantees the loan up to 95% of principal and interest against borrower default. Interest rates for direct loans are set monthly based upon cost of funds (USDA FSA 2025). The specific terms of guaranteed loans are set by the lender with interest rates subject to maximum limits. Direct and Guaranteed loan limits are set by congress. In order to qualify for an FSA loan, the borrower must meet a given set of criteria, not limited to being unable to obtain credit commercially in the case of direct loans or without the FSA guarantee in the case of guaranteed loans (USDA FSA b, 2025).

FSA offers two primary loan types, operating and farm ownership loans. Operating loans are for the purpose of purchasing livestock, seed and equipment, or covering farm operating costs and family living expenses (USDA FSA c, 2025). Farm ownership loans are aimed at purchasing or improving farmland including paying closing costs, constructing or improving buildings on the farm, or to conserving and protecting soil and water resources (USDA FSA c, 2025). Farm ownership loan terms are limited to no more than 40 years. Operating loans include both annual one-year lines of credit well as longer term loans, ranging from between 1 to 7 years. Results are shown only for term operating loans.

Calculating Loan Expenses and Payments

Loan data comes from the USDA FSA farm loan program datasets. To see how interest expenses and loan payment amounts changed between 2005 and 2025, the estimated first-year interest payment and total first-year loan payment amounts were calculated individually for each loan. The first-year interest payment was calculated as the loan interest rate times the loan principal. The first-year loan payment included both interest expenses and principal payments due. It was assumed that the borrower made one annual payment and that payments were split evenly over the length of the loan. This allowed setting the number of payments equal to the number of loan years and ignoring the possibility of ballon payments. It was also assumed that the loan interest rate was fixed for at least the first year even under the case of variable rate loans. Since we only look at first-year expenses and payments, this allowed treating variable and fixed rate loans similarly.

Annual loan payments were calculated using a standard loan amortization formula, where the annual payment was equal to the principal amount times the factor Z, where Z is the ratio of the interest rate times one plus the interest rate raised to the number of years divided by the number of years times one plus the interest rate minus one. Reported amounts are the average of the individual interest expense and loan payment amounts calculated separately for each loan.

Changes in Interest Rate Expenses and First-Year Loan Payments

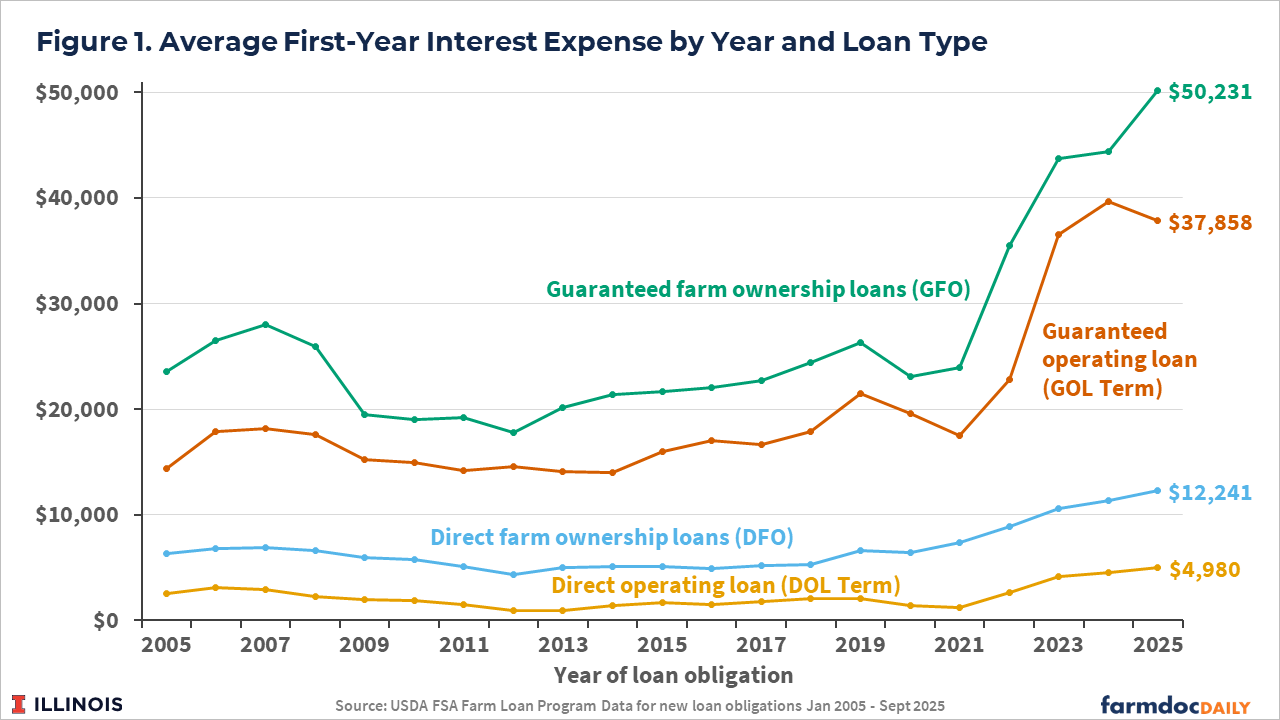

Figure 1 shows the average calculated first-year interest expense for newly obligated FSA loans by type and year between 2005-2025.

First-year interest expenses for guaranteed farm ownership loans more than doubled during the given period, from $28,000 on average in 2005 to $50,000 on average in 2025. Similarly, the first-year interest expense on guaranteed operating loans more than doubled, from $18,000 on average in 2005 to $40,000 on average in 2024. The magnitude of interest expense increases was smaller for direct loans compared to guaranteed loans, mainly due to their smaller average loan size. The first-year interest expense for direct farm ownership loans increased from $7,000 on average in 2005 to $12,000 on average in 2025, and direct operating loan interest expenses increased from $3,000 on average in 2007 to $5,000 on average by 2025.

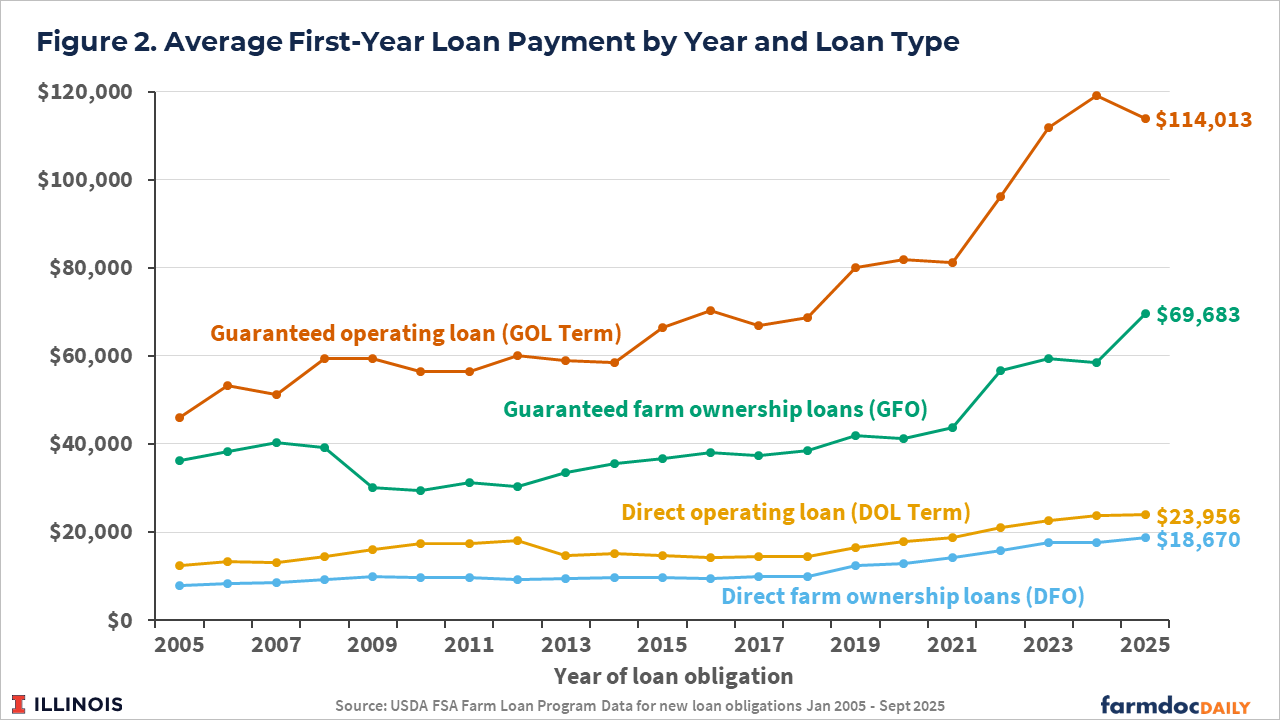

When principal payments are factored in, these increases are magnified. Figure 2 shows the average first-year loan payment (interest expense plus annual principal payment) for different loan types by year.

The average first-year payment for guaranteed operating loans more than doubled, from $46,000 on average in 2005 to $114,000 on average in 2025, and for guaranteed farm ownership loans almost doubled from $36,000 in 2005 to $70,000 in 2025. Similarly, the total first-year loan payment for direct farm ownership loans more than doubled from $8,000 on average in 2005 to $18,000 on average by 2025. Direct farm ownership loans experienced the smallest overall increase in first-year loan payments, going from $19,000 on average in 2005 to $24,000 on average by 2025.

Impact of Different Timeframes

Comparing the difference in interest expense and loan payments for newly obligated FSA loans in 2005 versus 2025 ignores important trends and shifts in interest rates and loan amounts that occurred during these twenty years. Primarily, this masks the impact of falling interest rates between 2008-2019, offset by increases in average loan size over the same time period.

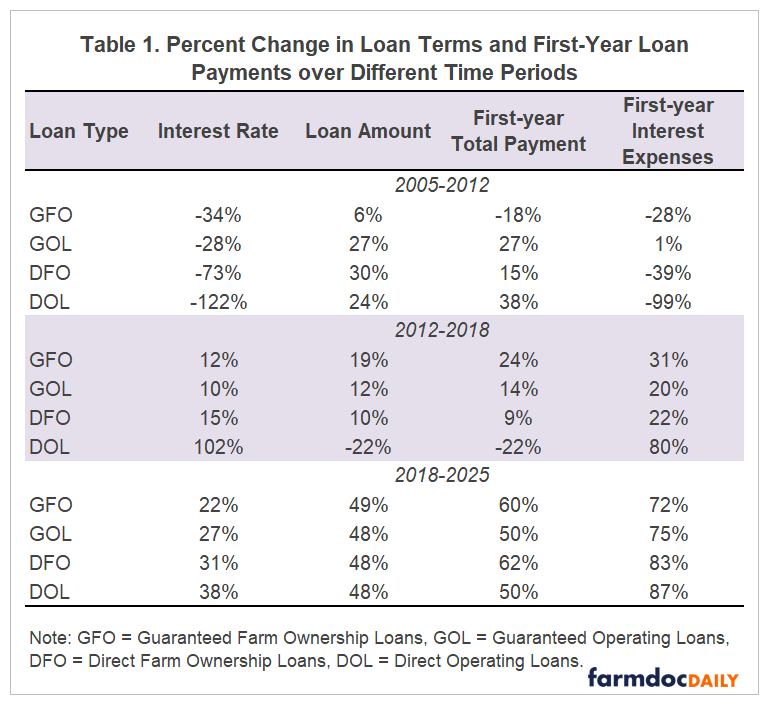

To better capture changes over time, the longer time period was broken into three smaller time frames, 2005-2012, 2012-2018, and 2018-2025. The average percentage change in interest rates, loan amounts, first-year interest expenses and loan payments over each different segment was calculated. The results are provided in Table 1.

Between 2005 and 2012 the average interest rate paid on FSA farm loans decreased for all loan types. This decrease ranged from between 28 percent for guaranteed operating loans to 122 percent for direct operating loans. This contributed to decreases in first-year interest expenses for almost all loan types. Direct operating loans exhibited the largest percentage decrease in first-year interest expenses (99 percent) followed by direct farm ownership loans (39 percent) and guaranteed farm ownership loans (34 percent). Despite significant decreases in interest rates and interest expenses, total first-year loan payments rose for all but guaranteed farm ownership loans. This increase was mainly due to increase in average loan amounts.

Between 2012-2018 interest rates and loan amounts increased slightly for most loan types, leading to relatively small increases in total interest expenses and first-year loan payments. The exception was direct operating loans, which experienced significant increases in average interest rates and interest rate expenses. It may be that these increases were a correction to the potentially overly large decline in direct operating loan rates in the prior period.

Between 2018-2025 interest expenses and first-year loan payments increased significantly. First-year total loan payments increased between 50-62 percent on average, while interest expenses rose between 72-87 percent on average. These increases were driven both by increases in the average interest rate as well as in the average size of loans.

Discussion

Increases in the average loan size have contributed to the increase in farm loan interest expenses and loan payment levels faced by producers. The impact of these loan increases is that while the average interest rate on a new FSA direct and guaranteed farm loan in 2025 is similar to those faced in 2007, the average interest expense and loan payment levels facing producers in 2025 are significantly higher than in 2007.

Farming is capital-intensive and farmers will likely continue to require access to credit, especially as we move into 2025 with expected shrinking farm margins for many producers. What does this mean for producers and what are some strategies that can be taken to mitigate these impacts? For producers, larger operating loans and resulting higher loan payments to cover this year’s expenses can become a drain on current working capital, reduce resources available for needed investment, and may lead to greater financial stress. The greatest impacts are most likely to be felt by those with high leverage and lower than average profits (Berg, 2023; Kreitman, 2024). Higher interest expense and loan payments are also likely to have a greater impact on operators who rely on short term financing using variable rate products or adjustable farmland loan products, as these loans are more apt to be refinanced at higher rates sooner. Adjustable farmland loans with five-year repricing schedules are common for farm real estate loans from commercial banks. The Kansas City Federal Reserve estimated that more than half of farmland loans outstanding in 2024 would be repriced in the next 18 months at higher rates than when the loan was originated (Kreitman, 2024). Borrowers with these loans are likely to first feel the impacts of increasing loan costs.

Producers can take steps now to mitigate the impact of higher loan costs. This includes focusing on controlling current expenses, carefully evaluating capital purchases and renting or borrowing instead of purchasing equipment if appropriate, timing purchases to take advantage of the best terms, carefully comparing options when undertaking vendor and other third-party financing, and taking advantage of off-farm earning opportunities to supplement income levels when possible. Importantly, producers need to employ greater diligence in evaluating land purchases. Purchasing high-cost land at high interest rates can burden the producer with large interest rate expenses, putting downward pressure on profitability as well as reducing the return on farmland investment (Kreitman, 2024). Finally, producers can seek out additional sources of credit or financing such state agricultural development programs or community supported agriculture programs which offer favorable rates and terms. Other credit options could include marketing loans to offer flexibility when crop prices are low or USDA FSA microloan programs, which provide lower loan amounts of up to $50,000 but often have lower costs and require less time to obtain. Options such as short-term operating loans, loan modifications to more closely match cash flow and crop cycles, or refinancing should be kept on the table but evaluated with care. The key is to work closely with your lender to determine the best possible plan moving forward.

References

Atkinson, S. "Double Trouble Part 1: Producers Request Larger Loan Levels with Rising Interest Rates." farmdoc daily (16):14, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, January 30, 2026.

Berg, Tait. “Elevated interest rates: How they impact producer’s cash flow and profitability.” Federal Reserve Bank of Minneapolis. July 28, 2023. https://www.minneapolisfed.org/article/2023/elevated-interest-rates-how-they-impact-producers-cash-flow-and-profitability

Kreitman, Ty. “Interest Expenses on Farmland Debt Could Challenge Farm Profitability.” kcFED Economic Bulletin. Federal Reserve Bank of Kansas City. February 14, 2024. https://www.kansascityfed.org/research/economic-bulletin/interest-expenses-on-farmland-debt-could-challenge-farm-profitability/

USDA FSA. “Current FSA Loan Interest Rates.” Accessed November 12, 2025. https://www.fsa.usda.gov/tools/informational/rates/current-fsa-loan-interest-rates.

USDA FSA b. “Farm Ownership Loans.” Accessed November 12, 2025. https://www.fsa.usda.gov/resources/farm-loan-programs/farm-ownership-loans.

USDA FSA c. “Farm Loan Programs.” https://www.fsa.usda.gov/resources/farm-loan-programs. November 12, 2025.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.