Rewriting the RFS Playbook: The Impact of Final RVOs on Projected D4 Biomass-Based Diesel RIN Generation for 2026-2027

On March 27, 2026, the U.S. Environmental Protection Agency (EPA) released the final “Set 2” rule establishing Renewable Volume Obligations (RVOs) under the Renewable Fuel Standard (RFS) for 2026 and 2027. The final rule confirms 70 percent reallocation of 2023–2025 small refinery exemptions (SREs) and delays rather than eliminates the so-called half-RIN penalty for imported biofuel and feedstock until 2028 or later. The 2026 and 2027 increases in the biomass-based diesel RVOs are unprecedented in the history of the RFS and will set the trajectory of the U.S. biomass-based diesel industry for years to come (farmdoc daily, April 16, 2026). The sheer magnitude of the RVO increases naturally raises fundamental questions about how the higher obligations will play out in the D4 RIN market, in physical biomass-based diesel production, and in underlying feedstock markets. The purpose of this article is to project D4 RIN generation requirements for 2026–2027 using a detailed balance sheet approach applied to both the D4/D5 balance sheet and the D6 balance sheet. The D4/D5 balance sheet extends the RIN balance sheet framework introduced in our earlier farmdoc daily articles (November 5, 2025; November 12, 2025; November 24, 2025; February 25, 2026) but is updated with actual 2025 data and the final RVOs. The D6 balance sheet is new to this series and is motivated by the crucial role that the D6 supply/demand balance plays in determining how much of the D4 market’s compliance burden is driven by the conventional fuel obligation rather than the biomass-based diesel mandate.

Analysis

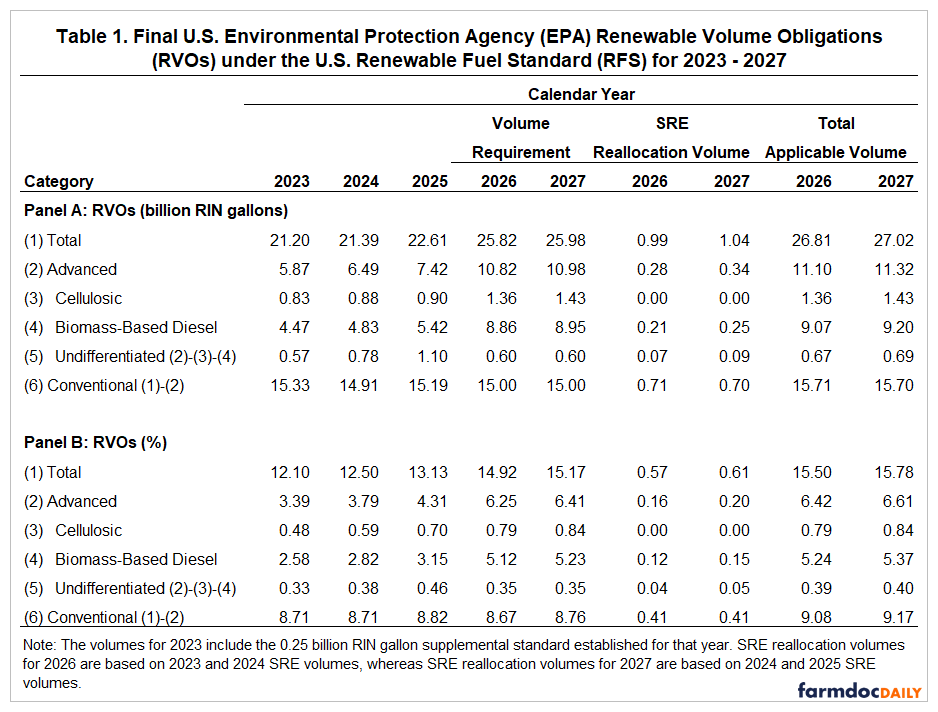

We begin with a brief review of the final RVOs for 2025 and 2026 presented in our April 16th article, reproduced here as Table 1. Panel A shows the final applicable volumes in billions of RIN gallons and Panel B presents the corresponding percentage standards. The total applicable biomass-based diesel volumes—combining the volume requirement with 70 percent SRE reallocation—are 9.07 billion RIN gallons in 2026 and 9.20 billion in 2027. The increases in biomass-based diesel RVOs for 2026 and 2027 are unprecedented in the history of the RFS, jumping by 67 and 70 percent, respectively, compared to the 2025 total of 5.42 billion gallons. Previously, the largest year-over-year increase in the biomass-based diesel RVO was in 2013, when the RVO increased by 28 percent. The conventional fuel applicable volumes are 15.71 and 15.70 billion RIN gallons, up from 15.19 billion in 2025. The increase in the applicable conventional RVO of approximately 0.52 billion RIN gallons, driven almost entirely by SRE reallocation, is modest in absolute terms but has important consequences for the D6 balance sheet.

The first step in understanding how the higher biomass-based diesel RVOs for 2026 and 2027 will play out regarding physical biomass-based diesel production and underlying feedstock markets is to estimate the required D4 RIN generation in each year. Analysis of this issue is complicated by two features of the RFS compliance system that create important linkages across fuel and RIN categories. First, RINs can be banked from year-to-year, meaning that the stock of RINs carried forward from a prior compliance year can buffer—at least temporarily—the need for new production. The buffering is only temporary because RINs have a limited life: a RIN generated in a given year can be used for compliance in that year or the following year only. Second, D4 RINs function historically as the “marginal” gallon for filling not only the biomass-based diesel RVO but also the undifferentiated advanced and conventional fuel RVOs (farmdoc daily, July 19, 2017). Because RINs are nested based on greenhouse gas reduction scoring (farmdoc daily, May 17, 2023), D4 RINs can substitute upward in the RIN hierarchy, filling deficits in the advanced and conventional categories when lower-category RIN supply is insufficient.

The framework used to project D4 RIN generation is the balance sheet identity that governs RIN markets. Each year’s balance sheet can be written as:

Beginning RIN Bank + RIN Generation + Current Year Deficit − RVOs − Exports − Previous Year Deficit − Ending RIN Bank = 0

Each component of this identity provides critical insights into market dynamics:

- Beginning RIN Bank: The stock of RINs carried forward from previous years.

- RIN Generation: New RINs created through biofuel production and imports.

- Current Year Deficit: Up to 20 percent of obligations may be waived.

- RVOs: The regulatory demand for RINs based on renewable volume obligations.

- Exports: RINs associated with exported biofuels that cannot be used for RFS compliance.

- Previous Year Deficit: Deficits from previous year must be made up in the following year.

- Ending RIN Bank: The stock of RINs carried forward to the following year.

The logic of the RIN balance sheet for a given year can be further demonstrated as follows:

Total Supply = Beginning RIN Bank + RIN Generation + Current Year Deficit

Total Demand = RVOs + Exports + Ending RIN Bank + Previous Year Deficit

Total Supply – Total Demand = 0

At first glance, it may seem inconsistent to have a deficit and a positive ending RIN bank for the same compliance year. This can, and does occur, for a given compliance year because some obligated parties run a deficit while others finish the year with a positive inventory of RINs.

We construct separate D4/D5 and D6 balance sheets for the analysis in this article. The D4/D5 balance sheet incorporates both biomass-based diesel (D4) and non-ester renewable diesel and other qualifying advanced biofuels (D5) RINs because this is the way that historical RIN bank data is reported by the EPA. D5 RINs play a small but measurable role in satisfying the undifferentiated advanced mandate and export retirements. The D6 balance sheet models the ethanol conventional fuel market, and the implied D4 use line in that sheet feeds directly into the D6 demand line of the D4/D5 balance sheet, the critical cross-market linkage.

Because compliance has not yet closed for 2025, the balance sheets for 2023–2025 incorporate a mix of actual EPA data and projections based on partial-year information. The starting point is the beginning D4/D5 bank for 2023, which the latest published data on historical RIN bank levels by the EPA indicates is 247 million gallons (see Table 1.8.3-1 on p.37 of the document at the following link: https://www.epa.gov/system/files/documents/2026-03/420r26011.pdf).

Key assumptions for 2023–2027 include the following:

- D4, D5, and D6 gross RIN generation for 2023-2025 are drawn directly from EPA’s public RIN data reports. For 2026 and 2027, D6 net RIN generation is held constant at the 2025 actual level of 14.647 billion gallons, reflecting an expectation of stable operating conditions for U.S. ethanol production.

- Errors and corrections and other use (RINs retired for non-compliance reasons such as invalid RINs, enforcement obligations, ocean-going vessel use, and non-transportation applications) are taken from EPA’s public RIN data for 2023–2025. For 2026-2027, errors and corrections and other use are held at their 2025 levels.

- RVOs are drawn directly from Table 1 each year.

- D4, D5, and D6 export retirements for 2023–2025 are based on EPA compliance data. For 2026 and 2027, D4 exports are projected at 534 million gallons, 50 percent of the 2025 level of 1.067 billion gallons, consistent with the decline in early 2026 export RIN data. D5 export retirements for 2026-2027 are kept constant at the 2025 level of 57 million gallons. In a similar manner, D6 export retirements for 2026-2027 are fixed at the projected 2025 level of 657 million gallons.

- For 2023 and 2024, previous year deficits are drawn from EPA’s reported compliance data. For 2025, only the current year deficit has been reported by EPA (the 2024 deficit carried forward). For simplicity, we assume that 2025-2027 current year deficits for D4, D5, and D6 equal the last known data point, which is the prior year deficit for 2025.

- The ending D6 bank is computed in the conventional manner as: Ending RIN Bank = Beginning RIN Bank + RIN Generation + Current Year Deficit − RVOs − Exports − Previous Year Deficit. This can be a negative number because the computation at this point is based solely on D6 RIN data and does not account for the use of D4 RINs to “top off” the conventional RVO. Implied D4 use is the reported D6 ending bank (which must be non-negative by definition) minus the computed ending bank. We assume that the reported EPA ending D6 RIN bank in 2026 and 2027 will be 1 billion gallons, reflecting the tight overall market conditions for RINs. The ending D6 RIN bank has been lower in only one year, 2022, when the bank dipped to 568 million gallons.

- The ending D4/D5 bank for 2026 and 2027 is fixed at 200 million gallons. This minimal bank reflects the expectation that the market will be operating in a “tight” regime during these high-RVO years, analogous to conditions during the first renewable diesel boom of 2021–2023 when ending bank levels were similarly constrained. Starting with this assumption for the value of the ending RIN bank in 2026 and 2027, net D4 RIN generation is imputed using the balance sheet identity as follows: Net RIN Generation = RVO + Exports + Current Year Deficit – Previous Year Deficit + Ending RIN Bank – Beginning RIN Bank.

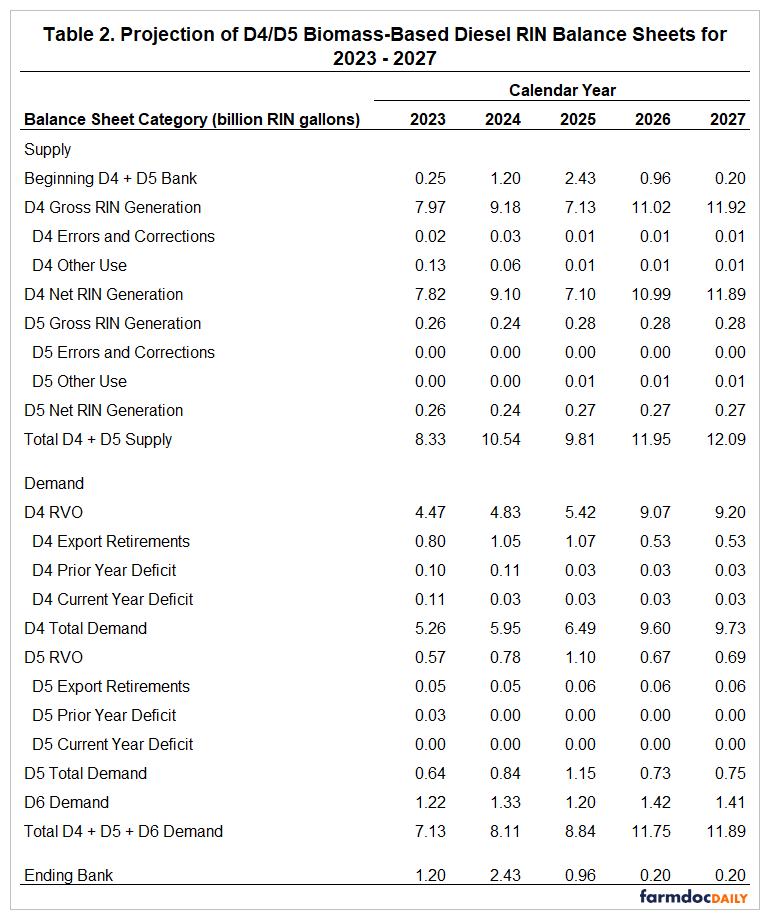

The resulting D4/D5 RIN balance sheets for 2023–2027 are presented in Table 2. The results reveal a dramatic and historically unprecedented shift in D4 market fundamentals between the 2023–2025 and the 2026–2027 period.

The supply side of the D4/D5 balance sheet tells the story of a market that experienced a massive surplus accumulation followed by a sharp reversal. In 2023, D4 net RIN generation of 7.82 billion gallons far exceeded total D4+D5+D6 demand of 7.13 billion gallons, enabling the ending bank to build from 247 million gallons at the start of the year to 1.20 billion by year-end. The surplus expanded further in 2024 as D4 net generation reached 9.10 billion gallons against demand of only 8.11 billion, pushing the ending bank to a historically unprecedented 2.43 billion gallons—nearly three times the previous peak in 2016. The massive bank reflected a combination of robust renewable diesel capacity expansion and RVOs set under the Biden administration’s Set 1 rule that were lower than expected. In 2025, however, the picture reversed sharply. D4 net generation fell to 7.10 billion gallons as biomass-based diesel production dropped precipitously in response to policy uncertainty surrounding the transition from the blenders tax credit to the 45Z Clean Fuel Production Credit and the absence of a finalized Set 2 rule. Despite this production decline, total demand of 8.84 billion gallons exceeded generation, drawing down the bank from 2.43 billion to 0.96 billion gallons by year-end 2025.

The 2026 and 2027 projections reveal the scale of the challenge ahead. Required D4 net RIN generation must jump from 7.10 billion gallons in 2025 to 10.99 billion in 2026 and 11.89 billion in 2027. These translate to increases of 55 percent and 67 percent, respectively, relative to the 2025 actual level. In absolute terms, the 3.89-billion-gallon increase in required D4 net generation between 2025 and 2026 alone is larger than the entire 2025 D4/D5 ending bank.

The demand structure underlying these required generation levels is instructive. D4 total demand in 2026 reaches 9.60 billion gallons, driven primarily by the D4 biomass-based diesel applicable RVO of 9.07 billion plus 530 million gallons of export retirements. D5 total demand in 2026 is 730 million gallons. Most importantly, D6 demand on the D4/D5 pool—the volume of biomass-based diesel RINs that must be used to satisfy the conventional fuel obligation when D6 ethanol RIN supply is insufficient—stands at 1.42 billion gallons in 2026. This D6 pull is larger than in any prior year, including 2023 and 2024, and reflects the increase in the D6 RIN supply deficit created by the SRE reallocation volumes in the final rule. The mechanics of this deficit are analyzed in detail in the D6 balance sheet discussion below. In 2027, the D6 pull remains nearly unchanged at 1.41 billion gallons, as the assumed EPA D6 ending bank holds at 1.00 billion gallons, leaving the gap between D6 supply and demand that D4 must bridge essentially the same as in 2026.

The ending D4/D5 bank trajectory reveals the full severity of the compliance squeeze. The bank falls from 0.96 billion at the close of 2025 to just 0.20 billion by year-end 2026—a decline of 760 million gallons in a single compliance year. In 2027, the bank holds at 0.20 billion, reflecting the assumption that the minimum viable operating bank has been reached. For practical purposes, the entire surplus accumulated during 2023–2024 will have been consumed within two compliance years of the final rule taking effect. After 2026, the market will have no meaningful RIN cushion to absorb production shortfalls or demand surprises.

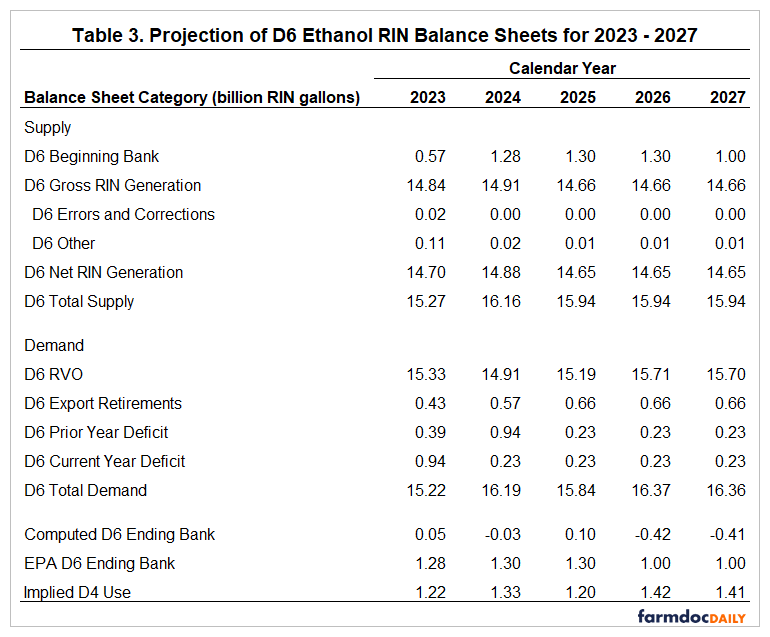

The D6 balance sheet presented in Table 3 analyzes the conventional ethanol fuel market and provides the foundation for the D6 demand line in Table 2. Understanding the D6 balance sheet is essential to a complete picture of D4 RIN market dynamics under the final Set 2 rule because it explains why a significant share of D4 RIN demand in 2026 and 2027 is driven by the need to backfill the conventional RVO with D4 RINs.

The supply side of the D6 balance sheet is governed by domestic ethanol production capacity. D6 gross RIN generation was 14.84 billion gallons in 2023 and 14.91 billion in 2024 before slipping to 14.66 billion in 2025, reflecting modestly lower domestic fuel ethanol consumption. For 2026 and 2027, D6 net RIN generation is projected at 14.65 billion gallons, equal to the 2025 level. After accounting for a beginning bank of 1.30 billion gallons in 2026, total D6 supply is 15.94 billion gallons in both 2026 and 2027.

The demand side of the D6 balance sheet is revealing. The D6 applicable RVO rises from 15.19 billion gallons in 2025 to 15.71 billion in 2026 and 15.70 billion in 2027. This increase of approximately 520 million gallons reflects the addition of SRE reallocation volumes to the conventional category under the final Set 2 rule. Export retirements—D6 RINs retired by ethanol exporters—add another 657 million gallons of demand in each year. Prior year deficit carryover adds 229 million gallons, and current year deficits are assumed to remain at 229 million gallons, equal to recent historical levels. Total D6 demand therefore reaches 16.37 billion gallons in 2026 and 16.36 billion in 2027.

The arithmetic of D6 supply and demand produces a computed D6 ending bank of −0.424 billion gallons in 2026 and −0.414 billion in 2027. A negative ending bank is physically impossible—it would require D6 RINs that do not exist. In practice, this deficit is resolved by obligated parties substituting higher-value D4 biomass-based diesel RINs for D6 RINs in their compliance submissions. Under the RFS nested compliance structure, D4 RINs are fully fungible for D6 purposes: a D4 RIN can satisfy a D6 conventional fuel obligation on a one-for-one basis. The volume of D4 substitution required is determined by comparing the computed D6 ending bank to the EPA’s reported D6 ending bank.

In 2023 and 2024, the implied D4 use averaged 1.28 billion gallons per year, driven by a similar but smaller structural D6 deficit. The conventional fuel RVO in those years was lower, but export retirements and deficit carryovers were large enough to create a gap that D4 RINs had to fill. What changes under the final Set 2 rule is the size of the applicable D6 obligation. The 520-million-gallon increase in the D6 applicable RVO from 2025 to 2026—driven almost entirely by SRE reallocation—pushes the D6 deficit, and therefore the implied D4 use, above 2023–2024 levels.

The D6 balance sheet also illustrates a subtlety about how the SRE reallocation policy transmits through the compliance system. When the EPA reallocates SRE volumes back into the applicable RVOs, the increment is spread across all four fuel categories in proportion to the SRE percentage standards. For the conventional category, this means that the reallocation adds roughly 0.52 billion gallons to the D6 applicable obligation in both 2026 and 2027 (0.71 billion gallons of SRE reallocation multiplied by the approximately 73 percent conventional share). Every gallon of this reallocation increment that falls on the conventional category translates directly into an additional D4 RIN demand because the D6 supply base is not expected to grow. This is the mechanism by which SRE reallocation policy generates additional D4 demand pressure through the conventional fuel compliance channel.

Finally, it is important to recognize the key uncertainties regarding our projection of D4 RIN generation requirements for 2026 and 2027. First, the actual compliance volumes of obligated parties may vary from the volumes in Table 1 because the volume of SREs awarded by the EPA may differ from those projected in the final rulemaking for 2026 and 2027 (and 2024 and 2025 as well). If the volume of SREs turns out to be higher than the EPA projection of 7.55 billion gallons this will reduce the RVOs in volume terms because the percentage standards shown in Table 1 are fixed from this point forward. In a similar fashion, the actual volume of obligated petroleum and diesel for 2026 and 2027 may differ from that projected by the EPA. Second, actual RIN deficits may differ substantially from what we assumed. This is particularly important for the D6 RIN balance sheet because the magnitude of the deficits can be much larger simply because the conventional mandate is so much bigger than any of the other mandates.

Implications

The balance sheet analysis presented in this article quantifies the full scope of the D4 RIN generation challenge created by the EPA’s final Set 2 rule for 2026 and 2027. Required D4 net RIN generation must increase from 7.10 billion gallons in 2025 to 10.99 billion in 2026 and 11.89 billion in 2027—increases of 55 and 67 percent, respectively, over a two-year period. These are demands on the physical biomass-based diesel production system that have no precedent in the history of the RFS. The analysis identifies two distinct sources of D4 RIN demand growth. The first and largest source is the biomass-based diesel RVO, which increases from 5.42 billion gallons in 2025 to 9.07 billion in 2026 and 9.20 billion in 2027, directly requiring more physical production of FAME biodiesel and renewable diesel. The second source, the D6 “pull,” is more subtle and often absent from market discussions of the final rule’s implications. In both 2026 and 2027, the deficit in D6 ethanol RIN supply requires approximately 1.42 and 1.41 billion gallons, respectively, of D4 RINs to satisfy conventional fuel compliance obligations. When the D6 pull is combined with the biomass-based diesel applicable RVO and other D4 demand components, total D4+D5+D6 demand reaches 11.75 billion gallons in 2026 and 11.89 billion in 2027—well above what the biomass-based diesel RVO alone would imply.

The trajectory of the D4/D5 RIN bank is an equally critical finding. The 2.43-billion-gallon bank at year-end 2024 provided a historically large buffer, but the market will effectively be operating with no cushion as of the start of the 2027 compliance year. Any material shortfall in domestic biomass-based diesel production in either 2026 or 2027—from feedstock supply disruptions, capacity underperformance, or unexpected demand-side developments—will have no banked RIN supply to absorb it. This transforms each compliance year under the final Set 2 rule into a high-wire act in which physical production must closely track the required generation levels shown in Table 2. These findings set the stage for the following articles in this series, which will analyze the implications for physical biomass-based diesel production, capacity utilization rates, and feedstock market demand. Understanding those production dynamics is essential for interpreting what the final Set 2 rule will mean for soybean oil, animal fat, used cooking oil, and other feedstock markets over the next two years.

References

Gerveni, M., T. Hubbs and S. Irwin. “Biodiesel and Renewable Diesel: What’s the Difference?” farmdoc daily (13):22, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, February 8, 2023.

Gerveni, M., T. Hubbs and S. Irwin. “Overview of the U.S. Renewable Fuel Standard.” farmdoc daily (13):90, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, May 17, 2023.

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: Final 2026–2027 RVOs for Biomass-based Diesel.“ farmdoc daily (16):66, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 16, 2026.

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: Final RVOs for 2026–2027.“ farmdoc daily (16):30, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, February 25, 2026.

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: Revised RVOs Backload Projected Biomass-Based Diesel Production and Feedstock Use into 2027.“ farmdoc daily (15):217, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 24, 2025.

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: The Impact of Revised RVOs on Projected Biomass-Based Diesel Production and Feedstock Use for 2026–2027.“ farmdoc daily (15):209, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 12, 2025.

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: The Impact of Revised RVOs on Projected D4 Biomass-Based Diesel RIN Generation for 2026–2027.“ farmdoc daily (15):204, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 5, 2025.

Hubbs, T. and S. Irwin. “Rewriting the RFS Playbook: The Impact of Recent EPA Decisions on 2023–2027 RVOs for Biomass-Based Diesel.“ farmdoc daily (15):199, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 29, 2025.

Irwin, S. and D. Good. “Filling the Gaps in the Renewable Fuels Standard with Biodiesel.” farmdoc daily (7):130, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, July 19, 2017.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.