Will Brazil’s Corn and Soybean Production Continue to Grow in 2027?

Brazil, the world’s largest soybean producer and a major corn exporter, faces production challenges in the upcoming 2027 crop year. Low commodity prices, high fertilizer costs, difficult credit conditions, and the likelihood of El Niño-related extreme weather all factor into Brazil’s production prospects. While these issues are not unique to Brazil, they are likely to have their largest and most immediate impact on global agricultural commodity supply there. U.S. crop acreage and input decisions for 2026 are now essentially set and U.S. growing season weather has thus far been conducive to crop development. Indeed, some have questioned whether Brazilian soybean and corn production will continue to grow in 2027 (Sousa 2026).

Lower Brazilian crop production would buck historical trends. For the past fifteen years, growth in Brazil’s expected soybean and corn output, as measured by pre-planting production forecasts, has been steady. Average annual expected production increases are about 6.5% for both crops. Recently released USDA production forecasts for the 2026-27 marketing year show essentially similar growth for Brazil in 2027. If realized, forecast production levels of both crops would exceed estimated levels for 2026, which are already historic records.

This article documents both the long-run production trends and short-run production challenges for corn and soybeans in Brazil. It scrutinizes initial production forecasts from the USDA for 2027 corn and soybean production in Brazil, which appear to be much more in line with long-run trends than with a productive retreat on the part of Brazilian farmers. While it may be tempting to forecast lower production now, Brazilian farmers have increased production in the past even when economic conditions have been difficult. Weather-driven supply shocks rather than farmer-driven production decisions explain more year-to-year variation in production. Continued growth in Brazilian crop supply would further dampen the prospects for high commodity prices needed to boost farm profitability in the United States.

Long-Run Production Trends and Current Forecasts

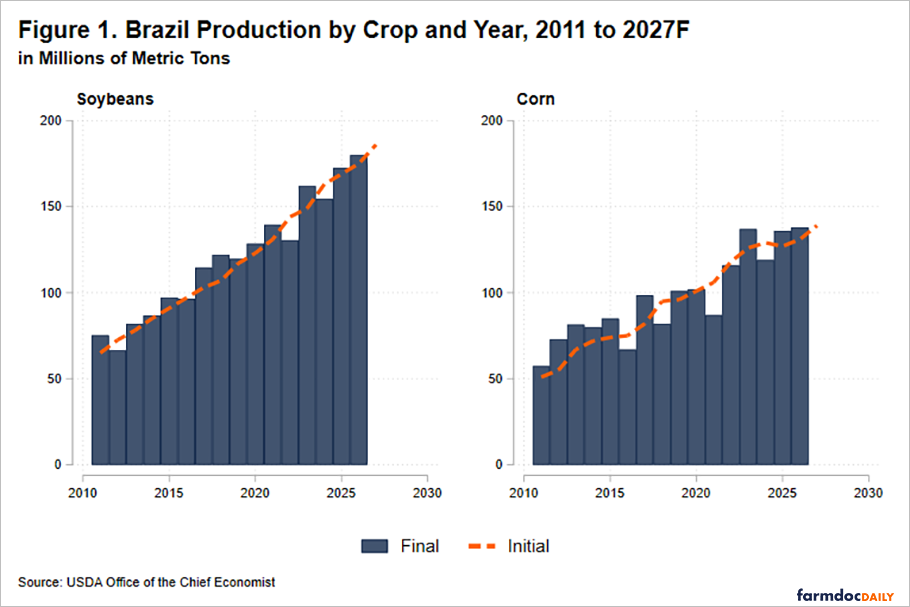

Figure 1 plots realized Brazilian production as reported by USDA against initial forecasts for soybeans and corn since 2011. Three features stand out. First, production has grown steadily. Final soybean output has climbed from roughly 75 million metric tons (MMT) in 2011 to 180 MMT in 2026, while corn production has risen from about 57 MMT to 138 MMT. Growth has been more consistent than episodic, averaging nearly 6.5% per year over the past fifteen years. That trend held even through the mid-2010s price collapse: Brazil’s production routinely hit records during this period, with the notable exception of 2016 when El Niño crop losses shrank yield and production.

Second, the initial forecasts rise steadily over time for both crops. USDA’s procedure for generating production forecasts is essentially one of linear growth, especially for soybeans. Simply, USDA forecasters have not made dramatic changes to production forecasts based on current economic conditions. Forecasts for 2027 production follow this procedure, with the recently released initial soybean production forecast 6.1% higher and the initial corn forecast 6.2% higher than the initial forecasts from one year ago. If realized in 2027, both levels would be production records for Brazil.

Finally, the initial forecasts have themselves been reliable guides to eventual production. Pre-planting expectations rarely diverge far from final outcomes, and where they do, the gaps reflect within-season surprises rather than persistent forecast bias. Against this backdrop, the newly released 2027 forecasts are unremarkable: both crops are projected to extend their long-run trajectories. A production decline in 2027 would be the historical exception, not the rule.

Decomposing Growth: Area and Yield

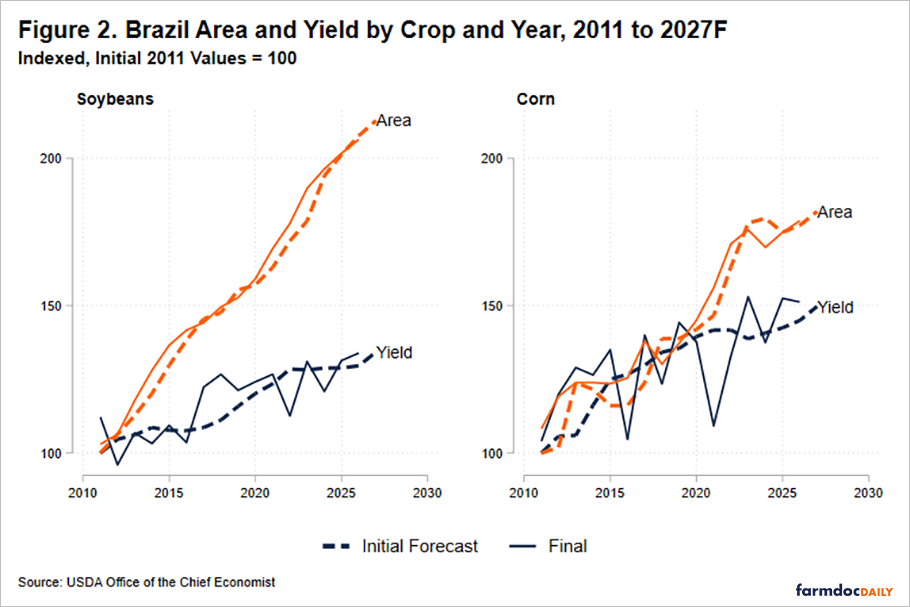

Production is the product of harvested area and yield. Figure 2 indexes each component to its 2011 value to show how the two components have evolved over time. For both crops, area expansion has been the primary and most consistent driver of growth. Soybean area has more than doubled since 2011, rising steadily with little interruption; corn area has increased by roughly three-quarters. This sustained expansion reflects deliberate, ongoing investment by Brazilian farmers and these decisions that have continued even through periods of low prices and tight margins. For instance, area kept setting records through the mid-2010s, even though the period saw a downturn in commodity prices.

Yield, by contrast, has grown more modestly and far more erratically. Soybean yields are up about a third since 2011 and corn yields about half, but both swing sharply from year to year. These swings, not changes in planted area, account for most of the deviation of final production from trend. Because yield is largely weather-determined, the short-run risks facing the 2027 crop are likely to operate mainly through yield, while the underlying area trend that anchors production growth remains intact.

Challenges to 2027 Production Growth

The long-run production trends suggest that Brazil’s production growth has been persistent and largely supported by continued area expansion. However, the question is whether the combination of short-run shocks facing the 2026/27 crop season is strong enough to interrupt that trajectory. Elevated fertilizer costs, Brazil’s heavy dependence on imported inputs, tighter credit conditions, high interest rates, and rising farm debt are increasing financial pressure at a time when margins are already near breakeven (see farmdoc daily, March 16, 2026). At the same time, a potentially very strong El Niño during the 2026/27 crop season adds weather uncertainty, with potential effects on soybean planting and second-crop corn performance.

Fertilizer costs are one of the reasons to question whether USDA’s soybean and corn production outlook for Brazil will be realized. Prices have been decreasing from recent peaks, but they remain high enough to affect planting and input-use decisions. The surge in fertilizer prices, particularly for urea, associated with the conflict in the Middle East, coincided with the period when Brazilian farmers typically begin purchasing inputs for the 2026-27 crop season. When the conflict began in late February, less than 30% of fertilizer purchases for the next crop season had been completed by Brazilian farmers (see farmdoc daily, April 10, 2026).

Unlike the United States, Brazil does not have a strong domestic fertilizer industry, and in 2025, fertilizer imports accounted for 88% of total consumption (see farmdoc daily, April 20, 2026). In this context, high fertilizer costs may not prevent planting altogether, but they could limit input application, reduce margins, and make USDA’s early production estimates harder to achieve, especially for soybean production, which begins to be planted in the middle of September. For second-crop corn (known as safrinha), planted after the soybean harvest in early 2027, the impact could be smaller if urea prices continue to decline.

The combination of lower soybean prices, high production costs, and weak port premiums compressed profitability for Brazilian farmers. In 2025, trade tensions between the United States and China boosted soybean export premiums at Brazilian ports, even during a period that typically sees lower premiums due to record production. Without a similar premium this year, farm margins would likely have been even tighter, potentially turning negative – reducing the incentive for aggressive acreage expansion.

Financial stress among Brazilian farmers has also intensified in recent years as interest rates have remained elevated, with the benchmark rate reaching nearly 15% per year. As borrowing costs have risen and lenders have grown more selective, access to credit has become another source of pressure for producers already dealing with tighter margins. With less room to rely on their own capital, farms are turning more often to banks, trading companies, and multinational input suppliers to fund each crop season (see farmdoc daily, October 11, 2024).

A potentially strong El Niño adds weather uncertainty to the next Brazilian crop season. El Niño conditions are already present and are expected to strengthen into the Northern Hemisphere winter of 2026/27, according to the Climate Prediction Center’s Official Probabilistic El Niño-Southern Oscillation Outlook released on June 15, 2026. Equatorial sea surface temperatures are above average across the central and eastern Pacific Ocean, and atmospheric circulation anomalies over the equatorial Pacific are consistent with El Niño. The last El Niño event of comparable intensity occurred in 2015/16, when Brazil faced significant crop losses.

During El Niño events, conditions across South America often favor reduced precipitation in parts of Center-West and northern Brazil, where soybean and corn production are concentrated, and increased rainfall in southern Brazil. Because Brazil has continental dimensions and agricultural production is spread across several regions, some areas may face intense drought while others may experience excessive rainfall. In this case, both soybean and corn production could be affected, since any delay in soybean planting would directly affect the performance of the second-crop corn planted afterward.

Discussion

What, then, to make of the initial USDA 2027 production forecasts for Brazil? The economic headwinds facing Brazilian producers are real, and tighter margins, costlier credit, and high input costs may well slow the pace of expansion on some margin. But the historical record offers little support for a widespread, farmer-driven retreat in production. Brazilian output set records straight through the 2014-16 commodity price collapse, and the pattern appears to be repeating now: USDA estimates a record 2026 soybean crop of 180 MMT following a previous record 2025 crop of 172.5 MMT, even as margins sit close to breakeven and near their lowest level in nearly two decades (see farmdoc daily, March 16, 2026).

Yield has been the larger source of year-to-year deviation from long-run production trends; weather is bigger driver than the economics that dictate acreage and input decisions. For those anticipating that a Brazilian shortfall will firm commodity prices and lift U.S. farm incomes, the more dependable bet is on an adverse weather event than on a deliberate pullback in planting and input use. However, the broad geographic scope of Brazilian production makes it less likely that adverse weather shocks occur across the entire corn and soybean growing area. Absent such a shock, initial 2027 USDA production forecasts for Brazil look like a reasonable extension of a durable trend, even as current economic and weather risks warrant close monitoring.

References

Climate Prediction Center/NCEP. ENSO: Recent evolution, current status and predictions. National Oceanic and Atmospheric Administration, U.S. Department of Commerce. June 15, 2026. https://www.cpc.ncep.noaa.gov/products/analysis_monitoring/lanina/enso_evolution-status-fcsts-web.pdf

Colussi, J. and M. Langemeier. "Brazil Heads for a Record Soybean Harvest as Farm Margins Approach Breakeven." farmdoc daily (16):44, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 16, 2026.

Colussi, J. and M. Langemeier. "Middle East Conflict Revives Concerns Over Fertilizer Dependence in the U.S. and Brazil." farmdoc daily (16):68, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 20, 2026.

Monaco, H., J. Colussi, G. N. Schnitkey, N. Paulson, A. V. Lobo and J. A. Caregnato. "The Iran Conflict and Fertilizer Markets: Why Brazil Faces Greater Near-Term Risk than the U.S." farmdoc daily (16):62, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 10, 2026.

Monaco, H., J. Colussi, G. Schnitkey and N. Paulson. "Shifting Dynamics in Soybean Farm Funding in Brazil." farmdoc daily (14):186, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 11, 2024.

Sousa, Dayanne. “Fertilizer Crunch in Brazil Raises Risks for the Farm Economy” Bloomberg. May 21, 2026. https://www.bloomberg.com/news/articles/2026-05-21/iran-war-driven-fertilizer-crisis-threatens-brazil-farming

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.