2026 Illinois Farmland Price Expectations: Navigating a Stable Yet Softening Market

Following the substantial appreciation in farmland valuations observed during the early 2020s, the Illinois farmland market is currently transitioning toward a period of stabilization. According to the latest annual survey from the Illinois Society of Professional Farm Managers and Rural Appraisers (ISPFMRA), market participants anticipate that while long-term optimism remains incredibly strong, near-term land values face modest downward pressure (see the Land Values report from the Illinois Society).

This controlled softening is primarily driven by tighter crop margins, higher expected input costs, and a contracting broader agricultural economy. This article details the survey’s findings on these shifting price expectations, historical parallels to previous market plateaus, the underlying economic factors driving current sentiments, and the evolving impact of alternative land uses such as renewable energy and data centers.

Near-Term Expectations

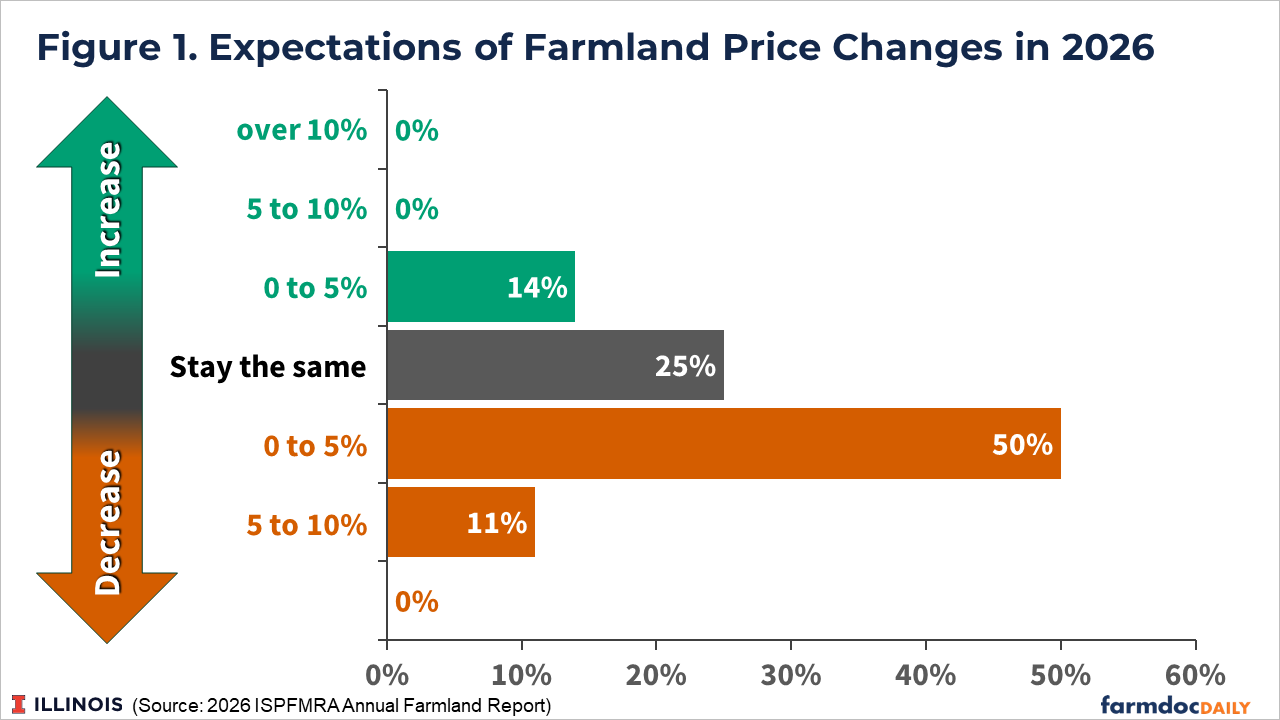

The ISPFMRA survey indicates a clear consensus that the rapid, double-digit appreciation of farmland values has paused. When asked about their expectations for 2026, 61 percent of respondents indicated they expect farmland prices to decline overall.

However, this anticipated decline is expected to be highly controlled rather than a severe market correction. As shown in Figure 1, exactly half (50%) of the respondents expect prices to decrease in a narrow margin of just 0 to 5 percent. Another 11 percent foresee a slightly deeper decline between 5 and 10 percent. Notably, zero percent of respondents expect a severe drop of more than 10 percent. On the other side of the spectrum, 25 percent expect farmland prices to remain the same, and 14 percent anticipate a slight increase of 0 to 5 percent.

Despite near-term caution, long-term expectations remain strong. When asked where farmland prices will be five years from now, 77 percent of respondents expect prices to be higher. Specifically, 5 percent expect prices to be more than 10 percent higher. This dichotomy between short-term softening and long-term appreciation highlights the belief in Illinois farmland as a resilient asset.

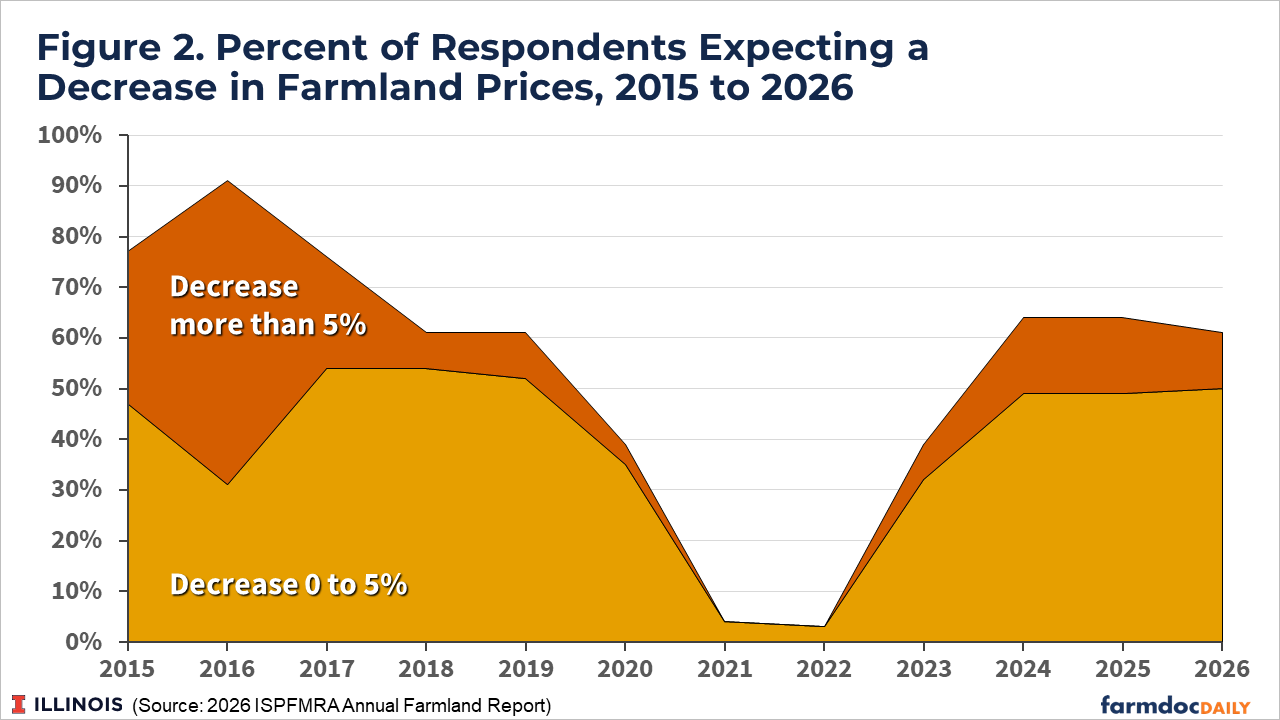

This near-term view of a stable but softening market is remarkably consistent with the sentiments recorded in the most recent surveys, but it also mirrors an earlier period in the agricultural economy. As shown in Figure 2, the percentage of respondents expecting price declines for 2024, 2025, and 2026 has consistently remained between 61 and 64 percent. This prevailing level of market apprehension concerning short-term valuations aligns closely with the documented sentiment of the 2018 and 2019 agricultural cycles. During those years, a similarly high percentage of respondents expected price declines, and farmland prices remained relatively flat overall, facing distinct downward pressure without collapsing.

Interestingly, the current market environment shares a major characteristic with the 2018/2019 period: a heavy reliance on ad hoc federal payments to support farm incomes. Much as the Market Facilitation Program (MFP) provided crucial financial support to farmers navigating trade disruptions in 2018 and 2019, recent years have seen similar interventions. Programs like the Economic Relief Program (ERP) and the Farmer Bridge Assistance (FBA) program provided critical revenue support in 2024 and 2025; for instance, the 2025 FBA program provided $44 per planted acre for corn and $34 for soybeans. This historical parallel strongly suggests that such payments are playing a stabilizing role in the land market, much as they did in 2018 and 2019.

The Agricultural Economy and Crop Prices

Beyond federal assistance, the cautious outlook for 2026 is heavily influenced by an anticipated compression in agricultural profit margins. Specifically, 72 percent of survey respondents expect average corn prices to remain modest, forecasting a range between $4.00 and $4.50 per bushel. Concurrently, 69 percent of the surveyed cohort anticipates that aggregate farming costs will continue to escalate.

This projected rise in operational expenses is exacerbated by geopolitical volatility; specifically, ongoing disruptions in the Middle East have introduced supply chain uncertainties that place sustained upward pressure on global energy and fertilizer markets. Ultimately, the intersection of modest commodity prices, high input costs, and a sustained high-interest rate environment yields an overarching expectation of exceptionally tight margins, which inherently restricts aggressive farmland valuation growth.

Market Volume

As price expectations soften, transaction volumes are also cooling. Sixty percent of respondents noted a decrease in the overall volume of farmland sold in the latter half of 2024 compared to the previous year. Looking at 2026, 35 percent expect volume to decline further, while 47 percent expect it to remain unchanged.

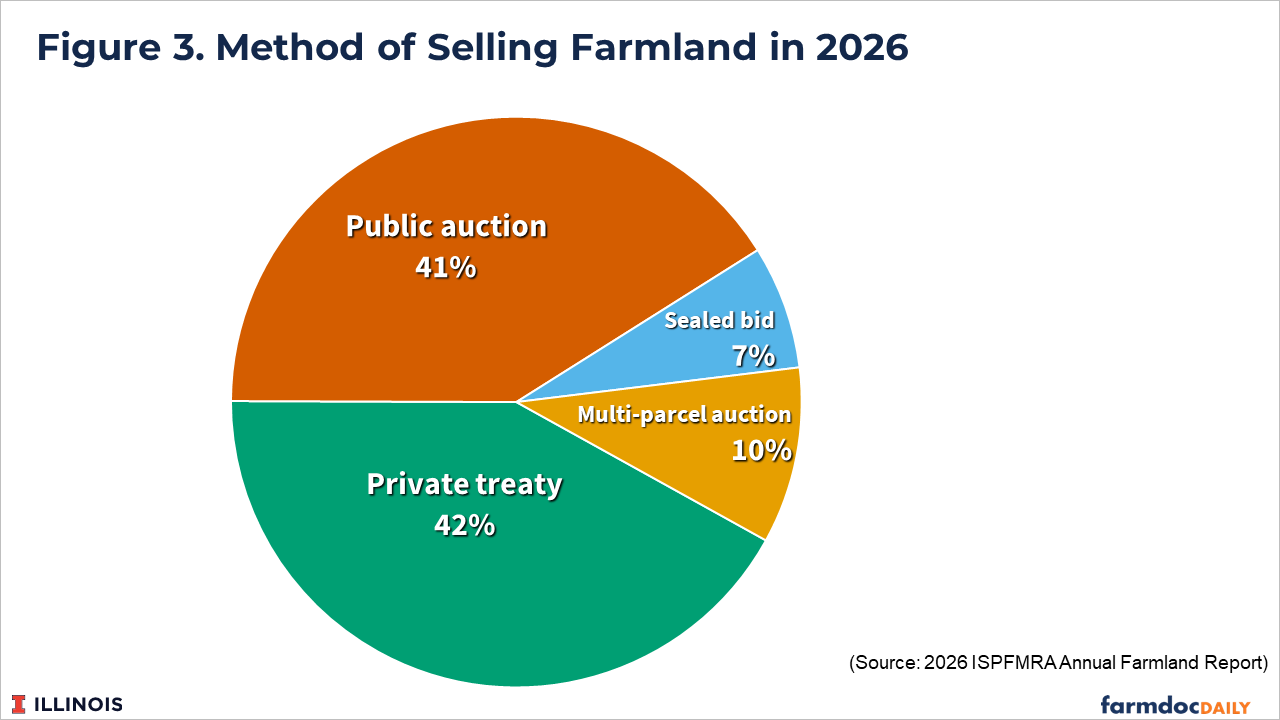

Alongside this cooling volume, the methods by which farmland is transacted are shifting, suggesting that buyers and sellers may now prefer bilateral negotiation over public competition. This represents a notable departure from recent trends; the prevalence of public auctions increased dramatically between 2020 and 2023, ultimately peaking at 53 percent of all transactions in 2023. However, as detailed in Figure 3, this trajectory has reversed, with private treaty sales regaining primacy and edging out public auctions in 2025.

This subtle pivot toward private treaty transactions implies a market where participants value the ability to directly negotiate terms in a softening economic environment. Additionally, this trend could be driven by an increasing presence of buyers utilizing 1031 tax-deferred exchanges. These buyers often require the flexibility, confidentiality, and extended timelines that private and negotiated sales can provide, as opposed to the rigid and highly competitive structure of a public auction.

When farmland does change hands, local farmers continue to be the primary purchasers, accounting for 56 percent of all buyers, while individual non-farming investors account for roughly a third of the Illinois farmland market. Despite high capital requirements, debt remains a critical tool. 62 percent of land purchases in Illinois required some form of debt financing, with the loan amount averaging 54 percent of the purchase price.

Summary

The 2026 Illinois farmland market continues in a phase of stabilization following several years of unprecedented appreciation. While valuations exhibit projected softening in response to compressed crop margins and elevated operational expenditures, these downward pressures are partially countered by the distribution of ad hoc federal payments. Ultimately, as the market adjusts to current economic headwinds, the farmland sector maintains its fundamental strength and long-term resilience.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.