2011 IFES: Crop and Livestock Price Prospects for 2012

This is a presentation summary from the 2011 Illinois Farm Economics Summit (IFES) which occured December 12-16, 2011 at locations across Illinois. Summaries and MP3 podcasts of all presentations will be republished on farmdoc daily. The ‘Presentations’ section of the farmdoc site has PDF presentation slides and MP3 podcasts from all presenters here.

Crops

Crop prices continue to trade in wide ranges, reflecting factors ranging from U.S. and world production uncertainty to world economic and financial conditions. The price environment will likely remain very unsettled in 2012.

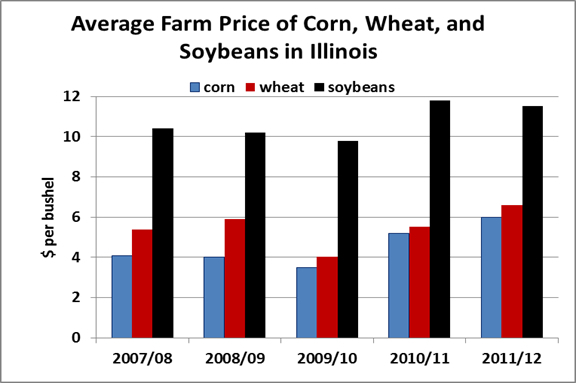

The small corn crop in 2011 should result in small inventories by the end of the marketing year. Large grain crops in the rest of the world will keep export demand weak. The expiration of the ethanol benders’ tax credit and declining broiler and cattle numbers point to stagnant domestic consumption in the first half of 2012. Southern hemisphere corn production is expected to increase in 2012, but hot, dry conditions are currently being experienced in Argentina. U.S. farmers may increase corn acreage and a higher yield in 2012 would result in more abundant supplies, but uncertainty will persist through the summer. Prices are expected to remain in the mid-$5 to low-$6 range in early 2012. Prices later in the year will reflect crop prospects and world financial conditions.

A small U.S. soybean crop in 2011 has been met with weaker demand. A large South American harvest in 2011 and expectations for another large crop in 2012 has resulted in weaker export demand for U.S. soybeans, meal, and oil. Chinese purchases started more slowly than in the previous year. Year ending stocks of U.S. soybeans will be relatively small, but adequate. U.S. soybean acreage in 2012 will need to be maintained near the level of 2011. Supply uncertainty will persist through the summer of 2012, suggesting that prices will be maintained in a wide range around $11.

Total U.S. wheat production declined sharply in 2011, but SRW production was nearly double the small crop of 2010. Production of wheat in the rest of the world was up sharply, leading to declining export demand for U.S. wheat and prospects for adequate year ending stocks. Most of the 2011 wheat crop in Illinois has been sold, at an average price near $6.60. The focus early in 2012 will be on U.S. winter wheat seedings, the status of drought conditions in the HRW areas, and prospects for the Australian crop. A more modest northern hemisphere wheat crop in 2012 and a lingering drought in the U.S. southwest would be supportive for prices late in 2012. Prices in the first half of the year may remain in the mid-$5 to mid-$6 range.

Livestock

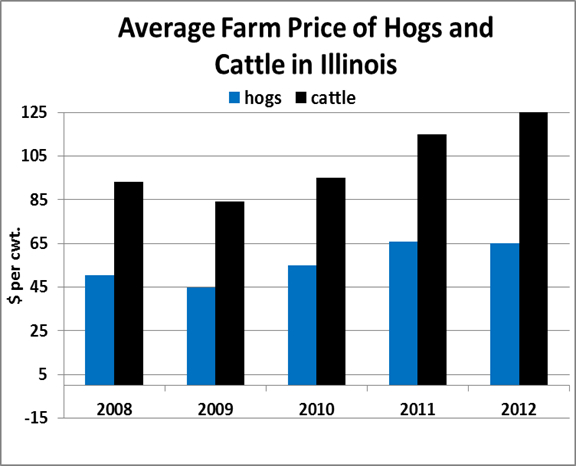

U.S. pork production is expected to increase from 22.7 billion pounds in 2011 to 23.1 billion pounds in 2012. Exports of U.S. pork grew from 3 billion pounds in 2006 to a projected 5.1 billion pounds in 2011. Exports will remain large in 2012. Domestic pork supplies are projected at 46.2 pounds per capita in 2012, up from 45.7 pounds in 2011. The average price of hogs in Illinois was only $45 in 2009, but likely exceeded $66 in 2011. Prices are expected to average in the mid-$60 range in 2012.

U.S. beef production has declined slowly from the peak of 26.6 billion pounds in 2008 to a projected 25 billion pounds in 2012. From a 19 year low of 460 million pounds in 2004, U.S. beef exports grew to 2.78 billion pounds in 2011 and should remain at that level in 2012. Domestic per capita beef supplies declined from 59.6 pounds in 2010 to 57.4 pounds in 2011 and are projected at only 54.1 pounds in 2012. Fed cattle prices averaged $95 in 2010, but jumped to $115 in 2011. Depending on economic conditions, the average for 2012 could be near $125.

Additional Resources

- The slides for this presentation can be found at:

- http://www.farmdoc.illinois.edu/presentations/IFES_2011

- For current outlook information, see:

- http://www.farmdoc.illinois.edu/marketing/newsletters.html

- http://www.agmanager.info/

- http://www.agecon.purdue.edu/extension/prices/index.asp

- http://cattlemarketanalysis.org/

- http://www.extension.iastate.edu/agdm/

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.