Rewriting the RFS Playbook: The Impact of No Half-RIN and Higher RVOs on Projected Biomass-Based Diesel Production and Feedstock Use for 2026-2027

Editorial Note: The data for 2026 and 2027 in the original version of this article for Figure 4 was incorrect. The correct version of Figure 4 was uploaded on March 4, 2026.

Since last June, the U.S. Environmental Protection Agency (EPA) has released a series of decisions regarding implementation of the U.S. Renewable Fuel Standard (RFS) for 2026-2027. We analyzed the impact of these decisions on biomass-based diesel production and feedstock use in a series of farmdoc daily articles (October 29, 2025; November 5, 2025; November 12, 2025). The combined effect of higher renewable volume obligations (RVOs), more restrictive small refinery exemptions, and mandatory reallocation creates substantially higher biomass-based diesel requirements and feedstock use for 2026-2027. A particularly controversial part of the EPA proposals is the limitation of imported biofuel and feedstock to 50 percent of the RINs generated by domestic biofuel and feedstock. There has been widespread reporting in recent weeks that the so-called “half RIN” proposal may be eliminated in the final rulemaking to be issued soon and biomass-based diesel RVOs raised to offset this change. The purpose of this article is to project biomass-based diesel production and feedstock use for 2026-2027 without the half-RIN provision and higher biomass-based diesel RVOs.

Analysis

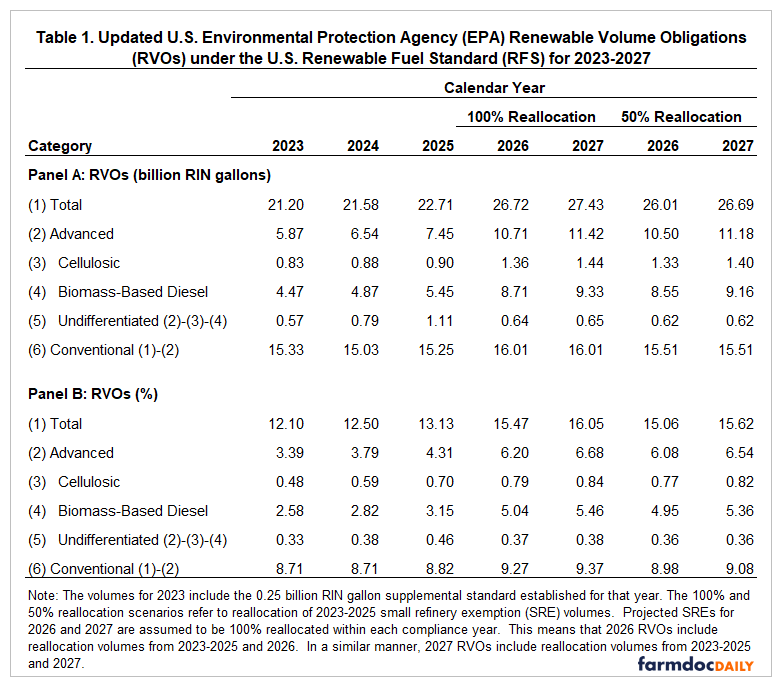

We begin by updating the RVOs for 2026-2027 presented in earlier farmdoc daily articles (October 29; November 5, 2025; November 12, 2025). The RVOs presented in these articles were based on five important EPA rulemakings: i) proposed RVOs for 2026 and 2027 released in June 2025; ii) a comprehensive rulemaking on small refinery exemptions (SREs) over 2016-2024 that was released in July 2025; iii) a reallocation policy framework for small refinery exemptions published in September 2025, iv) a new methodology for projecting obligated petroleum gasoline and diesel volumes released in September 2025, and v) additional SREs granted for 2021-2024 that were announced in November 2025. Two scenarios for reallocation of 2023-2025 SREs in 2026-2027 were presented: 100 percent and 50 percent reallocation. Projected SREs for 2026-2027 were also assumed to be fully reallocated within each compliance year.

The June proposed RVO rulemaking included a provision to lower the RIN value by 50 percent for imported biofuel or biofuel produced domestically with foreign feedstock. The half RIN proposal was controversial from the start, as it dramatically changed the status of imported fuel and feedstock under the RFS. Additionally, the EPA proposed lowering the D4 RIN equivalence value for non-ester renewable diesel from 1.7 to 1.6 RINs per gallon. This change of policy would place FAME biodiesel, which receives 1.5 RINs per physical gallon, on a more equal basis with renewable diesel.

While a final RVO rulemaking has not yet been released by the EPA, there has been widespread reporting in the financial press and on social media about a compromise that would eliminate the half-RIN proposal entirely in exchange for higher biomass-based diesel RVOs. For example, on a recent quarterly earnings call, Robert Day, Chief Financial Officer of Darling Ingredients, stated, “So, I’ll go on record saying we support an RVO for advanced biofuels that translates to 5.25 billion gallons or 5.61 billion gallons.” In addition, it appears that the proposal to discount non-ester renewable diesel from 1.7 to 1.6 RINs will be delayed until 2027.

The updated RVOs for 2026 and 2027 in Table 1 assume that the 2026 and 2027 biomass-based diesel RVOs will be set at 5.25 and 5.61 billion physical gallons, respectively, consistent with recent reporting. Using an average equivalence value of 1.6, this converts to 8.4 billion RIN gallons for 2026 and 8.976 billion gallons for 2027. The biomass-based diesel RVOs shown in Panel A of Table 1 for 2026 and 2027 (row 4) are slightly larger because a small amount of reallocation volumes from 2023-2025 are included in the totals. In addition, we assume that the equivalence value for non-ester renewable diesel drops from 1.7 to 1.6 RINs in 2027. Note that the RVOs shown on Panel A of Table 1 are presented in billions of RIN gallons.

The next step in the analysis is to compare the updated biomass-based diesel RVOs to those in the June proposed rulemaking from the EPA. To facilitate comparison, we convert the updated and June biomass-based diesel RVOs to billions of physical gallons using, once again, an average equivalence value of 1.6:

This indicates that the updated biomass-based diesel RVOs are about 20 percent higher than the June levels. In essence, the increase can be viewed as compensation to the U.S. domestic biomass-based diesel industry for the elimination of the half-RIN penalty for imported biofuel and feedstock. A key question is whether this tradeoff is favorable or unfavorable for participants in the domestic biomass-based diesel market.

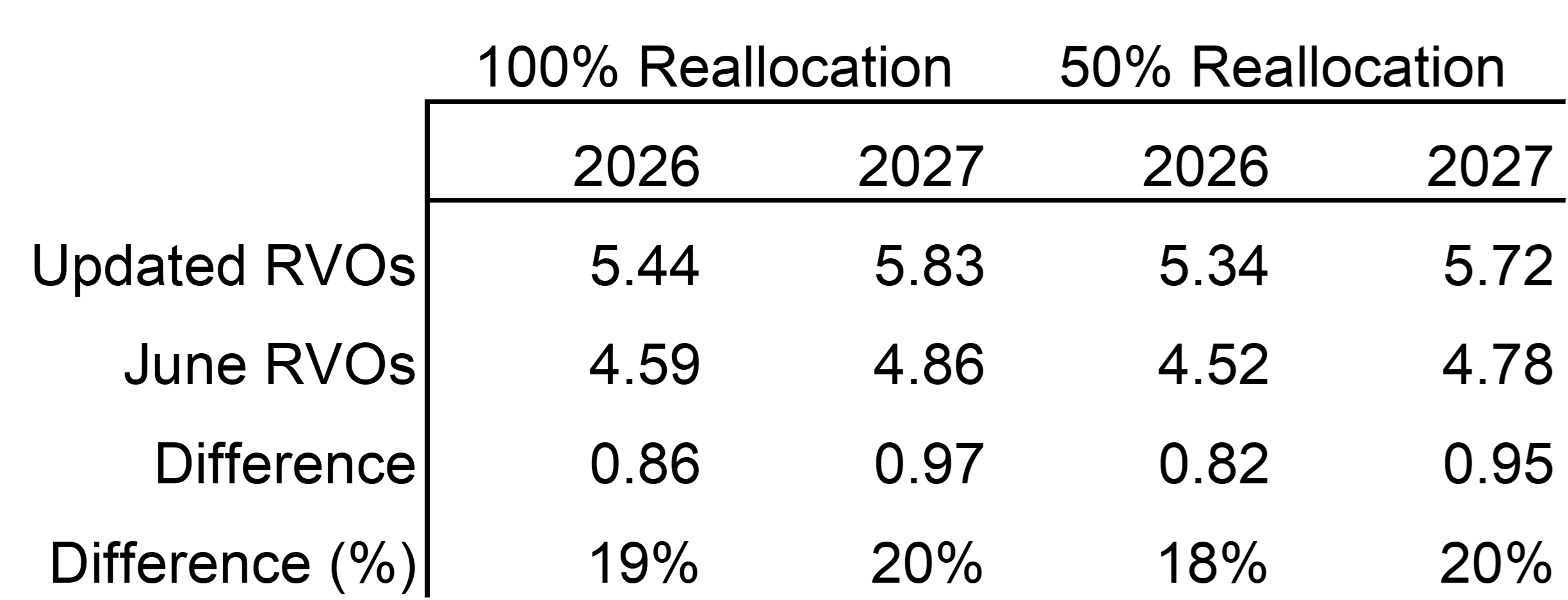

In order to analyze the tradeoffs, we must first project the impact on required D4 RIN generation over 2026-2027. We follow the same procedures as in our previous farmdoc daily articles (November 5, 2025; November 12, 2025; November 24, 2025) with the exception of the updated RVOs shown in Table 1 and other data for 2025 that has also been updated. The updated D4 RIN balance sheet shown in Table 2 reveals that D4 generation over 2023-2025 averaged 7.92 billion (RIN) gallons. This compares to an average of 9.44 billion gallons across the two reallocation scenarios for 2026 and 12.03 billion gallons for 2027. These translate into a 19 percent increase in required D4 RIN generation in 2026 and a 52 percent increase in 2027. Both are substantial increases in required RIN generation over a relatively short period of time. It is also important to emphasize that the estimates of D4 RIN generation shown in Table 2 are independent of developments in physical biomass-based diesel markets. The projections of D4 generation can be thought of as fixed targets that can be met by a wide variety of combinations of domestic and imported physical biomass-based diesel production. The key is that physical biomass-based diesel volumes must add up to the D4 RIN generation requirements (after appropriate weighting), not the other way around.

Another important result to highlight in Table 2 is the explosion in the ending D4 RIN bank to an unprecedented 3.0 billion gallons in 2024—over three times the previous 2016 peak. This massive accumulation resulted from RIN generation substantially outpacing obligations during 2023-2024 after accounting for SREs. The bank declines to 1.8 billion gallons in 2025, but this is still extremely large by historical standards. This enormous RIN bank provides a substantial buffer as the market transitions to higher RVOs in 2026-2027. Obligated parties can draw down the bank to help meet compliance obligations, blunting the immediate impact on physical biomass-based diesel production and feedstock use. The backloading effect due to the RIN bank was discussed in a previous farmdoc daily article (November 24, 2025).

We can now turn to the task of estimating physical biomass-based diesel production and feedstock use in 2026-2027 under the updated RVOs. We do this in three steps:

- We assume that FAME biodiesel and renewable diesel fuel imports in 2026 and 2027 will be twice the level of 2025, unless larger imports are required due to domestic production reaching 100 percent of capacity. Imports of both biodiesel and renewable diesel fell sharply in 2025 with the conversion of the blenders tax credit to the new 45Z tax credit. This assumption allows a rebound in fuel imports due to the higher RVOs in 2026 and 2027.

- We then solve for the biomass-based diesel capacity utilization rate that generates the required number of D4 RINs in 2026 and 2027, net of fuel imports. This assumes the same domestic capacity utilization rate for FAME biodiesel and renewable diesel within each year. FAME biodiesel operable capacity is assumed to be 1.958 and 2.285 billion (physical) gallons in 2026 and 2027, respectively. The capacity for 2026 is assumed to be the latest operable capacity estimate available from the EIA (November 2025). The higher capacity in 2027 reflects an assumption that much of the production taken offline in the last few years will be incentivized to come back into production. Renewable diesel operable capacity in both 2026 and 2027 is assumed to be 5.015 billion (physical) gallons. The capacity for 2026 and 2027 is also assumed to be the latest operable capacity estimate available from the EIA (November 2025).

- We allocate domestic production of FAME biodiesel and renewable diesel into two components—domestic production from domestic feedstock and domestic production from imported feedstock. We had previously estimated these two shares for FAME biodiesel in 2024 to be 81 and 19 percent, respectively. Likewise, the shares for renewable diesel in 2024 were estimated to be 56 and 44 percent, respectively. We assume that the share of imported feedstock will be moderately lower in 2026-2027 due to the disincentives provided by the 45Z restriction of North American feedstocks only, the likelihood of continuing additional tariffs on goods like biofuel feedstocks, and potential logistical constraints on importing larger volumes of animal fats such as tallow and white grease. Specifically, we assume that the two shares for FAME biodiesel in 2026-2027 will be 85 and 15 percent, respectively. Likewise, the shares for renewable diesel in 2026-2027 are assumed to be 66 and 34 percent, respectively.

In the following set of comparisons, we use average values for 2023-2025 as a benchmark to smooth fluctuations during this period. In addition, we average results across the 100 percent and 50 percent reallocation scenarios for 2026 and 2027 to simplify comparisons. Taking an average in this manner is the same thing as assuming 75 percent reallocation.

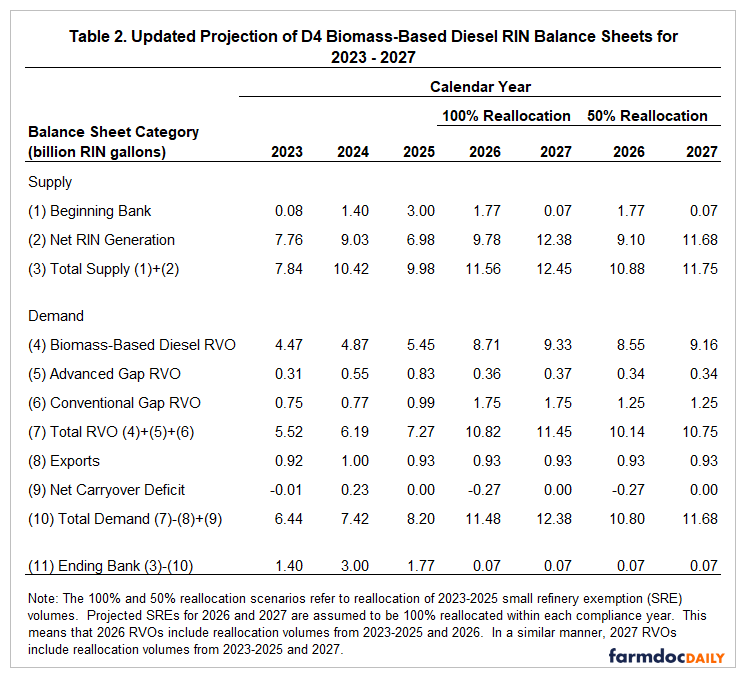

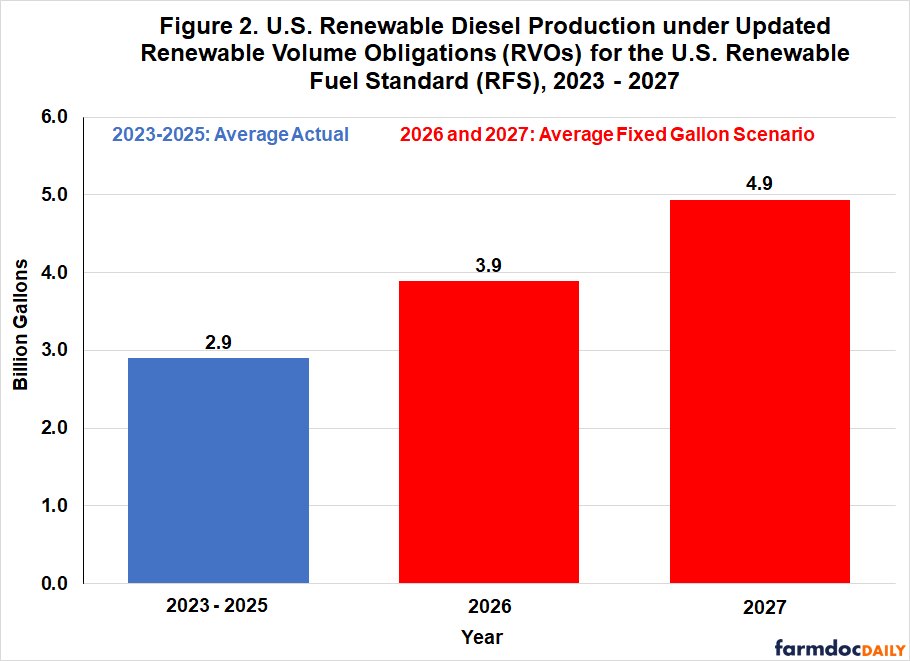

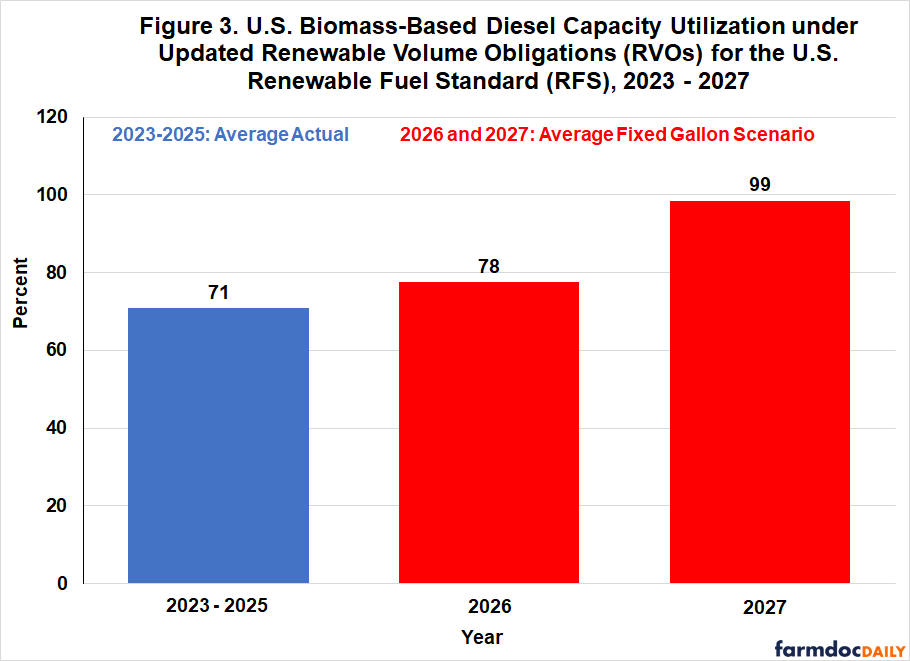

Figure 1 shows that FAME biodiesel production under these assumptions is flat at 1.5 billion gallons in 2026 compared to the 2023-2025 average. This comparison masks the fact that biodiesel production was down sharply in 2025 compared to 2023 and 2024. Compared to 2025, FAME production in 2026 is projected to increase 300 million gallons. Consistent with the large increase in required D4 RIN generation shown in Table 2, biodiesel production jumps sharply in 2027 to 2.3 billion gallons. Figure 2 shows that renewable diesel production increases a billion gallons per year in both 2026 and 2027. This is the result of a lower average capacity utilization rate for renewable diesel over 2023-2025 compared to biodiesel. Figure 3 shows the biomass-based diesel capacity utilization rate that is necessary for domestic production to meet the required D4 RIN generation. Capacity utilization increases moderately from 71 percent in 2023-2025 to 78 percent in 2026 and then increases sharply to 99 percent in 2027. For all practical purposes, domestic biomass-based diesel production in 2027 is required to be at full capacity.

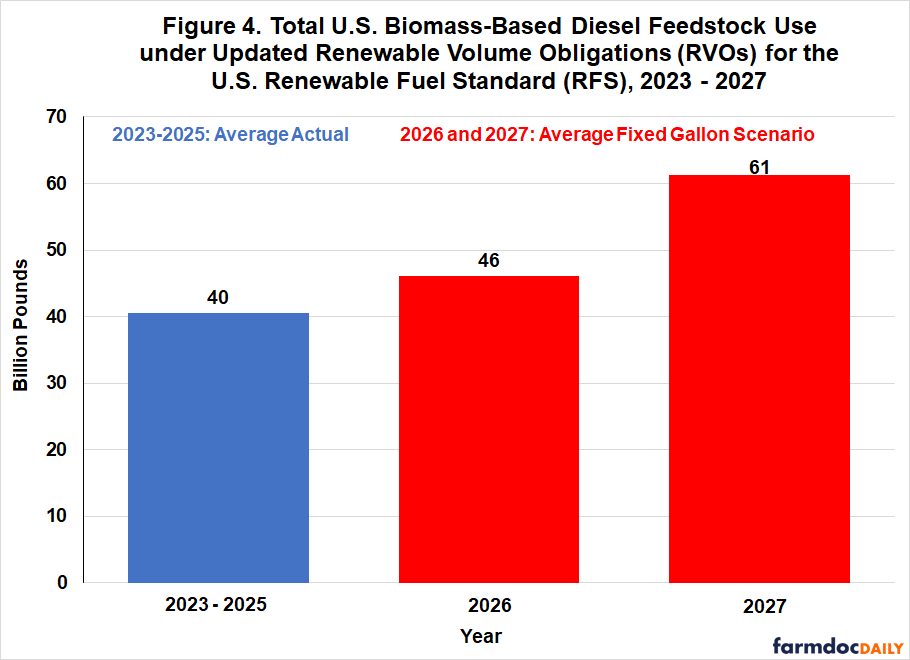

We calculate feedstock requirements using 7.55 pounds per gallon for biodiesel and 8.25 pounds per gallon for renewable diesel. These assumptions result in a weighted average of 8.0 pounds per gallon over 2023-2025, very close to the 7.96 rate implied by EIA’s survey measures of biomass-based diesel feedstock use. Figure 4 shows total feedstock use when domestic fuel, domestic feedstock, imported fuel, and imported feedstock are combined. The 2023-2025 baseline averaged 40 billion pounds annually, which then rises to 46 billion pounds in 2026 and 61 billion pounds in 2027. The increase in feedstock use for 2026 compared to 2023-2025 is 6 billion pounds, and this rises another 15 billion pounds in 2027. The total increase of 21 billion pounds is an increase of 53 percent relative to the 2023-2025 benchmark.

The 2026 and 2027 estimates of total feedstock use are large in absolute terms and comparable to our earlier estimates under the half-RIN proposal, which were 48 billion pounds in 2026 and 59 billion pounds in 2027 (farmdoc daily, November 24, 2025). This indicates that the increase in the updated RVOs translates into total feedstock demand that is about the same as under the half-RIN proposal.

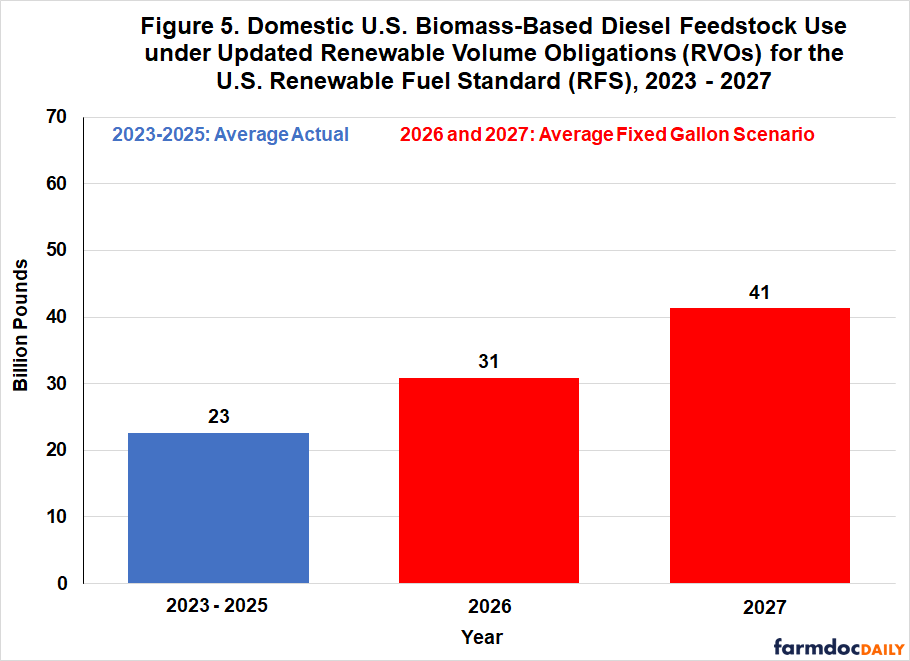

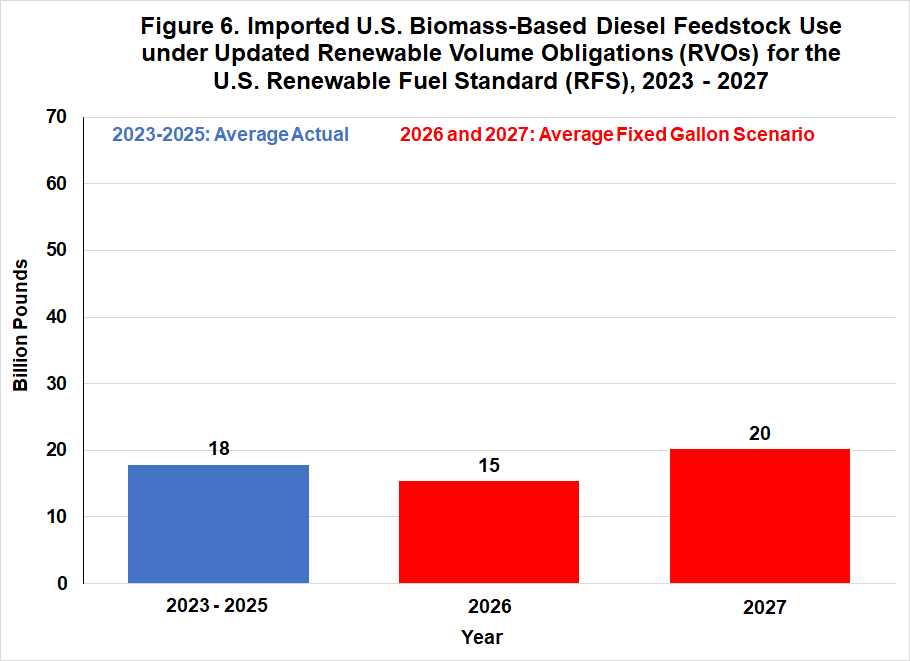

The remaining key question is how this larger feedstock demand is distributed between domestic and imported feedstock suppliers. Figure 5 shows total domestic feedstock use for the 2023-2025 baseline averaged 23 billion pounds and then increases to 31 billion pounds in 2026 and 41 billion pounds in 2027. The increase in feedstock use for 2026 compared to 2023-2025 is 8 billion pounds, and this increases another 10 billion pounds in 2027. The total increase of 18 billion pounds represents a jump of 78 percent relative to the 2023-2025 benchmark. As impressive as these increases appear, it is important to note that they are substantially smaller than our earlier projections under the half-RIN proposal, which were 38 billion pounds in 2026 and 49 billion pounds in 2027. The loss of the disincentive provided by the half-RIN drives domestic feedstock use down by 8 billion pounds each year, or about 20 percent. Not surprisingly, Figure 6 shows that import feedstock suppliers are the main beneficiary of dropping the half-RIN. Import feedstock demand actually increases by 2 billion pounds when comparing 2027 to 2023-2025. As would be expected, the 8-billion-pound loss to domestic feedstock suppliers approximately equals the gain to import suppliers.

It is important to recognize that our assumptions for imported feedstock shares drive the reduction in domestic feedstock usage in the analysis. We assumed that the share of imported feedstocks is constant in 2026 and 2027 and only moderately below the level of 2024 and 2025. Key policy prescriptions, like 45Z, may reduce imported feedstock shares during 2026 and 2027 more than we assume and create incentives for domestic feedstock usage to maximize the revenue from the policy stack (e.g., LCFS credits). However, price differentials between domestic and foreign feedstock along with sourcing issues for low carbon intensity feedstock will also play a key role in the evolution of the feedstock markets under the updated RVOs. This is a significant area of uncertainty moving forward that will have to be monitored closely.

The magnitude of the projected feedstock demand under the updated RVOs warrants additional consideration. A recent USDA analysis (Bukowski, Swearingen, and Hubbs, February 2025) estimated total global supply of biomass-based diesel feedstock at 129 billion pounds for 2023-24. Our estimate of total feedstock demand in 2027 of 61 billion pounds is 47 percent of the USDA estimate of global supply. Our estimate of domestic feedstock demand in 2027 of 41 billion pounds is 51 percent of the USDA estimate of U.S. domestic supply. These comparisons provide only rough indicators, as feedstock supplies will likely respond to higher prices, and not all available feedstock currently flows to biomass-based diesel. Nevertheless, the scale of the 2027 increase suggests substantial adjustment pressures, particularly for animal fats and used cooking oil markets serving renewable diesel production. The soybean oil market is also likely to see sharply higher biofuel demand, with potential spillover effects on vegetable oil prices broadly.

Implications

Proposals have recently surfaced to eliminate the half-RIN provision from the final EPA renewable volume obligation (RVO) rulemaking for 2026-2027 in exchange for higher fixed biomass-based diesel requirements. This represents a potentially consequential policy tradeoff with meaningfully different implications for domestic and import market participants. The higher RVOs do indeed benefit the domestic biomass-based diesel industry, with total capacity utilization effectively reaching 100 percent in 2027 under the updated RVOs. Total feedstock demand of 46 billion pounds in 2026 and 61 billion pounds in 2027 is comparable to our earlier projections under the half-RIN proposal, which were 48 and 59 billion pounds, respectively. However, the distribution of feedstock demand changes. By dropping the half-RIN disincentive on imported feedstock, domestic feedstock suppliers lose approximately 8 billion pounds of demand per year, a reduction of about 20 percent compared to what they would have received under the half-RIN regime. This loss flows directly to import suppliers, who emerge as one of the main beneficiaries of the policy compromise. In essence, by dropping the half-RIN, the domestic biomass-based diesel industry would secure higher volume mandates but at the cost of redirecting feedstock demand towards import suppliers. Whether this tradeoff is favorable depends critically on which segment of the domestic industry one considers. Biofuel producers benefit from higher RVOs and the certainty that the half-RIN’s complex import accounting will not be imposed on them, while domestic feedstock suppliers of animal fats, used cooking oil, and soybean oil will face a meaningfully smaller share of the total feedstock demand increase than would otherwise have been the case. The supply-side challenge remains formidable regardless of the policy framing. The scale of the required adjustment—a 53 percent increase in total feedstock demand relative to the 2023-2025 average—leaves very little margin for error from either production disruptions or demand-side uncertainties.

References

Bukowski, M., B. Swearingen, and T. Hubbs. “Special Article: Estimating Biomass-Based Diesel Feedstock Availability in Marketing Years 2018/19-2023/24.” Oil Crops Outlook, U.S. Department of Agriculture, Economic Research Service, Situation and Outlook Report, February 2025. https://ers.usda.gov/sites/default/files/_laserfiche/outlooks/110935/OCS-25b.pdf?v=96817

Hubbs, T. and S. Irwin. "Rewriting the RFS Playbook: Revised RVOs Backload Projected Biomass-Based Diesel Production and Feedstock Use into 2027." farmdoc daily (15):217, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 24, 2025.

Hubbs, T. and S. Irwin. "Rewriting the RFS Playbook: The Impact of Revised RVOs on Projected Biomass-Based Diesel Production and Feedstock Use for 2026-2027." farmdoc daily (15):209, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 12, 2025.

Hubbs, T. and S. Irwin. "Rewriting the RFS Playbook: The Impact of Revised RVOs on Projected D4 Biomass-Based Diesel RIN Generation for 2026-2027." farmdoc daily (15):204, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 5, 2025.

Hubbs, T. and S. Irwin. "Rewriting the RFS Playbook: The Impact of Recent EPA Decisions on 2023-2027 RVOs for Biomass-Based Diesel." farmdoc daily (15):199, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 29, 2025.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.