Middle East Ceasefire Fails to Ease U.S. Fertilizer Price Pressure on Farmers

When the April 8 ceasefire was announced, oil prices dropped below $100 per barrel as crude markets priced out part of the war risk premium (see Reuters). However, U.S. nitrogen fertilizer prices have yet to follow. Retail prices for urea, anhydrous ammonia, and UAN solutions kept climbing through mid-April, as shipping through the Strait of Hormuz remained far below pre-conflict levels and insurance barriers continued to deter shipowners from returning to the route. Today’s article examines recent shipping data through the Strait of Hormuz, weekly U.S. retail fertilizer prices, and survey evidence on how farmers across the nation are experiencing the price shock.

Why Hormuz Matters for Fertilizer Markets

The Strait of Hormuz is the world’s most important oil transit chokepoint (see IEA). The International Energy Agency (IEA) estimates that an average of 20 million barrels per day of crude oil and oil products moved through the Strait in 2025, representing roughly one-quarter of global seaborne oil trade. More importantly for agriculture, nearly all liquefied natural gas (LNG) exported from Qatar and the United Arab Emirates transits the waterway. Because natural gas serves as both the primary feedstock and the energy source for manufacturing nitrogen fertilizers, bottlenecking this single corridor directly threatens global fertilizer supplies. Beyond the natural gas connection, roughly one-third of global seaborne fertilizer volumes pass through the waterway, with those shipments heavily concentrated in urea (67%) and DAP (20%) in 2024 (see UNCTAD). Additionally, the surrounding Gulf region is also a major producer of sulfur that is used for phosphatic fertilizers.

Shipping Through Hormuz Remains Far Below Normal

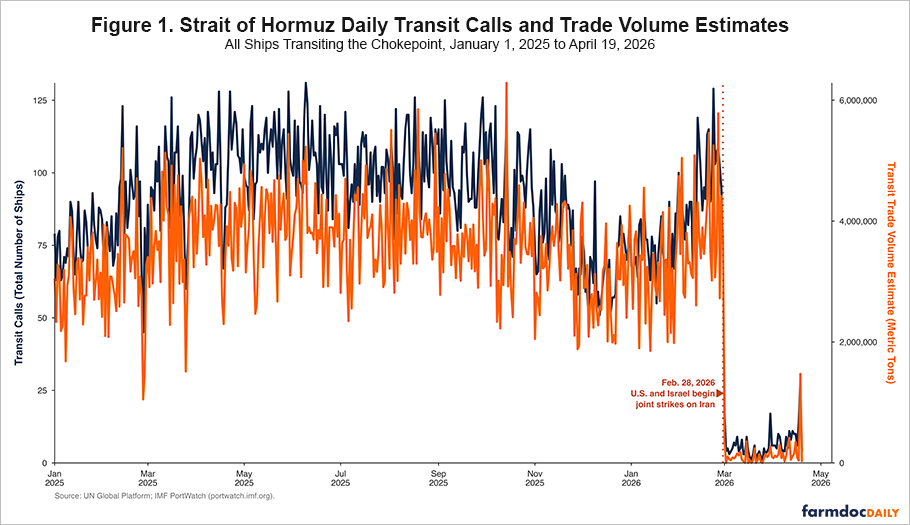

Figure 1 shows how sharply traffic through the Strait of Hormuz collapsed after February 28, 2026, using IMF PortWatch data that tracks both the number of vessels passing through (transit calls) and the physical weight of the cargo they carry (estimated trade volume) (see PortWatch). Between January 1 and February 27 of this year, an average of 84.1 ships passed through the Strait each day. From February 28 through April 7—the period from the start of the conflict to the ceasefire announcement—that average fell to just 7.2 ships per day. The total amount of cargo moving through the corridor collapsed similarly, plummeting from an estimated 3.44 million metric tons per day before the conflict to about 0.20 million metric tons during the fighting. Those changes represent severe declines of 91.5% in daily ship traffic and 94.2% in the actual volume of goods traded.

Conditions improved after the ceasefire, but the improvement was modest. Between April 8 and April 19, average daily vessel calls through the Strait increased slightly to 10.1 and estimated daily trade volume rose to roughly 0.26 million metric tons. To put that in perspective: ship traffic remained 88.0% below pre-conflict averages, and trade volume remained 92.4% below. S&P Global reported that market participants flagged three immediate concerns: the ceasefire was set to expire on April 22, insurance remained a barrier for most shipowners, and three ammonia vessels were still stuck west of the Strait (see S&P Global). As one ammonia shipbroker put it, “shipowners may take the view that the ceasefire needs to be extended beyond the initial two weeks. They don’t want to take the risk of sailing in, only to get stuck if the situation deteriorates.” President Trump subsequently extended the ceasefire on April 21, with no fixed end date, though the U.S. naval blockade remains in place (see Reuters).

Fertilizer Prices Continued to Move Higher

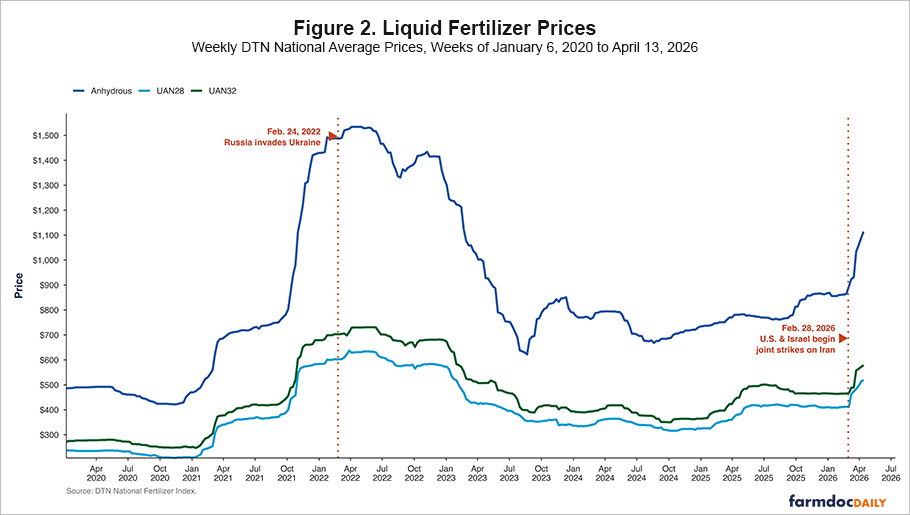

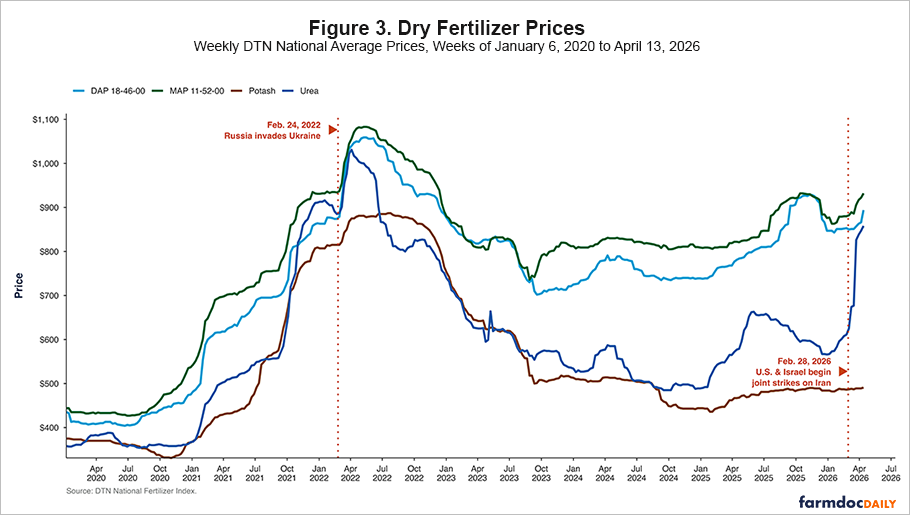

Figures 2 and 3 use DTN weekly retail fertilizer prices to show that the 2022 price spike began well before Russia’s invasion of Ukraine. Prices were already rising sharply through 2021 due to higher natural gas costs, COVID-related supply disruptions, and tightening global supplies. By mid-February 2022, urea, DAP, MAP, and potash had increased between 72% and 142% compared to early 2021, and anhydrous ammonia had reached $1,488 per ton. Russia’s invasion added additional upward pressure, particularly for nitrogen and phosphate products, pushing prices higher into April 2022. Prices declined from their peaks through mid-2023, though unevenly across products. By 2024, fertilizer prices had stabilized but remained above pre-pandemic levels. In 2025, prices for key products began rising again, and the Iran conflict accelerated that trend sharply by disrupting global fertilizer trade and energy markets.

Figure 2 shows some of the retail prices for the liquid fertilizers tracked in the DTN series. By the week of April 13, 2026, anhydrous ammonia had a national average of $1,114 per ton, UAN32 averaged $579, and UAN28 averaged $520. Those prices were up 29.2%, 24.5%, and 26.2%, respectively, from the week of February 16. Compared to a year ago, anhydrous ammonia is up 42.6%, UAN28 36.8%, and UAN32 29.2%. However, the ceasefire brought no immediate relief: in the first full week after the announcement, UAN28 and UAN32 increased by 1.4% and 1.2%, respectively, while anhydrous ammonia rose 2.4%.

Figure 3 shows national average retail prices for urea, DAP, MAP, and potash. Urea has seen the sharpest price increase since the conflict broke out. Natural gas is the primary feedstock for urea production, making urea prices directly sensitive to supply disruptions. Furthermore, the U.S. has a moderate dependence on Gulf fertilizer supply with 17% of U.S. urea consumption and 20% of U.S. DAP/MAP consumption coming from the Persian Gulf in 2023, while potash exposure was negligible (see farmdoc daily, March 23, 2026). For the week of April 13, 2026, urea averaged $858 per ton, up 41.1% from the week of February 16 and 48.7% from a year earlier. DAP and MAP rose more modestly, increasing 4.9% and 5.9% from the week before the conflict. DAP was up 14.5% compared to a year ago, while MAP was up 13.4%. However, potash changed very little. At $491 per ton, it was up just 0.8% from the week before the conflict and 5.1% from a year ago.

What This Means for Farmers

Pre-booking has softened the immediate hit for some farmers, especially in the Midwest, but it has not eliminated the problem. A recent Farm Bureau survey found that 67% of Midwestern respondents had secured fertilizer ahead of the season, compared with 19% in the South, 30% in the Northeast, and 31% in the West (see Farm Bureau). That still left nearly one in three Midwestern respondents entering the season without all fertilizer needs secured. Affordability remains an issue as well. Nationally, about 70% of respondents said they could not afford all the fertilizer they needed. The share was lower in the Midwest, but still substantial, at 48%.

Current exposure to unbooked fertilizer matters because nitrogen is one of the largest variable costs in corn production. In Illinois, 2026 nitrogen recommendations ranged from about 180 to 200 lb per acre (see farmdoc daily, August 12, 2025). Recent price increases across nitrogen fertilizers translate directly into higher per-acre costs.

For example, for anhydrous ammonia (82% N), a $252 per ton increase is equivalent to $0.126 per lb of product ($252 ÷ 2,000). Supplying 180–200 lb of nitrogen requires about 220–244 lb of product, implying an added cost of roughly $28 to $31 per acre. Similar calculations for other nitrogen sources show comparable increases. UAN32 implies an increase of about $32 to $36 per acre, UAN28 about $35 to $39 per acre, and urea roughly $49 to $54 per acre at typical application rates.

In a tight margin environment, those increases are meaningful. Across products, recent nitrogen price increases are adding roughly $30 to $55 per acre to corn production costs, raising breakeven prices and narrowing already thin margins. With futures near $4.60 and a -$0.30 harvest basis, the implied cash price is about $4.30 per bushel, meaning recent nitrogen cost increases are equivalent to roughly 7 to 13 bushels per acre.

Summary

Despite the April 8 ceasefire, traffic through the Strait of Hormuz has not returned to pre-conflict levels, as shipowners and insurers continue to approach the route cautiously. For agriculture, the effects of this disruption are most evident in nitrogen fertilizer prices. In the U.S., urea was up 41.1% from the week of February 16, while anhydrous ammonia was up 29.2%. These increases have made navigating planting season especially challenging for farmers. In an American Farm Bureau Federation survey, about 70% of respondents reported that they could not afford all the fertilizer they needed. Pre-booking may have softened the price shock for some farmers, especially in the Midwest, but many remain exposed. At current market levels, these fertilizer price increases are adding roughly $30 to $55 per acre in nitrogen costs, equivalent to about 7 to 13 bushels of corn per acre.

References

Arita, S., R. Chakravorty, J. Kim, W. Y. Lwin and S. Steinbach. "Strait of Hormuz Closure and Fertilizer Supply Risks for U.S. Agriculture." farmdoc daily (16):48, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 23, 2026.

IEA. “Strait of Hormuz.” Factsheet, February 2026.

IMF PortWatch. “Daily Chokepoint Transit Calls and Trade Volume Estimates.”

Paulson, N., G. Schnitkey, H. Monaco and C. Zulauf. "Fertilizer Decisions for the 2026 Crop Year." farmdoc daily (15):145, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, August 12, 2025.

Parum, F. “Farm Bureau Survey Reveals Real Impact of Fertilizer Availability and Price.” American Farm Bureau Federation Market Intel, April 14, 2026.

Menon, P., Jose, J., and Masoni, D. Reuters. “Global energy stocks plunge as US-Iran ceasefire hits oil.” April 8, 2026.

Holland, Steve, Enas Alashray, and Mubasher Bukhari. “US announces ceasefire extension with Iran.” Reuters, April 21, 2026.

UNCTAD. “From gas to grain: Fertilizer disruptions raise risks for food security and trade.” UN Trade and Development, March 30, 2026.

Warner, T., and Gorman M. “Muted reaction in fertilizer markets to Strait of Hormuz reopening.” S&P Global Energy, April 17, 2026.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.