Little Tax Depreciation Exists on Many Illinois Grain Farms

Many Illinois grain farmers have reduced capital purchases in recent years, with prospects for further cuts in 2017 and future years. Overall, reducing capital purchases is a prudent step in times of low grain farm returns. Reducing capital purchases, however, could result in higher than expected 2017 tax liabilities. Many farmers used section 179 expensing and bonus depreciation to deduct most of the value of capital items in the year of purchase. As a result, little tax deprecation may exist from capital items purchased in previous years. In this article, trends in capital purchases and economic depreciation are shown from 2003 to 2016. Then, 2016 comparisons of tax and economic depreciation are presented.

Capital Purchases on Illinois Grain Farms

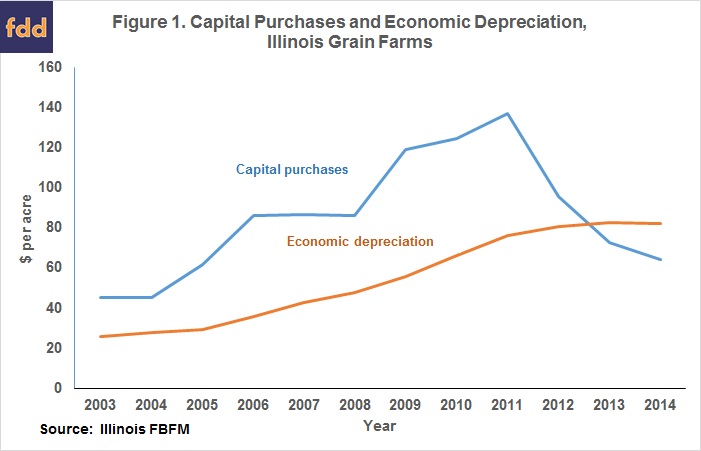

As reported by Illinois Farm Business Farm Management (FBFM), capital purchases on Illinois grain farms increased from the mid-2000s to 2013, reaching a high of over $130 per acre. Since 2013, capital purchases have decreased to about $60 per acre in 2016 (see Figure 1).

As would be expected, economic depreciation also increased during this period, reaching mid-$70 per acre range in 2016 (see Figure 1). Reported in Figure 1 is economic depreciation calculated by FBFM. FBFM calculates economic depreciation based on 125% declining balance depreciation methods using a $0 salvage value. In addition, FBFM uses the alternative depreciation system, ADS, which has a longer life than the more widely used general depreciation system (GDS). For most farm machinery, which is seven-year property (GDS) for most on a tax perspective, a ten-year life (ADS) is used to calculate economic depreciation.

Economic depreciation differs from depreciation used for calculating income taxes. Tax depreciation often is calculated using schedules which depreciate capital items quickly. Moreover, many grain farms use section 179 expensing and bonus depreciation. Section 179 expensing allows up to $510,000 of capital purchases made in 2017 to be deducted immediately. In some cases, 50% bonus depreciation comes into play when the section 179 deduction has been reached. Often, all or a significant portion of capital purchases are used to reduce income in the year purchase. In those cases, there is little deprecation remaining over the remaining life of the capital item.

As compared to tax methods, economic depreciation schedules typically spread out depreciation over a longer period. To Illustrate, the economic depreciation schedule used by FBFM for a typical $100,000 piece of farm machinery is $6,250 in the first year of service, $11,720 in the second year, $10,250 in the third year, $9,570 in the fourth through the tenth year, and $4,790 in the eleventh year. For tax purposes, the full $100,000 of the machine may have been deducted in the first year using section 179 expensing.

Comparison of Tax and Economic Depreciation

Many farmers used section 179 expensing for purchases made in 2006 through 2013 when incomes were relatively high. As a result, capital purchases made in those previous years have little depreciation remaining on schedules. In most cases, only farmers making purchases in the current year will have the ability to section 179 expense or add to depreciation amounts.

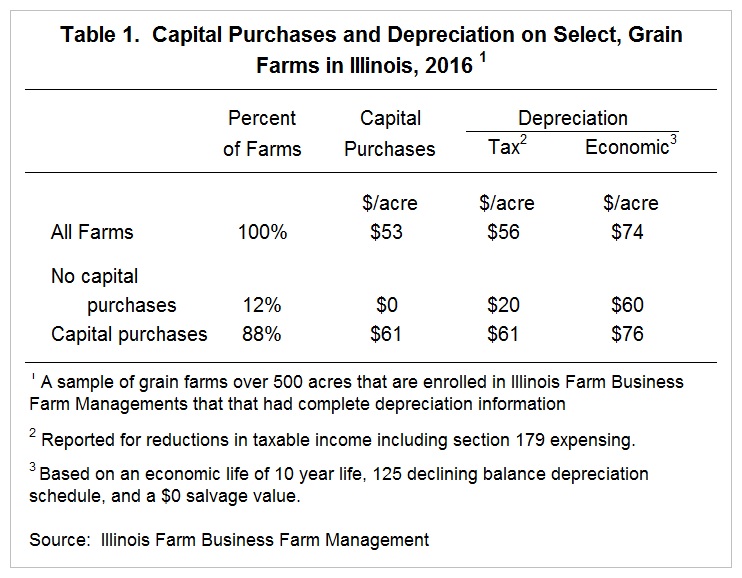

This fact is illustrated in Table 1, which shows 2016 values of per acre capital purchases and depreciation for a sample of grain farms enrolled in FBFM. Farms summarized in this table had at least 500 acres and had useable tax and economic depreciation information. There are 546 farms summarized in Table 1 with an average farm size of 1,200 acres.

In 2016, all the farms in the sample averaged $53 per acre in capital purchases. These farms had $56 per acre in tax depreciation. Note that the capital purchase and tax depreciation values are relatively close to one another. One way this could occur is if section 179 was used to deduct most of the 2016 capital purchases. These same farms had $74 per acre of economic depreciation, $19 more than tax depreciation.

The impact of 2016 capital purchases can be seen by examining differences in tax depreciation for those farms that had capital purchases in 2016 and those that did not. Of the 546 farms, 12% of the farms did not have capital purchases and had a $20 per acre in tax depreciation (see Table 1). This $20 per acre in tax depreciation is much less than the $61 per acre in tax depreciation for those farms that had capital purchases in 2016. The farms with capital purchases averaged $61 per acre in capital purchases, near the level of tax depreciation in 2016.

Summary and Implications

Many farms will have little tax depreciation if capital purchases are low due to use of section 179 expensing in previous years. As a result, these farms may have taxable liabilities even if net incomes are very low. This fact does not suggest that capital purchases should be made. Lower agricultural returns likely lead to lower capital purchases. Rather, it suggests tax planning should occur. Larger than hoped for tax liabilities should be anticipated.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.