Middle East Conflict Revives Concerns Over Fertilizer Dependence in the U.S. and Brazil

Four years after the start of the Russia-Ukraine war, which pushed fertilizer prices to historic highs, the current conflict in the Middle East has once again brought attention to the risks associated with dependence on imported fertilizers for agricultural production. With Iran restricting shipping through the Strait of Hormuz, a key route linking the Persian Gulf to global export markets, major supply disruptions have been affecting the United States and Brazil – the world’s two largest country-level fertilizer importers. This article compares fertilizer supply and demand trends over the past five years in both countries, analyzing the scale of their external dependence and the potential implications for agricultural competitiveness.

The Iran War’s Impacts on Global Fertilizer Markets

In 2024, the Strait of Hormuz was one of the world’s most important trade routes for both fertilizer and energy, carrying up to 30% of global fertilizer shipments, about 20% of liquefied natural gas, and 27% of internationally traded oil from the Persian Gulf to markets worldwide (Hebebrand et al., 2026). With Iran now restricting traffic through the waterway in response to attacks by the United States and Israel, prices across energy and fertilizer markets have surged (Arita et al., 2026).

The Persian Gulf region is a big production hub for nitrogen and phosphate. Over the past three years (2023-2025), the Gulf countries were the single largest regional exporter of urea and ammonia (both nitrogen-based) and the second-largest regional exporter of diammonium phosphate (DAP) and monoammonium phosphate (MAP) fertilizers (Hebebrand et al., 2026). Given this scenario, grain-to-fertilizer exchange ratios, or relative fertilizer prices, have remained near multi-year highs since 2022, particularly for nitrogen and phosphorus, both for Brazil and the United States (see farmdoc daily, April 10, 2026).

U.S Reliance on External Fertilizers

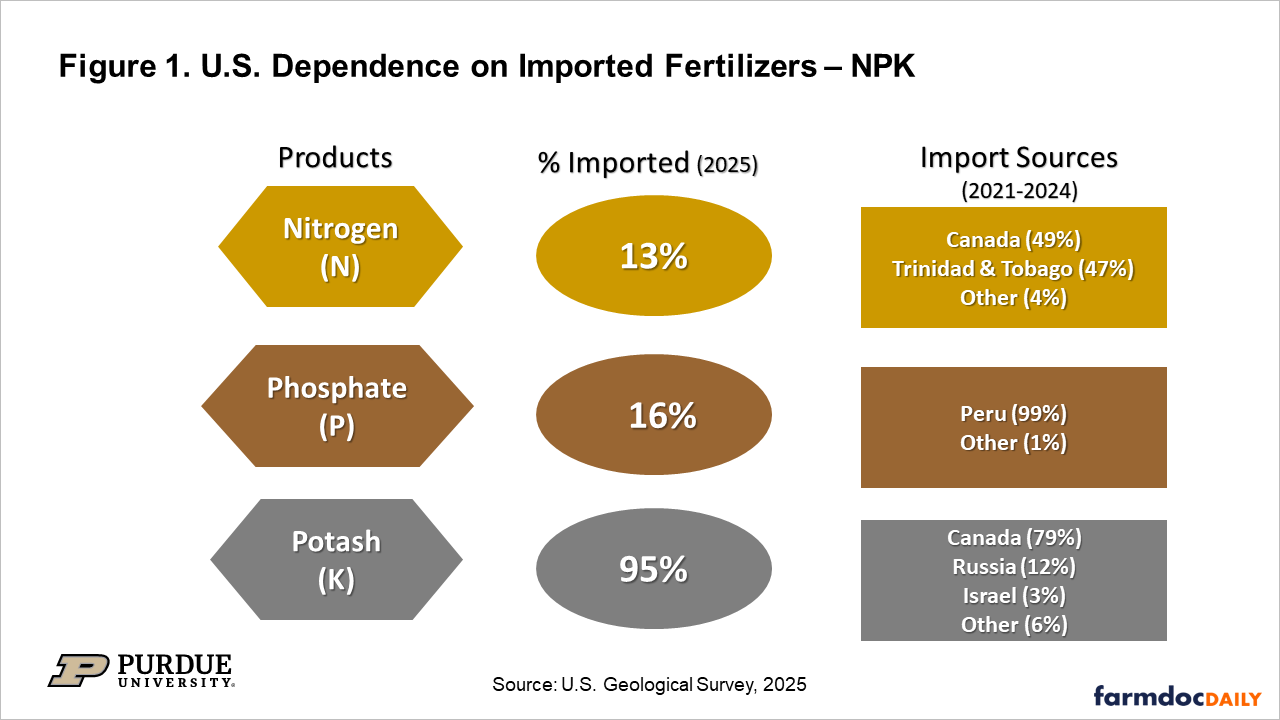

The United States has a strong domestic fertilizer industry, supplying nearly 60% of its demand for the primary macronutrients: nitrogen (N), phosphorus (P), and potassium (K). Even so, it remains exposed to major supply disruptions and sharp increases in fertilizer prices. In 2025, the U.S. imported 95% of its potash requirements, up from 93% in 2021, before the Russia-Ukraine war began (see farmdoc daily, March 17, 2022). From 2021 to 2024, Canada supplied 79% of the potash used in the United States, followed by Russia at 12% and Israel at 3% (see Figure 1).

U.S. dependence on nitrogen and phosphate imports is much lower (see Figure 1). Even so, this dependence has increased since 2021. Reliance on imported phosphate nearly doubled, rising from 9% in 2021 to 16% in 2025, while the share of imported nitrogen in total consumption increased slightly from 12% to 13% over the same period. Another shift over the last five years was the growing dependence on phosphate imports from Peru, which increased from 85% to 99%. There was also a rise in dependence on nitrogen imports from Canada, whose share increased from 30% in 2021 to 49% in 2025.

Brazilian Reliance on External Fertilizers

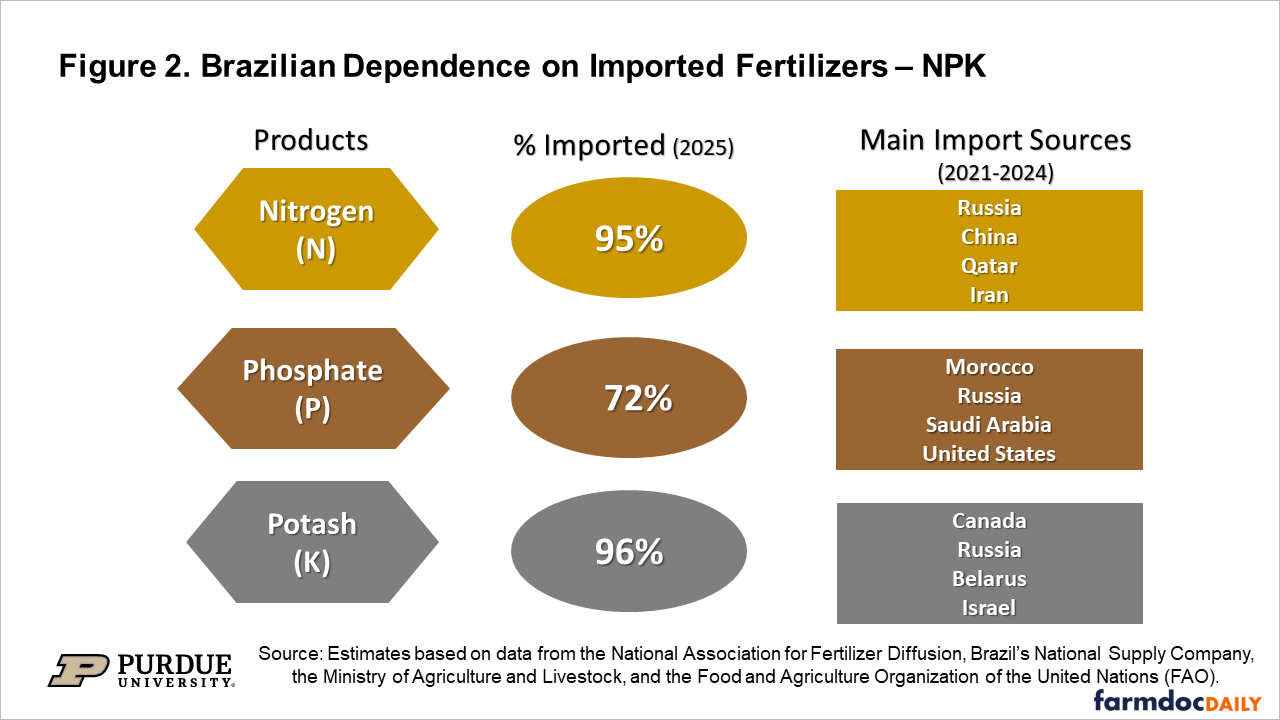

Unlike the United States, Brazil does not have a strong domestic fertilizer industry, despite the scale of its agricultural production. As a result, the country became the world’s largest fertilizer importer in 2024, surpassing the United States, India, and China, according to World Bank data. In 2025, imports accounted for 88% of Brazil’s total fertilizer consumption. Potash is the nutrient for which Brazil is most dependent on foreign supply. The country imports 96% of its potash consumption (see Figure 2), mainly from Canada, Russia, and Belarus. Although Brazil has known potash reserves, commercial-scale production remains limited.

Dependence is also high for nitrogen: 95% of the nitrogen used in Brazilian crop production is imported. Urea, the main source of nitrogen fertilizer, is almost entirely imported. Producing nitrogen fertilizer in Brazil is costly. The most widely used method is the Haber-Bosch process, which turns natural gas and nitrogen from the air into ammonia, the key ingredient in urea (see farmdoc daily, February 17, 2021). The additional challenge is that natural gas has historically been more expensive in Brazil than in major producing countries such as Russia, the United States, and the Middle East, where energy is more abundant and cheaper.

Brazil is the least dependent on imports for phosphate among the three essential fertilizer nutrients. In 2025, Brazil imported 72% of its phosphate needs. The country has significant phosphate rock reserves and exploits them relatively consistently. In 2024, Brazil opened a new mining and industrial complex with the capacity to produce 1 million metric tons of phosphate fertilizers annually for the domestic market alone.

Limited Changes Since the Russia-Ukraine Conflict

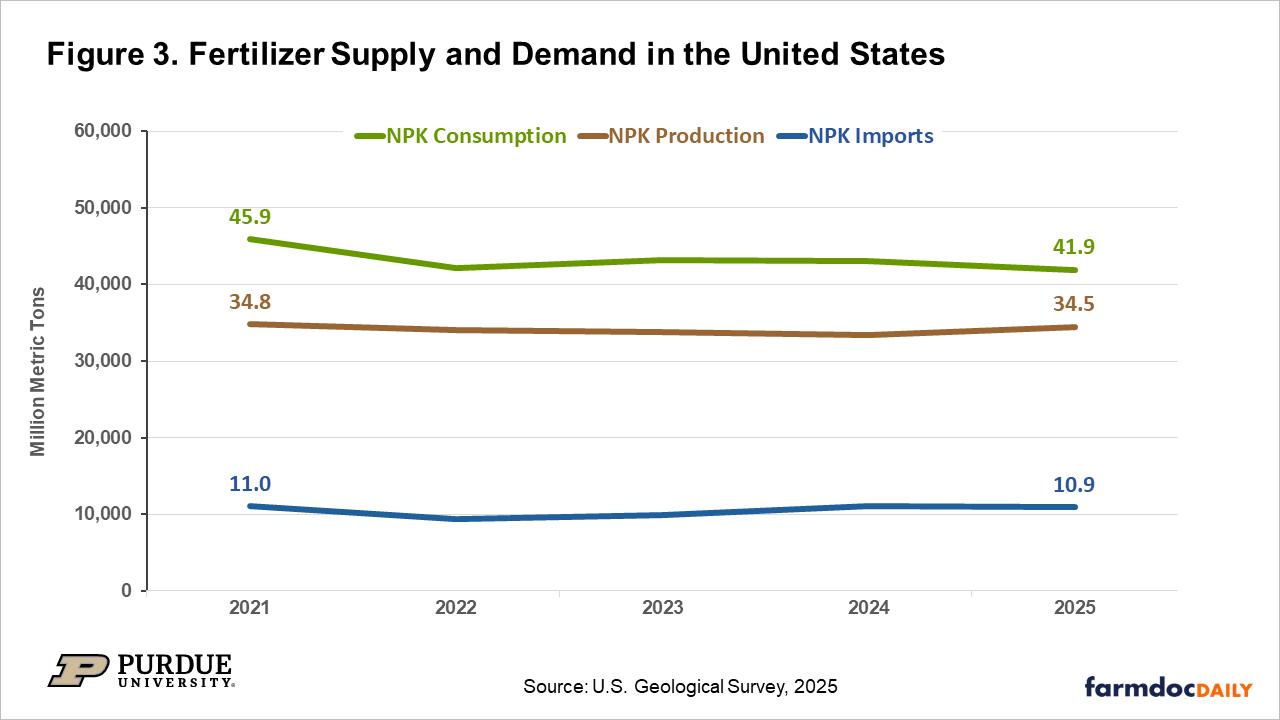

Although both Brazil and the United States released plans in 2022 to reduce their dependence on imported fertilizers after the Russia-Ukraine war disrupted global supply chains, the production outlook has changed little since then. Figure 3 shows that fertilizer supply and demand in the United States remained relatively stable from 2021 to 2025, according to U.S. Geological Survey. NPK consumption declined slightly over the period, from 45.9 million metric tons in 2021 to 41.9 million in 2025, while domestic production stayed close to 34 million metric tons. Imports also remained steady, at around 10 to 11 million metric tons.

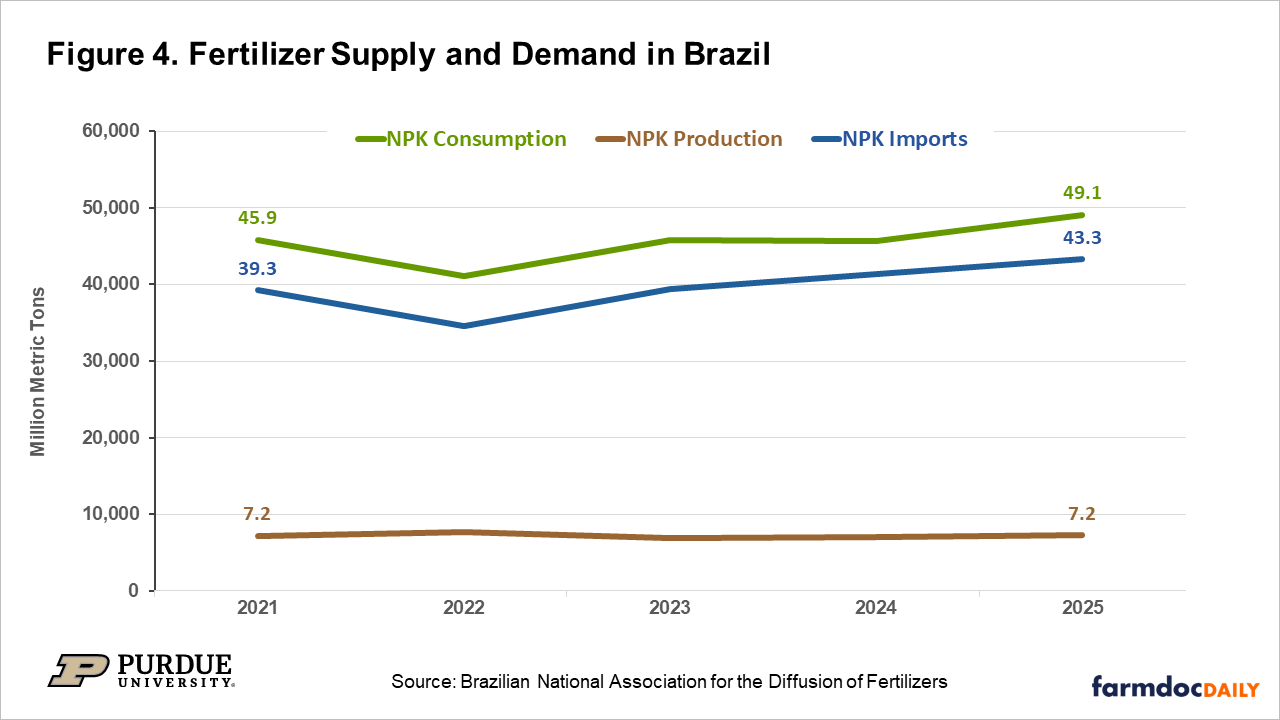

Meanwhile, Brazil became more dependent on imported fertilizers over the past five years. In 2025, a record 49 million metric tons of fertilizer were delivered to the Brazilian market, according to the National Association for the Diffusion of Fertilizers (see Figure 4). This growth mainly reflects the expansion of soybean and corn acreage in recent years (Colussi & Langemeier, 2025). As a result, imports also reached a record 43.3 million metric tons, while domestic fertilizer production remained relatively stable at around 7.2 million metric tons.

Final Considerations

The current conflict in the Middle East has renewed concerns about the vulnerability of agricultural production to disruptions in global fertilizer trade. Brazil remains in a riskier position because import dependence is high across all three primary macronutrients, and domestic production has not kept pace with rising record demand. Although the United States has a more developed domestic fertilizer industry, it also relies on external sources for key inputs, especially potash. This dependence, although at different levels, leaves crop production in both countries exposed to geopolitical shocks, higher input costs, and tighter farm margins.

Moreover, unlike in 2022, when rising input costs coincided with a strong increase in commodity prices, the current situation is characterized by fertilizer price increases with much smaller gains in soybean and corn prices. In the short term, this situation is likely to affect Brazilian producers more strongly, since the soybean fertilizer purchasing window for the 2026/27 crop season is happening right now. In the U.S. Midwest, by contrast, much of the fertilizer for the 2026 crop had already been purchased and/or applied last fall, before the conflict began.

Despite these different impacts, both Brazil and the United States should step up efforts to expand domestic fertilizer production and reduce their exposure to external shocks. This is a long-term challenge, but it is becoming increasingly necessary for both countries to remain competitive in the global grain market. Greater supply security would reduce vulnerability to geopolitical disruptions and provide more stability in input costs for producers.

References

Arita, S., R. Chakravorty, J. Kim, W. Lwin and S. Steinbach. "Strait of Hormuz Closure and Fertilizer Supply Risks for U.S. Agriculture." farmdoc daily (16):48, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 23, 2026.

Colussi, J. and Langemeier, M. “Brazil begins planting with expected record acreage driven by high demand but low margins.” Purdue Center for Commercial Agriculture, October 20, 2025.

Colussi, J., G. Schnitkey and C. Zulauf. "War in Ukraine and its Effect on Fertilizer Exports to Brazil and the U.S." farmdoc daily (12):34, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 17, 2022.

Hebebrand, C., Glauber, J., Vos, R. and Rice, B. “The Iran war’s impacts on global fertilizer markets and food production.” IFPRI Blog, April 1, 2026.

Monaco, H., J. Colussi, G. Schnitkey, N. Paulson, A. Lobo and J. Arromatte. "The Iran Conflict and Fertilizer Markets: Why Brazil Faces Greater Near-Term Risk than the U.S." farmdoc daily (16):62, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 10, 2026.

Sellars, S. and V. Nunes. "Synthetic Nitrogen Fertilizer in the U.S." farmdoc daily (11):24, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, February 17, 2021.

U.S. Geological Survey, 2026, Mineral commodity summaries 2026 (ver. 1.1, March 2026): U.S. Geological Survey, 222 p., https://doi.org/10.3133/mcs2026.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.