Incidence of Financial Stress on Illinois Grain Farms

Over time working capital has deteriorated and debt-to-asset ratios have increased on grain farms across the Midwest. Average levels of working capital and debt-to-asset ratios still suggest an overall strong financial position for grain-based agriculture. However, averages mask diversity in financial positions across farms. Ranges in debt-to-asset and working capital positions are presented in this article using data on grain farms enrolled in Illinois Farm Business Farm Management (FBFM). At the end of 2017, 12% of grain farms had debt-to-asset ratios exceeding 0.50, up from 7% at the end of 2013.

Trends in Financial Measures

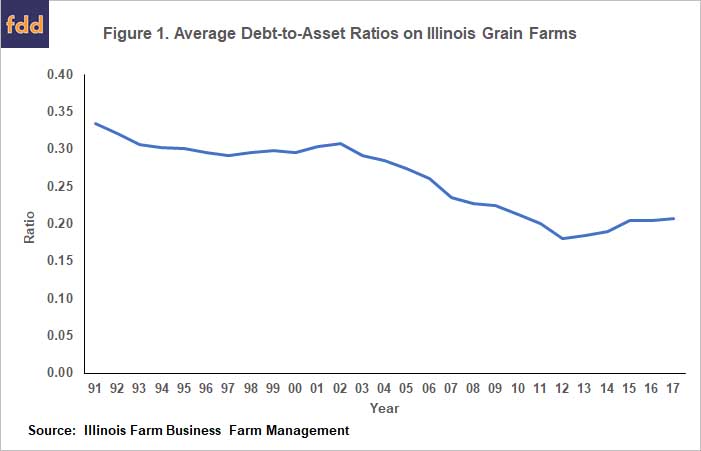

The debt-to-asset ratio is a measure of solvency, equaling debt divided by total assets. Generally, debt-to-asset ratios below 0.30 indicate a strong financial position. Debt-to-asset ratios above 0.50 mean the farm’s assets are funded by more debt than equity. Farmers with debt-to-asset ratios above 0.50 face more risk than those with less than a 0.50 debt-to-asset ratio. Debt-to-asset ratios above .75 would indicate that an adverse event could cause debt to exceed assets, and the farm is in a weak and risky position.

Debt-to-asset ratios on Illinois grain farms had an overall downward trend from 1991 to 2012, decreasing from .34 in 1991 to a low of .18 in 2012 (see Figure 1). Since 2012, debt-to-asset ratios have increased to .21 at the end of 2017 (for more information, see farmdoc daily, August 17, 2018). While a general upward trend is not desired, the average debt-to-asset level at the end of 2017 is not particularly troublesome either.

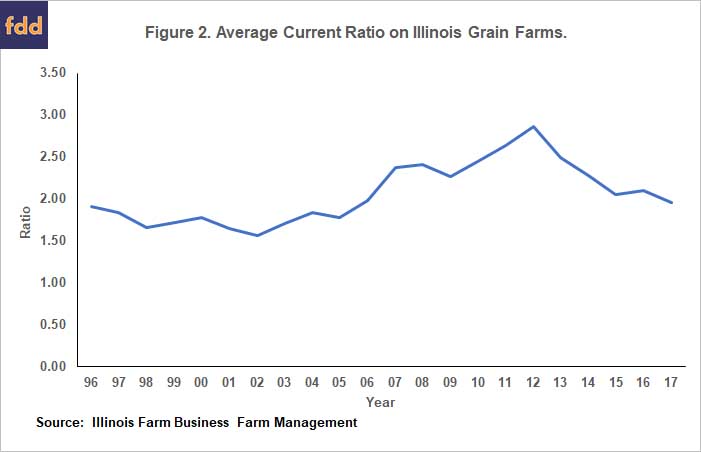

Current ratio is the measure of the working capital position of the farm. The current ratio equals current assets divided by current debt. Higher current ratios indicate that a buffer exists for meeting current obligations. This buffer is useful in countering any adverse events that may befall the farm. Current ratios above 2.00 are generally viewed as being very strong. A ratio below 1.00 indicates a problematic current position, as not enough current assets exist to meet current obligations. Farms often have a current ratio between 1.00 and 2.00.

The average current ratio on Illinois grain farms increased from 1.97 in 2006 up to 2.86 in 2012 (see Figure 2). The 2006-2012 period had high commodity prices and costs had not increased enough to offset higher prices, resulting in a period of above-average incomes. This above-average income period allowed farmers to improve their financial positions and strengthen current ratios. Since 2012, commodity prices have been lower, and incomes have decreased, resulting in the current ratio decreasing from 2.86 in 2012 to 1.96 in 2017. The average 1.96 ratio in 2017 is not particularly worrisome, however, the 2017 level is the same level as in 2006, indicating improvement in the current position during the high-income years has been erased.

Range in Financial Positions at the End of 2017

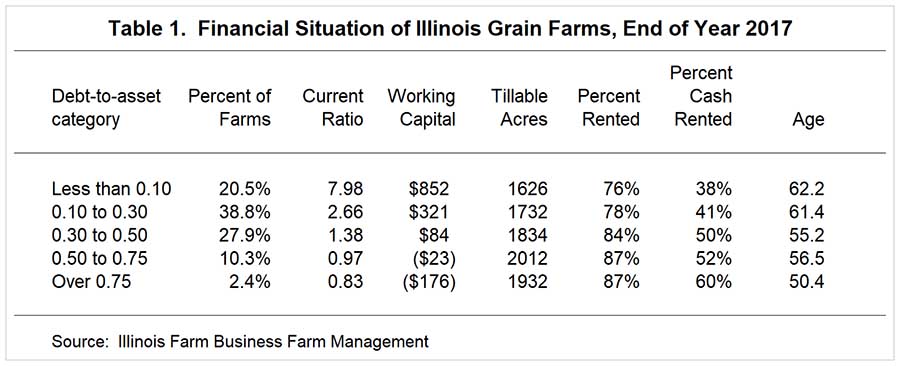

While averages serve as good indicators for general trend, they do not depict the range of financial positions on grain farms. Table 1 gives statistics for farms falling in different debt-to-asset ratio ranges at the end of 2017. This table summarizes data from grain farms in Illinois FBFM who meet the following conditions:

- Are categorized as grain farms, meaning that they receive most of their income from grain operations.

- Are certified usable by FBFM field staff.

- Are sole proprietors. Many farms have more than one person or entity involved, and those entities can have different financial positions. The focus on sole proprietors assures that financial statements are for complete operations.

- Had at least 1,000 tillable acres. This criterion assures that a significant grain enterprise exists on the farm.

Of the farms categorized in Table 1, 20.5% had less than a 0.10 debt-to-asset ratio, meaning that these farms had minimal debt with no more than 10% of their total assets financed. The 0.10 to 0.30 debt-to-asset category had 38.8% of farms and the 0.30 to 0.50 category had 27.9% of farms. In total, 87.3% of farms had debt-to-asset ratios less than 0.50, meaning a large majority of farms carry a level of debt that is less than half the asset level.

There are 10.3% of farms with debt-to-asset ratios between 0.50 and 0.75. These farms may require financial adjustments to reduce risks and to increases chances of viability in the future. There are 2.4% of farms with a debt-to-asset ratio above .75. These farms face significant risks and may require restructuring.

At the end of 2018, there are 12.7% of these farms with debt-to-asset ratios exceeding 0.50, meaning debt levels are more than half the level of assets. The percent of farms with above 0.50 debt-to-asset ratios has increased over time. At the end of 2013, only 6.6% of farms had a debt-to-asset ratio above 0.50. The percent of farms with above 0.50 debt-to-asset ratio has almost doubled from 2013 to 2017.

Working capital position is highly correlated with debt-to-asset ratio. The current ratio is 7.98 for the strongest debt-to-asset category, those with a less than 0.10 debt-to-asset ratio. Alternatively, the current ratio of .83 is in the problematic zone below 1.0 for the weakest debt-to-asset category, those with a 0.75 or higher debt-to-asset ratio (see Table 1). On average, the current ratio is below 1.0 for farms with debt-to-asset ratios above 0.50. These farms likely need to restructure assets or debt to improve the working capital position.

With each rising debt-to-asset category, the percent of the farm rented increases. Farms in the 0.10 debt-to-asset ratio category rent 76% of farmed acres, while farms with a debt-to-asset ratio above 0.5 rent 87% of farmed acres.

The portion of acres cash rented also increases as debt-to-asset ratio increases. Among farms in the 0.10 debt-to-asset category, only 38% of farmland is cash rented, compared to 60% for the over 0.75 debt-to-asset category.

Age is inversely correlated with debt-to-asset ratio. Average age is 62.2 years for the less than 0.10 debt-to-asset ratio category down to 50.4 years for the over .75 debt-to-asset ratio category.

Trends in tenure, cash rent percent, and age likely relate to the length of time the operation has been in farming. Younger operators likely have accumulated less wealth, thereby resulting in less owned land and more rented farmland. In recent years, these younger operators may have had to rely more on cash rented farmland to increase their farming base.

Summary

Statistics presented in this paper suggest a spectrum of financial positions on grain farms in Illinois. At one end are farms that are financially strong. These farms have the wherewithal to withstand a great deal of adversity, and also seek opportunities to invest funds in the farming operation. In the middle are farms whose solvency position is sound but may have very tight working capital positions. Some sort of restructuring may be needed to address working capital on these farms. Overall, the majority of farms are in strong, solvency positions.

There are some farms that have much weaker financial positions. These farms may face financial difficulties moving forward, particularly if grain prices remain at their current levels. These farms may need to restructure assets and debts.

None of this suggests the existence of a current financial crisis. In fact, many farms may improve financial position in 2018 as a result of high yields, some pre-harvest hedging, and Market Facilitation Program (MFP) payments (see farmdoc dailly, October 11, 2018). However, the situation will bear close scrutiny however moving into 2019, as projections currently indicate the expectation for grain farm income to be negative (see farmdoc dailly, September 18, 2018). A year of losses would weaken the financial position of grain farms in the Midwest.

References

Krapf, B., D. Raab and B. Zwilling. "Agricultural Debt Continues to Increase." farmdoc daily (8):154, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, August 17, 2018.

Swanson, K., G. Schnitkey and J. Coppess. "Reviewing Prices and Market Facilitation Payments." farmdoc daily (8):188, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 11, 2018.

Schnitkey, G. and K. Swanson. "2019 Crop Budgets Suggest Dismal Corn and Soybean Returns." farmdoc daily (8):173, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, September 18, 2018.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.