Do Futures Forecast the Future?

A common presumption is that futures prices can predict future price, specifically the price during the last or delivery month of trading on a futures contract. This presumption has potential importance for both marketing and policy. Many crop insurance contracts use futures prices to establish their pre-plant and harvest prices. In addition, it is common to hear that futures prices should be used to forecast prices when evaluating the farm program choices in the 2014 farm bill. This article calls into question the presumption that futures prices can predict future price. It also finds that cash price performs as well as futures price in forecasting future price. Because of the technical nature of the analysis, the article begins with its summary observations. Readers can then decide if they want to read the details of the analysis.

Summary Observations

- A futures price provides an unbiased forecast of future price but forecast error is large.

- A futures price provides no better forecast of future price than using last crop year’s cash price.

- Implication 1: crops with no futures market have no disadvantage in predicting future price

- Implication 2: using futures prices to help determine the farm program choice in the 2014 farm bill offers no advantage over using the 2014 crop year average price

- Implication 3: lack of a futures market is not a reason for not offering crop insurance; last crop year’s average cash price works just as well as a forecast

- Futures markets do provide one marketing advantage. They allow a price to be established for a future time by selling a futures or cash forward contract. But, this advantage is only acquired by selling the crop since price usually changes, often substantially. In other words, this advantage is obtained by selling at a price you like not because the forecast will turn out to be correct.

- Futures markets do provide one advantage for crop insurance. It allows earlier settlement of insurance claims. However, this advantage is limited since partial payments can be made on crop insurance contracts that use cash prices.

- While radical given the long history of using futures prices to determine crop insurance prices, this study begs the question if futures prices are in fact the best method for establishing the price of insurance contracts.

Background

Length of time over which corn and soybean futures contracts are traded has steadily increased over the last half century. Prior to 1970, it was rare that corn and soybean futures contracts traded a year prior to delivery. In contrast, on Friday, August 1, 2014, the December 2017 corn contract and July 2017 soybean contract traded. The increasing length of trading has reinforced the presumption that futures markets forecast future price.

Analysis

This study examines the forecast performance of the November soybean and December corn futures contract 1 year prior to delivery. The price of these so-called new crop futures contracts are averaged during their November/December delivery period and during the November/December one year prior to delivery. These average prices are then compared. To illustrate, average price of the November 2006 soybean contract during November 2005 is compared with average price of the November 2006 soybean contract during its delivery month of November 2006. We also compare, for example, the average U.S. cash price during the 2005 crop year with the average U.S. cash price for the 2006 crop year. In other words, we examine the potential of last crop year’s U.S. average price to forecast the current crop year’s U.S. average price.

The period of analysis is the 1975 through 2006 crop years. This was an extended period of what are called stationary prices. Stationary prices have no long term trend up or down and have stable price variation. Nonstationarity in prices can lead to an overstatement of price forecast performance.

The U.S. corn and soybean markets have desirable attributes when testing forecast performance. The U.S. is a major producer of corn and soybeans and thus the markets are heavily traded. The U.S. also produces corn and soybeans in a limited and similar timeframe, which creates a more uniform market environment in which to examine price forecast performance.

Findings — Futures Price Forecast Performance

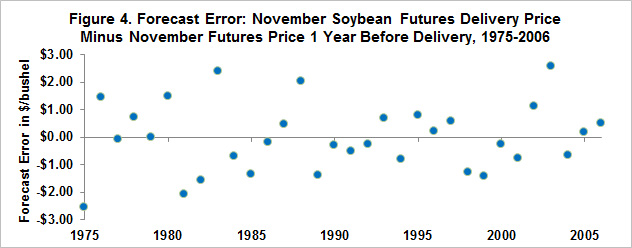

Figure 1 compares the average price of the December corn futures contract during its December delivery month with its average price during December of the previous year. A different graph of this data is provided in Figure 2. It shows the forecast error by year, where forecast error is defined as the average December delivery month price minus the average December price during the previous December. Figures 3 and 4 are the comparable set of graphs is presented for soybeans.

Over all the 32 years for corn, the December delivery month futures price averages 13 cents per bushel below the December futures price during the previous December (see Figure 5). While not small in a value sense, it does not differ statistically from 0 at commonly used levels of statistical significance. The reason it is not statistically significant is the high variation in forecast error as illustrated in Figure 2. In comparison, for soybeans over the 32 years, the November delivery month futures price averages 3 cents per bushel below the November futures price during the previous November (see Figure 5). This difference is highly insignificant. The implication of these findings is that the December corn futures contract and November soybean futures contract provides an unbiased estimate of the futures price that will occur during the delivery month. In this measure of forecast performance, the forecast of price provided by these futures contracts is accurate.

However, considerable error exists in the forecasts. For corn, in only 5 of the 32 years is the December futures price during the delivery month within 5% of the December futures price during the previous December. The comparable number for the November soybean futures contract is 6 of the 32 years. In only 1 of 64 possible crop-year combinations does the forecast error round to 0%: 1979 November soybeans. The average absolute forecast error is 16% for both the December corn and The November soybean futures contracts (see Figure 6).

Last, a regression line between the two delivery prices is presented in Figures 1 and 3. This regression line reveals how much of the variation in the delivery month futures price is explained by the futures price one year prior. For corn, this explanation is 11% (R2 value). The explanation is even lower for soybeans, 4%. The corn regression line has a statistical confidence of 93% while the soybean regression line has a statistical confidence of 72%. A commonly-used level of statistical confidence is 95% in terms of assessing whether the relationship differs from zero. In other words, from a statistical confidence perspective, neither the corn nor soybean new crop futures price one year prior to delivery helps explain what the new crop futures price will be at delivery, although the December corn futures price is not far from being statistically significant.

Findings — Comparing Cash and Futures Price Forecast Performance

A simple forecast of cash price is to assume that this year’ price will be the same as last year’s price. On average, last crop year’s U.S. cash price was nearly identical to this crop year’s U.S. cash price (see Figure 5). In fact, this difference was less than for the December corn and November soybean futures prices. Average forecast error was nearly identical for last crop year’s cash price and the new crop futures price (see Figure 6), with both having a forecast error of approximately 16%.

To further compare forecast performance, Figures 7 and 8 presents the forecast errors for both futures and cash prices. These figures also contain the regression line fitted between the two forecast errors. For both corn and soybeans, approximately 75% (R2 value) of the cash price forecast errors are explained by the futures price forecast errors. The figures and the regression lines both reveal that the futures price and crop year cash price forecasts have errors that tend to be similar. When taken as a group, Figures 5 through 8 suggests that new crop futures prices provide no better forecast of next year’s price than does last crop year’s U.S. average cash price.

The regression lines in Figures 7 and 8 reveal other important information. For corn, the regression intercept is 10 cents per bushel and it is differs from 0 at the 98% level of statistical confidence. This statistical confidence implies that the futures price forecast is biased relative to the cash price forecast. Thus, in terms of this measure of forecast performance, the cash price forecast performs better. For soybeans, the intercept coefficient is 2 cents per bushel and statistical confidence is approximately 8%. Thus, for soybeans there is no difference in the bias of the futures price and cash price forecasts.

The slope coefficient for both corn and soybeans is approximately +0.8. (the number followed by the x). The +0.8 slope coefficient is interpreted as follows: each 1 cent forecast error of the new crop futures price is associated with approximately a 0.8 cent forecast error for last crop year’s cash price. If the forecast errors are similar in size, the slope coefficient should equal +1.0. However, both slope coefficients differ from +1.0 at the 95% level of statistical confidence, implying that forecast error of estimating the U.S. crop year cash price by the previous crop year’s U.S. cash price is somewhat less than the forecast error of estimating the new crop futures price at delivery by using the new crop futures price 1 year prior to delivery. In other words, the cash price forecast is again somewhat better than the futures price forecast on this measure of forecast performance.

This publication is also available at http://aede.osu.edu/publications.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.