Cash Rent with Bonus Leasing Arrangement: Description and Example

A “cash rent with bonus” leasing arrangement is a variable cash rent lease that has a base rent and the potential for a bonus if crop revenue exceeds target revenue. Variable lease rental arrangements have become more popular in recent years as crop prices have become more variable, thereby making it more difficult to determine satisfactory cash rents. This document describes details of cash rent with bonus arrangements.

Basics

The landlord and farmer agree on a base rent that will be paid no matter the yield or price level. A bonus results if crop revenue exceeds a crop revenue target. Crop revenue is determined based on the yield from the farm and a price. The price typically is an average of prices from a delivery point near the farm. This lease differs from others which may be based on crop insurance parameters (available here) in that the rent is based on yields from the farm.

For a cash rent with bonus rental arrangement to work properly, the landlord and farmer must agree on certain parameters. These parameters are described in the following section. After harvest is complete, the bonus can be calculated and the final cash rent will be determined. This process is described in the “Calculation of the Bonus” and “Calculation of Rent” sections.

Parameters of a Cash Rent with Bonus

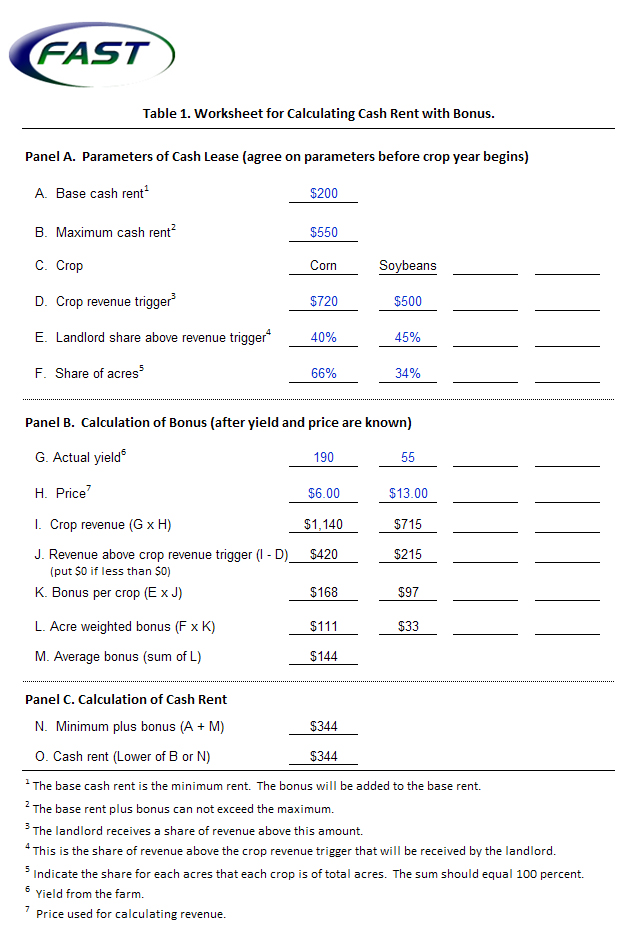

Table 1 shows a worksheet for setting parameters of a cash rent with bonus arrangement and then determine the bonus and cash rent at harvest. Panel A gives parameters of the cash rent with bonus lease that should be determined at the time of signing up for the agreement. These parameters are:

- Base cash rent is the minimum cash rent that the landlord will receive regardless of crop revenue. In Table 1, the base cash rent is $200 per acre.

- Maximum cash rent is the maximum cash rent the landlord will receive. In Table 1, the maximum cash rent is $550 per acre.

- Crops can have an influence on the crop revenue trigger and landlord share of revenue above the trigger. Hence, each crop is listed and then parameters are listed by crop in lines D and E.

- Crop revenue trigger. The landlord will receive a bonus based on revenue above the crop revenue trigger. In Table 1, the crop revenue trigger is $720 for corn and $500 for soybeans.

- Landlord share above revenue trigger is the landlord’s share of crop revenue above the trigger. In the example, the landlord share is 40% for corn and 45% for soybeans.

- Share of acres indicates the share of acres in each crop. In Table 1, 66% of the acres are in corn and 34% are in soybeans.

Calculation of the Bonus

The bonus is calculated after harvest is complete so that yield is known. Panel B of Table 1 shows how the bonus is calculated:

- Actual yield is the yield from the farm. The farmer will provide the landlord with harvested bushels, typically specified at a standard moisture level. In the example, the yield is 190 bushels for corn and 55 bushels for soybeans.

- Price is used to calculated at revenue. One method for calculating price is to select a local delivery point and then collect prices from those delivery points. For example, prices could be collected each Wednesday beginning March 1 through October 31st. Others use futures prices or crop insurance prices. In Table 1, the price is $6.00 for corn and $13.00 for soybeans.

- Crop revenue equals actual yield times price. In Table 1, Crop revenue for corn is $1,140 (190 bushel yield x $6.00 corn price) and for soybeans is $715 (55 bushel corn yield x $13.000 per bushel price).

- Revenue above crop revenue trigger gives the amount of revenue on which a bonus is calculated. In Table 1, revenue above the trigger is $420 per acre for corn ($1,140 crop revenue – $720 crop revenue trigger) and $215 per acre for soybeans ($715 soybean crop revenue – $500 crop revenue trigger).

- Bonus per crop equals revenue above crop revenue trigger times the landlords share above revenue trigger. In Table 1, corn has a bonus of $168 per acre ($420 revenue above trigger x 40% landlord share) and soybeans have a bonus of $97 per acre ($722 revenue above trigger x 45% landlord share).

- Acre weighted bonus takes the bonus per crop and multiplies that crop’s share of acres. This is done so that per acre bonuses can be added together to arrive at the average bonus. In Table 1, the acre weighted bonus for corn is $111 per acre (66% of acres in corn x $168 bonus for corn) and for soybeans is $33 per acre (34% of acres in soybeans x $97 bonus for soybeans).

- Average bonus is the sum of the acre weighted bonuses. In Table 1, the average bonus is $144 per acre (sum of $111 for corn + $33 for soybeans).

Calculation of Cash Rent

Once the bonus is calculated, the cash rent can be determined. Panel C of Table 1 shows this calculation.

- The minimum plus the bonus equals the base cash rent plus the average bonus. In Table 1, the minimum plus the bonus is $344 per acre ($200 base cash rent + $144 bonus).

- The cash rent will be the smaller of the maximum cash rent (Line b) or the base rent plus bonus (line N). In Table 1, the base rent plus the bonus is the smaller of the two, resulting in a $344 per acre rent.

Setting Parameters for a Cash Rent with Bonus

Critical parameter to understand is the non-land costs of producing crops. Budgets are available in the management section of farmdoc (available here). For 2012, non-land costs are estimated at about $520 per acre for corn and $300 per acre for soybeans. The crop revenue trigger can be set at non-land costs plus the base cash rent. In Table 2, the $720 trigger for corn equals $520 non-land costs plus $200 base cash rent and the $500 trigger for soybeans equals $300 non-land cost and $220 base cash rent.

The landlord share above revenue trigger should relate to the base cash rent. Higher landlord share above the trigger should be associated with lower base cash rents. A lower base cash rent indicates that the landlord is willing to bear more risks and hence should be compensated with a higher share of revenue above the trigger

FAST Spreadsheet: Cash Rent with Bonus Worksheets

A FAST spreadsheet entitled “Cash Rent with Bonus Worksheet” (available here) can be used to evaluate alternative cash rent with bonus arrangements. This spreadsheet includes the worksheet in Table 1. Also included are sheets that show how cash rent with bonus performs under different prices and yields. An example of the corn sensitivity analysis is shown in Figure 1. This spreadsheet was develop with Jeff Reed and Bob Rhea, field staff in Illinois Farm Business Farm Management.

Summary

Often, it is difficult to agree on a fixed cash rent because of uncertainty about the economic outlook for the coming leasing period. A cash rent with bonus leasing arrangement allows rent to vary with different prices and yields, thereby allowing the rent to adjust to realized prices and yields. A blank form of the worksheet is included in the appendix.

Appendices

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.