Expected Corn and Soybean Returns and Shifts in Acres

Tomorrow’s (March 31) release of USDA’s Prospective Plantings report will focus attention on 2015 plantings of corn and soybean. Many expect corn acres to decrease and soybean acres to increase. Where acreage shifts could occur are examined by calculating 2015 expected corn minus soybean returns for counties in the United States. These projections suggest that shifts to soybeans are more likely outside the Corn Belt. Moreover, expected 2015 returns suggest smaller acreage shifts than in other recent years.

Construction of 2015 Corn minus Soybean Returns

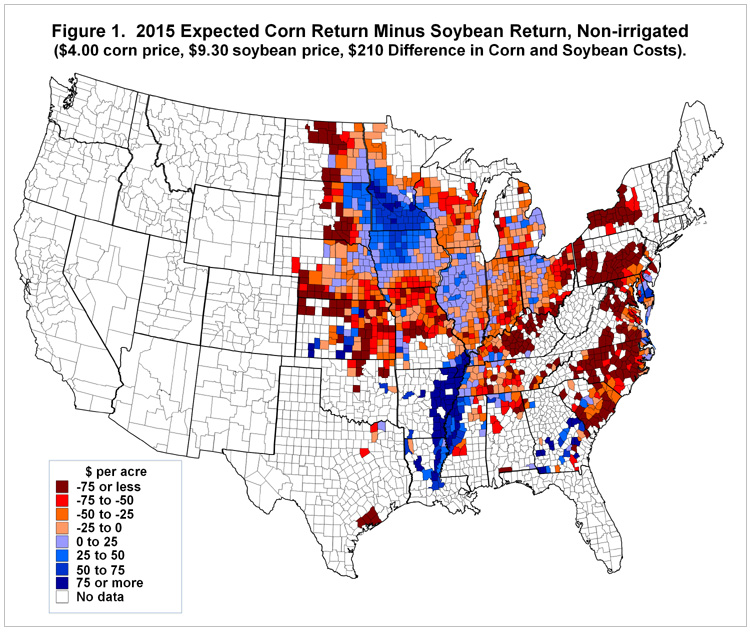

Figure 1 shows a county map shaded based on each county’s expected 2015 expected corn return minus expected 2015 soybean return. Blue shaded counties have higher expected corn returns than soybean returns while red shaded counties have higher expected soybean returns.

These values for each county are used in constructing the map in Figure 1:

- Expected corn revenue equals expected corn price times the county’s expected yield. The corn price is $4.00 per bushel. The 2015 expected yield is a trend yield based on fitting county yield data from 1972 to 2014.

- Expected soybean revenue equals expected soybean price of $9.30 per bushel times the county’s expected yields. Expected 2015 soybean yields represent a trend yield calculated in a manner similar to that for corn.

- Difference in corn and soybean costs. Corn costs minus soybean costs are calculated using 2015 Illinois Crop Budgets. Corn minus soybean costs for 2015 equal $215 per acre.

Expected 2015 corn returns minus soybean returns then equals:

Expected corn revenue – expected soybean revenue – difference in corn and soybean costs.

A county had to have at least six of the last ten years of yields for both corn and soybeans to be included in the analysis. Also, non-irrigated yields are included in this analysis. Use of irrigated yields in places like Nebraska would cause corn to have higher expected returns than soybeans.

2015 Expected Corn minus Soybean Returns

Note that much of the Corn Belt has higher expected corn returns than soybean returns. Southern Minnesota, northern and central Iowa, and northern and central Illinois have higher expected corn returns (see Figure 1). Also, corn is expected to have higher returns than soybeans in the Mississippi Delta. Given that corn is expected to have higher returns in these areas, one would not expect large shifts from corn to soybeans in these areas. Shifts to soybeans likely are to occur outside the central Corn Belt and the Mississippi Delta.

2015 Expected Returns Compared to Other Years

Compared to several recent years, the geographical patterns shown in Figure 1 do not suggest large changes in 2015. To illustrate, two recent years are compared to expectations in 2015.

Corn planted acres increased from 92 million acres in 2011 to 97 million in 2012, an increase of 5 million acres. Soybean acres increased from 75 million in 2011 to 77 million acres in 2012. The large increase in corn acres was associated with higher expected corn returns than soybean returns over much of the United States, as illustrated in Figure 2. Figure 2 is calculated in the same manner as Figure 1 except that values in the spring of 2012 were used in constructing the graph. Corn expected returns were much higher than soybean expected returns over most counties in the greater corn-belt and Mississippi Delta.

Corn planted acres decreased from 95 million acres in 2013 to 91 million acres in 2014, a decrease of 4 million acres. At the same time, soybean acres increased from 77 million acres to 84 million acres, an increase of 7 million acres. Soybean returns were higher than corn returns over much of the United States, as illustrated in Figure 3.

Soybeans were expected to be more profitable than corn over more counties in 2014 than in 2015, as can be seen by visually comparing Figure 3 to Figure 1. Note that more counties had soybeans having higher returns than corn in 2014 than in 2015. Moreover, soybeans had higher expected returns in 2014, as indicated by more counties having darker shades of red in 2014 (Figure 3) as compared to 2015 (Figure 1).

Summary

In 2015, corn has higher expected returns than soybeans in much of the center of the Corn Belt, suggesting that shifts to soybeans may occur outside the Corn Belt. Moreover, the expectations in 2015 currently do not suggest as large as shifts as occurred in 2014.

More insights into 2015 plantings will be gained with USDA’s release of the Prospective Plantings report on March 31st. This report then could lead to market reactions and changes in market prices, leading to future revisions in planting intentions.

References

Schnitkey, G. "Crop Budgets, Illinois, 2015." Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, January, 2015.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.