Cash Is King

In good times cash is king and in not so good times it is even better. There are three primary liquidity ratios that are important from a business perspective. And we in agriculture are no different. A cash cushion gives one a good position to launch a new initiative and it can be of benefit to fall back on when one?s business may not be able to generate the cash desired.

The three commonly used measures of liquidity are 1) working capital, 2) the current ratio, and 3) the working capital to gross farm returns ratio.

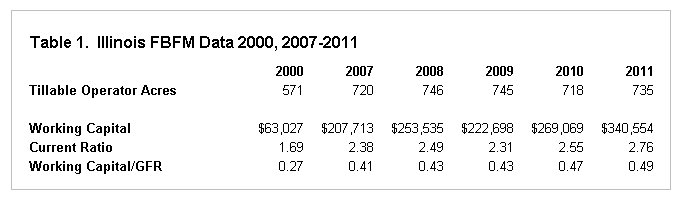

Working Capital is the result of subtracting your current liabilities from your current assets. Working capital is measured in dollars and is difficult to compare between farms. One can look at the same farm over time and to get an idea of the increase or decrease in working capital. From 2007 to 2011 from data provided by the the Illinois FBFM Association, median working capital has increased from $207,713 to $340,554. Farm size increased only 15 acres while gross farm returns increased by 39% over the same period.

The current ratio is the result of dividing current assets by current liabilities. If the current ratio is greater than 1, then there is positive working capital. Conversely, if the current ratio is less than one, the working capital is negative. The current ratio is a more comparable number than is working capital. The current ratio varies by age of the farm operator and farm type; the older the farm operator the more likely they are to have a greater level of working capital and a higher current ratio. Grain farms tend to have higher current ratios than do livestock farms. From the same group of Illinois FBFM data, the current ratio increased from 2.38 in 2007 to 2.76 in 2011.

Working Capital to Gross Farm Returns ratio is the result of dividing Working Capital by Gross Farm Returns. This ratio gives a relative measure of one?s cash cushion. In 2007, this ratio was 0.41 and it increased to 0.49 in 2011. In 2007, working capital was 41% of gross farm returns and in 2011 working capital was 49% of gross farm returns. That might not seem like a large increase, but remember gross farm returns were increasing during this period as well.

As with most financial analysis, it takes many pieces to complete the puzzle. Any of these three financial measures provides good input to the financial management of one?s end-of-year balance sheet and accrual income statement. Considering all three of them provides an even higher level overview.

With the current condition of the Illinois crop, strategizing to maintain prudent liquidity could go a long way to providing some peace of mind. If you don?t have a financial trend analysis that includes a five year history of your liquidity ratios, now might be a good time. See Table 1 below for a five year history for sample of farms in Illinois that participate in the Illinois FBFM Association. This table includes a look back to this same information in the year 2000. That was only twelve years ago, but how the times have changed. The liquidity ratios were at significantly lower levels than those of the recent five year era and gross farm returns were well under 50% of the recent past. Life is never boring for those involved in agriculture! This year it seems like a roller coaster ride?and we?re blindfolded and riding backwards!

The author would like to acknowledge that data used in this study comes from the local Farm Business Farm Management (FBFM) Associations across the State of Illinois. Without their cooperation, information as comprehensive and accurate as this would not be available for educational purposes. FBFM, which consists of 5,500 plus farmers and 60 professional field staff, is a not-for-profit organization available to all farm operators in Illinois. FBFM field staff provide on-farm counsel along with recordkeeping, farm financial management, business entity planning and income tax management. For more information, please contact the State FBFM Office located at the University of Illinois Department of Agricultural and Consumer Economics at 217-333-5511 or visit the FBFM website at www.fbfm.org.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.