Rewriting the RFS Playbook: The Challenge of Meeting D4 Biomass-Based Diesel RIN Generation for 2026-2027

On March 27, 2026, the U.S. Environmental Protection Agency (EPA) released the final “Set 2” rule establishing Renewable Volume Obligations (RVOs) under the Renewable Fuel Standard (RFS) for 2026 and 2027. The 2026 and 2027 increases in the biomass-based diesel RVOs are unprecedented in the history of the RFS and will set the trajectory of the U.S. biomass-based diesel industry for years to come (farmdoc daily, April 16, 2026). In our most recent article in this series (farmdoc daily, April 27, 2026), we used a detailed balance sheet approach to project the level of D4 RIN generation required to meet the final RVOs in 2026 and 2027. The headline finding was that required D4 net RIN generation must increase from 7.10 billion RIN gallons in 2025 to 11–12 billion RIN gallons in 2026 and 2027—levels that have no precedent in the history of the U.S. biomass-based diesel industry. The purpose of this article is to put that requirement into a more tangible context by examining the recent monthly pace of D4 RIN generation alongside the pace that will be needed to meet the final RVOs.

Analysis

We begin with a brief recap of the D4/D5 RIN balance sheet analysis presented in our April 27th article. The framework is the standard balance sheet identity that governs RIN markets:

Beginning RIN Bank + RIN Generation + Current Year Deficit − RVOs − Exports − Previous Year Deficit − Ending RIN Bank = 0

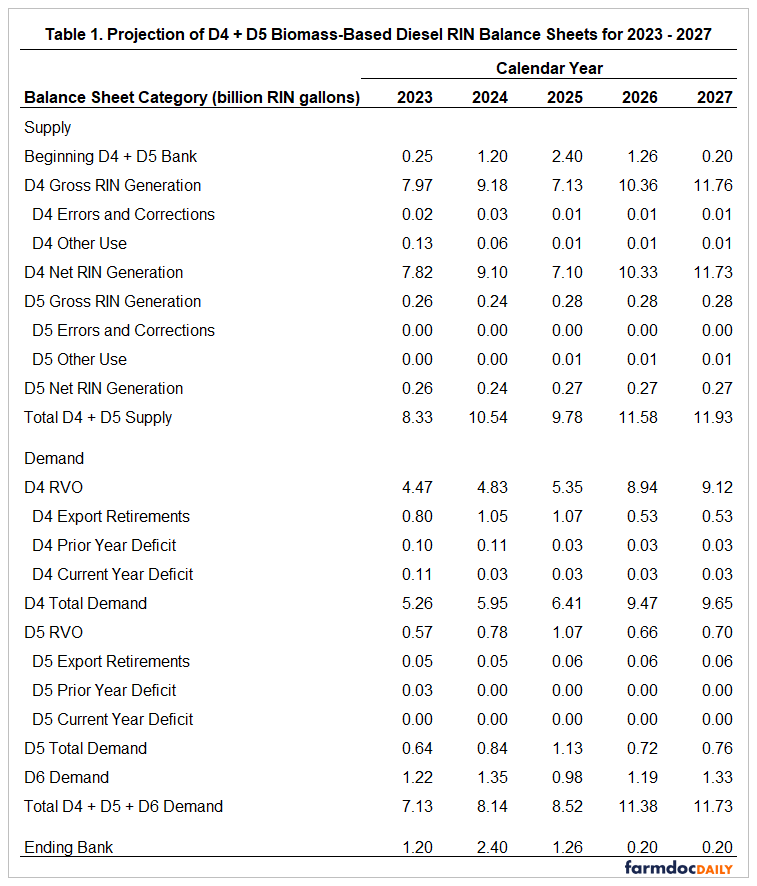

We construct the D4/D5 balance sheet using actual EPA data for 2023–2025 and projections for 2026–2027 based on the final Set 2 RVOs, an assumed minimum operating bank of 200 million gallons in both 2026 and 2027, and crucial cross-market linkages with the D6 conventional balance sheet. The balance sheet from our April 27th article is shown in Table 1. Required D4 net RIN generation must rise from 7.10 billion RIN gallons in 2025 to 10.99 billion RIN gallons in 2026 and 11.89 billion RIN gallons in 2027.

These represent increases of 55 and 67 percent, respectively, relative to the actual level of 2025. In absolute terms, the 3.89-billion-RIN-gallon increase in required D4 net generation between 2025 and 2026 alone is nearly four times the size of the 2025 D4/D5 ending bank of 0.96 billion gallons. The demand structure underlying these required generation levels comprises three components: the biomass-based diesel applicable RVO of 9.07 billion gallons in 2026 and 9.20 billion in 2027; D4 export retirements of 0.534 billion gallons in each year; and the D6 “pull”—the volume of biomass-based diesel RINs needed to satisfy the conventional fuel obligation when D6 ethanol RIN supply is insufficient—of 1.42 billion gallons in 2026 and 1.41 billion in 2027. The ending D4/D5 bank is projected to fall from 0.96 billion gallons at the close of 2025 to the assumed minimum operating level of 0.20 billion gallons by year-end 2026 and to remain at that level through 2027. In short, required D4 net RIN generation is the crucial number that the biomass-based diesel sector must hit in each of the next two compliance years, and the cushion provided by the RIN bank is essentially exhausted after 2026.

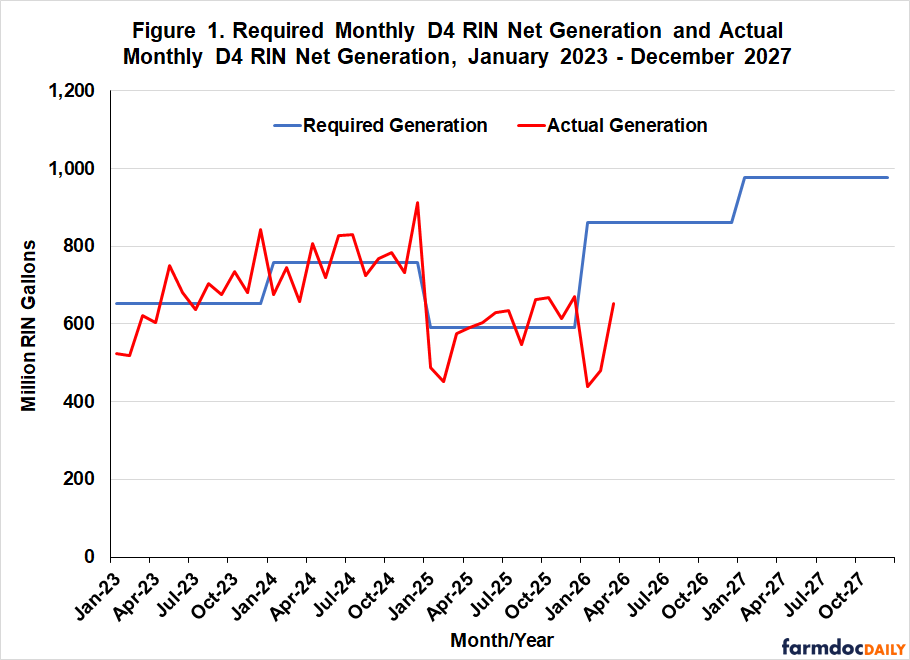

The challenge of meeting these required generation levels comes into sharp relief when set against the recent history of monthly D4 RIN net generation. Figure 1 shows actual monthly D4 RIN net generation from January 2023 through the latest data point in 2026, alongside the average monthly pace of D4 RIN net generation required to satisfy total D4 demand in each calendar year. The required monthly pace was 652 million RIN gallons in 2023, rose to 758 million RIN gallons in 2024, and fell to 592 million RIN gallons in 2025. Under the final Set 2 rule, the required monthly pace jumps to 916 million RIN gallons in 2026 and 991 million RIN gallons in 2027. RIN generation incorporates both imports and domestically produced biomass-based diesel.

Two features of Figure 1 stand out. The first is the simple fact that the required monthly pace of D4 RIN net generation for 2026 and 2027 is well beyond any sustained level observed in the historical record. Monthly generation averaged 652 million RIN gallons in 2023, 758 million in 2024, and 592 million in 2025. Only one month over the three-year period of 2023–2025—December 2024 at 906 million gallons—came anywhere close to the monthly pace required for 2026 and 2027, and this single observation is widely understood to reflect a pull-forward of imports motivated by the expiration of the $1 per gallon blenders tax credit rather than sustained underlying supply. In other words, the biomass-based diesel sector must shift to a level of monthly D4 RIN generation that has, with one transitory exception, never been achieved in any single month over the last three years and must sustain that level for 24 consecutive months.

The second notable feature of Figure 1 is that monthly D4 RIN net generation in early 2026 has started off well below the pace needed to meet the 2026 RVO. The latest available data show monthly D4 RIN net generation of 436 million gallons in January, 478 million in February, and 649 million in March 2026. Each of these monthly values is below not only the pace required to meet the 2026 RVO but also the average monthly pace observed in 2025. Import levels, in particular, remain very low in comparison with 2024 due to the switch from the blenders tax credit to the 45Z clean fuel production credit. Imported biofuels are not eligible for the new 45Z credit. The cumulative shortfall through the first three months of 2026 is on the order of 1,184 million RIN gallons relative to the pro-rata required pace; or, about 11 percent of the entire annual requirement. Closing this early-year gap will require monthly D4 RIN generation in the remaining nine months of 2026 to average roughly 1,090 million RIN gallons—a pace that is over 20 percent higher than the highest single month ever recorded. Even if the December 2024 pull-forward is treated as the upper bound of what is physically possible, the required pace for the balance of 2026 exceeds it by a wide margin.

It is important to recognize that our projection of the required monthly pace of D4 RIN generation for 2026 and 2027 could prove to be too high. Three factors could push the required pace below the required levels shown in Figure 1. First, the volume of small refinery exemptions (SREs) awarded by the EPA for 2026 and 2027 may turn out to be larger than the 7.55 billion gallons projected in the final Set 2 rulemaking. Because the percentage standards in the final rule are fixed from this point forward, a larger SRE volume would translate into a smaller applicable RVO in volume terms across each fuel category, including biomass-based diesel. Second, actual obligated petroleum gasoline and diesel volumes for 2026 may fall short of the EPA’s projection. This is particularly relevant given the run-up in crude oil prices associated with the Iran war, which would be expected to reduce gasoline and diesel consumption relative to the EPA’s baseline projection. Lower obligated volumes would, again through fixed percentage standards, reduce the applicable RVOs in volume terms. Third, D4 export retirements in 2026 and 2027 may turn out to be even lower than the 534 million gallons assumed in our balance sheet projection.

Even taken together, however, the cumulative effect of these three factors would only moderately reduce the required monthly pace of D4 RIN generation for 2026 and 2027. Our best assessment is that, under reasonable downside scenarios for SREs, obligated volumes, and exports, the required monthly pace would fall to no lower than roughly 850 million RIN gallons per month, compared with the average 950 million RIN gallon pace for 2026-2027 under our baseline assumptions. A monthly pace of 850 million RIN gallons would still exceed the average pace observed in any year over 2023–2025 and would require sustained generation well above the 592 million gallon average observed in 2025. In other words, even under a relatively generous combination of downside assumptions, the challenge facing obligated parties and biomass-based diesel producers in 2026 is only marginally diminished. The bottom-line is that the biomass-based diesel sector will have to sustain monthly D4 RIN generation at a level reached only a few times in the historical record under the most conservative assumptions.

Implications

The analysis presented in this article frames the central question facing the biomass-based diesel sector and obligated parties under the EPA’s final Set 2 rule: How will the market deliver an unprecedented increase in D4 RIN generation in 2026 and 2027? The required monthly pace of D4 RIN net generation must rise from 592 million gallons in 2025 to 916 million gallons in 2026 and 991 million gallons in 2027—levels that exceed any sustained monthly pace in the historical record. Compounding the challenge, monthly D4 RIN generation in the first three months of 2026 has averaged only 521 million gallons, leaving a cumulative shortfall of approximately 1,184 million gallons that will have to be made up over the remaining nine months of the year. Mechanically, this means that monthly generation must average nearly 1,100 million gallons for the rest of 2026 if the 2026 RVO is to be met without drawing the D4/D5 ending bank below the assumed minimum operating level or accumulating large deficits.

How will obligated parties and biomass-based diesel producers respond to this challenge? At a high level, there are three margins of adjustment. First, biomass-based diesel producers can ramp up capacity utilization, both for FAME biodiesel and for renewable diesel, well above the 60 percent average utilization rates observed in 2023–2025. Second, imports of biomass-based diesel and feedstocks can play a larger role than they did during the slowdown of 2025. Third, in the event that physical production and imports fall short, obligated parties can draw down the existing D4/D5 RIN bank and incur compliance deficits that must be made up in the following year. The relative contributions of these three margins of adjustment will shape outcomes in the D4 RIN market, in the soybean oil and other feedstock markets, and ultimately in the diesel fuel market itself. These dynamics will be the focus of the next articles in this series, beginning with a detailed look at the implications for biomass-based diesel production and capacity utilization.

References

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: The Impact of Final RVOs on Projected D4 Biomass-Based Diesel RIN Generation for 2026-2027.” farmdoc daily (16):73, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 27, 2026.

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: Final 2026–2027 RVOs for Biomass-based Diesel.” farmdoc daily (16):66, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 16, 2026.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.