Watching Your Instrument Panel

Harvest is on us and it’s time to give serious thought to how this year will end financially if you haven’t done so already. Coming off of a period of years of sustained profitability, the prudent manager will consider the past (without dwelling on it – you can’t change it) while thinking about the future…it’s hard to move forward in the manner you want if you only have a rear view mirror to guide you.

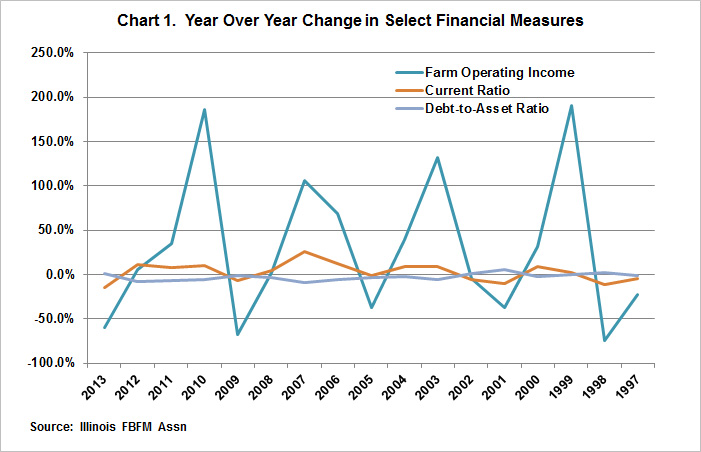

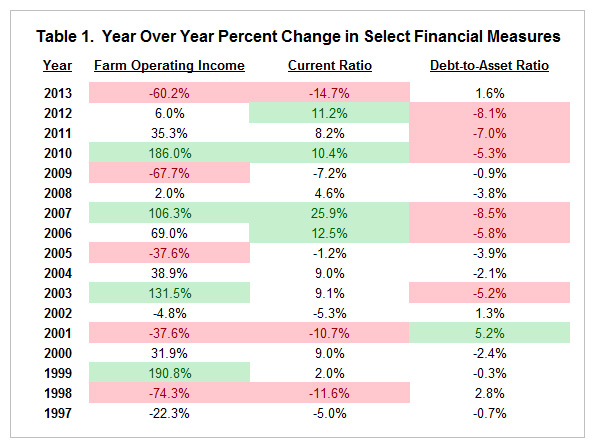

To put things is a bigger perspective, consider Table 1, it contains a review of data from a period that spans 1996 to 2013 – a period of 18 years and 17 intervals. Over that period, income levels have varied considerably and there is some thought that with the ethanol mandate put in place that there is a new plateau of price levels and some might even say that has extended to farm earnings.

This article will not delve into those issues, but will more simply review some of the changes that have occurred over time and try to put them in perspective with the price levels at the present for our commodity crops.

While the level of earning is important, let’s look at the change in the level of earnings over time as represented by accrual farm operating income. While the recent period shows the greatest levels of actual dollars of farm income, the change in the level of farm operating income is remarkable. There are four periods that are noted for a year-over-year change that exceeds 100%. There are five periods that show a negative year-over-year change with two of those near a 40% decrease with the other three periods showing decreases of approximately 60% to 70%.

The financial summary of the year is very readily seen in accrual farm operating income. Income less expenses transmits to the bottom line in a quick and is easily seen and understood. Other financial measures show the year-to-year changes in a more muted fashion. The current ratio (current assets divided by current liabilities) is obviously influenced by farm operating income, but changes less dramatically than farm operating income depending on how and where farm operating income is used. There are only seven of the eighteen periods that register a change of over 10% from year-to-year. Four of those periods show a positive change and three of those show a negative change. The most recent year-to-year change (2012 to 2013) shows the most dramatic of the negative changes in the current ratio.

The change in the debt-to-asset ratio changes in an even more muted way than the current ratio. In seven of the periods, the change in debt-to-asset ratio was over a positive or negative 5%. The remaining ten periods show a change in debt-to-asset ratio of less than 5% positive or negative.

Summary

Every year provides a different set of operating conditions – weather, markets, interest rates, etc that test the skills of farm operators. The eighteen years at hand tells that while farm income can change dramatically from year to year, the effects of a change in income are transmitted more readily to some ratios than others. Make yourself knowledgeable about all of the financial measures of your farming operation. If you borrow money, your lender will be very aware of those financial measures.

Be aware of the things that have the greatest financial impact. Data would tell us that the five expense categories that make up the greatest percentage of your expenses are: fertilizer, seed, pesticides, depreciation and family living.

Consider yourself the pilot of your farming operation. You know you need to pay attention to your instrument panel (your financial measures) as they tell you ‘how’ well you are flying the plane. It is paramount that you know how to operate the aircraft (your management skills) as your financial measures show the result of your management skills. Watching the instrument panel is only useful if you know how to react and make changes.

The author would like to gratefully acknowledge that data used in this study comes from the local Farm Business Farm Management (FBFM) Associations across the State of Illinois. Without their cooperation, information as comprehensive and accurate as this would not be available for educational purposes. FBFM, which consists of 5,700 plus farmers served by 60 professional field staff, is a not-for-profit organization available to all farm operators in Illinois. FBFM field staff provide on-farm counsel along with recordkeeping, farm financial management, business entity planning and income tax management. For more information, please contact the State FBFM Office located at the University of Illinois Department of Agricultural and Consumer Economics at 217-333-5511 or visit the FBFM website at www.fbfm.org.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.