The Ongoing Debate over Farmland Taxation

All 50 U.S. states provide some form of preferential tax treatment for agricultural land (see Sherrick and Kuethe, 2014). These tax policies were adopted state-by-state in response to the rapid loss of farmland associated with the rapid expansion of urban land use activities, following World War II. The majority of States tax farmland through a form of use-value assessment. Under use-value assessment, agricultural lands are taxed according to the potential earnings from agricultural production, rather than the full market value of the property. The goal of these programs was to limit farmers’ tax liability based on the belief that, in many areas, farmland market values were predominantly driven by the potential conversion to non-agricultural uses, such as housing or commercial development. The mechanisms used to measure potential earnings from agricultural have come under fire in a number of states, as a result of the recent declines in farm profitability. Farmers in a number of states have argued that the measures of “potential” earnings drastically lag the realized decline in farm profit margins.

The two most common concerns expressed by farmers are that (1) the effective tax rate exceeds the underlying value of the property and (2) the tax burden accounts for an outsized share of farm production expenses. In order to examine these two concerns, we rely on a number of relevant economic measures provided by the USDA Economic Research Service’s Farm Income and Wealth Statistics database. We examine data from the most recent available year, 2015.

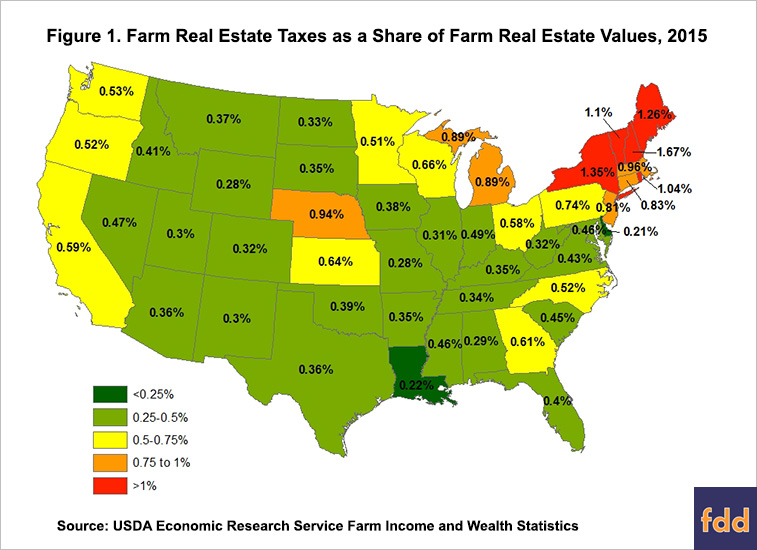

To examine the first concern, Figure 1 shows the total farm real estate taxes paid in each state divided by the state’s total farm real estate value. The ratio is an approximate measure of the “effective tax” rate for farmland in each state. The USDA’s measure of farm real estate values includes the approximate market value all land, buildings, structures, and improvements but excludes operator dwellings. The tax expenses related to operator dwellings are similarly excluded. Figure 1 indicates a clear regional pattern. Effective tax rates are highest in the Northeast, at well above one percent of the farm real estate value. The lowest effective tax rates are found in Louisiana and Delaware, but the rates are relatively stable across most of the Midwest and Plains states.

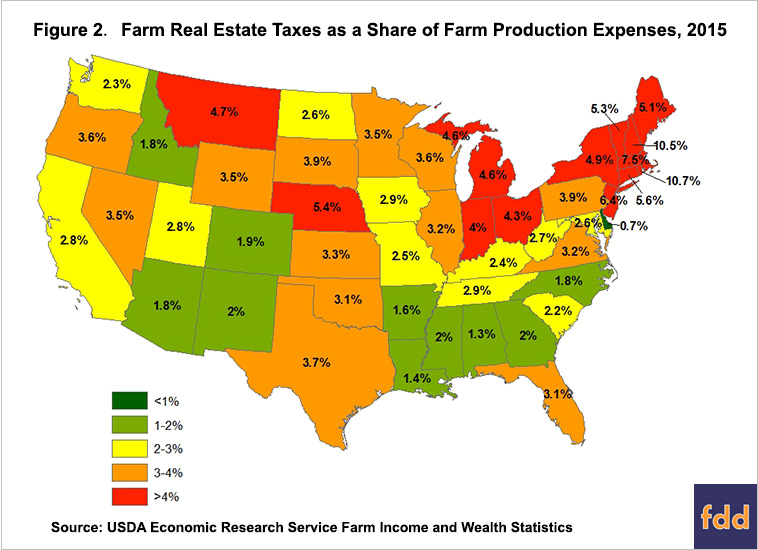

To examine the second concern, Figure 2 shows the total farm real estate taxes paid in each state as a share of total farm production expenses. This ratio therefore captures the relative tax burden. Again, production expenses exclude all costs associated with operator’s dwellings. The tax burden also indicates a clear regional pattern. Real estate taxes represent a larger share of production expenses in Northeastern States, but farm real estate taxes exceed four percent of total production expenses in a number of other states, including Indiana, Ohio, and Nebraska.

While farmland owners in all 50 States are given some form of preferential property tax treatment, a continued decline in farm profit margins will likely result in farmers requesting additional property tax relief. These debates are mostly likely to occur in areas in which the effective tax rate is higher than national average or in states in which property taxes represent a large share of production expenses.

References

Sherrick, B. and T. Kuethe. "The Taxation of Agricultural Land in the United States." Policy Matters, Department of Agricultural and Consumer Economics, University of Illinois, October 15, 2014. http://policymatters.illinois.edu/the-taxation-of-agricultural-land-in-the-united-states/

USDA Economic Research Service. Farm Income and Wealth Statistics, accessed March 10, 2017. https://www.ers.usda.gov/data-products/farm-income-and-wealth-statistics/

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.