Rising Interest Rates – What to Consider on Your Farm

As the Federal Reserve has raised interest rates in response to rising inflation (farmdoc daily, October 12, 2022), the average Illinois grain farm has various things to consider when analyzing the effect on their farm. Using data from Illinois Farm Business Farm Management (FBFM), this article will look at the current make up of debt on the farm and interest as a percent of gross farm revenue as some factors that can be looked at to determine the impact of rising interest rates on individual farms.

In 2021, the average total (farm and non-farm) debt on Illinois grain farms enrolled in FBFM was $925,437, this compares to $335,036 in 2002. Total debt on these Illinois grain farms has almost tripled in 20 years, primarily due to rising asset values. Figure 1 shows these values as well as the make-up of the loan terms. On the total debt in 2021, 39% was for short-term obligations. This includes operating loans, accounts payable, accrued interest on all loan terms, Commodity Credit Corporation (CCC) loans, the current portion due in twelve months on intermediate and long-term loans, etc. that typically have one-year or less term. Another 11% was for intermediate term loans (includes vehicle loans, machinery loans, grain bins, etc.) that typically are from more than a year to seven-years. The final 50% is long-term obligations (includes farmland, homes, farm buildings, etc.) that have the longest term of greater than 7 years. These percentages have changed over time with short term loans being the largest percentage until 2018 when long-term loans became a larger portion of the total.

When looking at the short-term share, the farm operating loan portion has averaged 65% of the total short-term loans over 20 years. 29% of all loans on average are for farm operating loans. As interest rates increase, the first impact to the farm is on operating loans as they can only be one year at a time. Therefore, the amount of interest paid on operating loans will increase the most in the short term. In addition, with rising operating expenses forecasted for the rest of 2022 and 2023 (farmdoc daily, November 15, 2022), this will likely increase the amount of operating debt needed, also increasing interest paid.

Current intermediate term notes will not be affected if the interest rate was locked in. However, as farmers purchase equipment, they will need to consider the rising interest rates in addition to the rising value. Capital budgeting for machinery will help you plan out your needs and be able to plan for replacement of equipment when needed. However, these added increases may lead to delays in those plans, so now is a good time to either start or reevaluate a long-term capital budget for machinery purchases to manage any extra interest cost.

Like with intermediate term notes, current long-term notes will not be affected if there is a fixed interest rate. If long term assets are purchased such as land or buildings, those will now have a higher loan payment due to the rise in interest rates.

Even though new loans will have higher interest rates, farmers have held onto cash over the last couple of years due to higher incomes leading to increases in working capital. Another way to express working capital is the current ratio. The 2021 current ratio of 3.32 (farmdoc daily, November 15, 2022) was the highest since 2012. The cash portion of this working capital can be used to mitigate the increased interest rates in the near term by paying operating expenses and down payments on new purchases to allow for less funds to be borrowed at higher rates. However, if interest rates continue to rise over a longer period and incomes decrease, working capital could be needed to offset current liabilities.

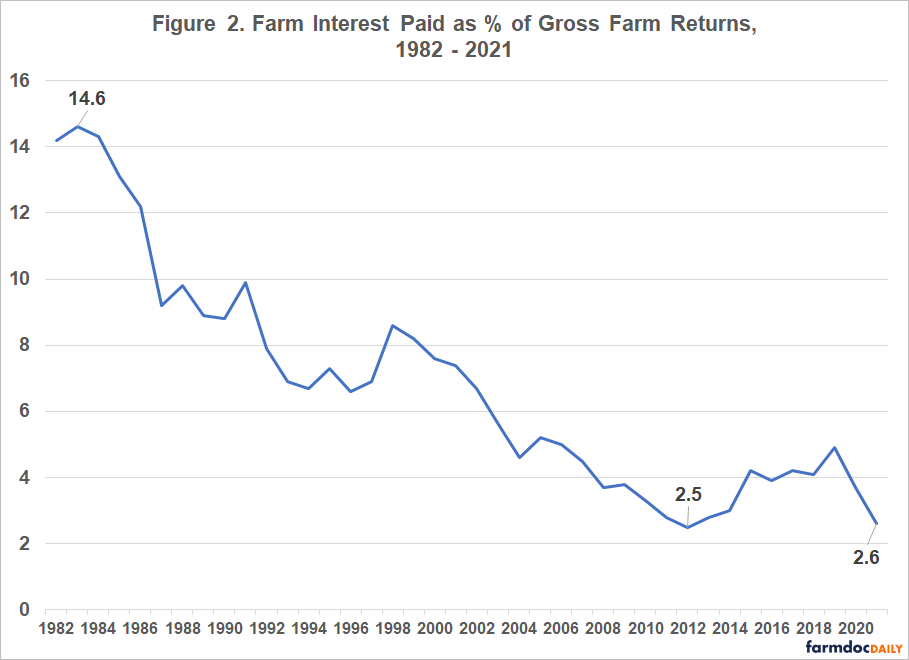

Figure 2 shows interest paid as a percentage of farm gross revenue from 1982 until 2021 for Illinois farms. During this 40-year window, we have seen interest paid as a percent of farm gross revenue as high as 14.6% in 1983 and as low as 2.6% in 2021. While this measure is not only affected by the amount of interest paid but also farm gross revenue, long term, multi-year averages can remove some of the variability over time. The most recent 20-year average (2002-2021) for interest as a percent of gross farm revenue was about 4%. This compares to the last 10-year average of 3.6% and the 40-year average of 6.8%. Even with rising interest rates and increasing loan values leading to higher interest expenses, interest as a percentage of gross revenue has been declining over time due to higher gross revenues.

Summary

Rising interest rates will have an impact on farms. Farm operating loans will be affected first for most farms leading to higher interest expense. As farms acquire machinery, land and buildings with debt, more non-current debt will have higher rates leading to larger interest expenses for many years. However, working capital can be used to help minimize the amount of debt needed, especially when considering long term loans at higher rates. Over the last 40 years, interest as a percent of gross farm revenue has been decreasing and has averaged about 4% over the last 20 years. Farm interest has been a small portion of gross returns and will continue to be until more of the intermediate and long-term loans on the balance sheet have a higher interest rate due to new purchases. If purchases of machinery, buildings and land are not needed, continue to increase working capital during profitable years to help with down payments as well as larger loan payments when purchases are made. Each farm will be impacted differently due to rising interest rates, so good recordkeeping and understanding of your financial statements will help you move your operation forward during this period of higher interest and volatility.

The author would like to acknowledge that data used in this study comes from the Illinois Farm Business Farm Management (FBFM) Association. Without Illinois FBFM, information as comprehensive and accurate as this would not be available for educational purposes. FBFM, which consists of 5,000+ farmers and 70 professional field staff, is a not-for-profit organization available to all farm operators in Illinois. FBFM field staff provide on-farm counsel along with recordkeeping, farm financial management, business entity planning and income tax management. For more information, please contact our office located on the campus of the University of Illinois in the Department of Agricultural and Consumer Economics at 217-333-8346 or visit the FBFM website at www.fbfm.org.

References

Schnitkey, G., C. Zulauf, N. Paulson and J. Baltz. "Grain Farm Income Projections for 2022 and 2023." farmdoc daily (12):172, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 15, 2022.

Zulauf, C. "Update on US Interest Rates and Inflation." farmdoc daily (12):155, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 12, 2022.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.