The Clean Fuel Production Tax Credit (45Z); Introductory Discussion

The Clean Fuel Production Credit, enacted in the Inflation Reduction Act and often referred to simply as “45Z” for its placement in the tax code, remains the subject of much attention (Brooks, February 11, 2026; Bausch and Squire, February 5, 2026; Warnes, November 1, 2025; McNaughton-Peterson, October 14, 2025; Ayoub and Parum, July 24, 2025). For farmers, interest has centered on the possibility that “low carbon” grain could receive price premiums if biofuel producers begin to place greater value on feedstocks with lower carbon intensity scores. Most existing 45Z information remains highly technical, filled with tax, legal, and policy language, as well as life-cycle analysis terms such as “CO2e” “mmBTU,” and “ILUC.” At the same time, some private-sector messages may overpromise by suggesting guaranteed premiums or simple “carbon money” without clearly explaining market mechanisms, data collection needs, or supporting record requirements. This article begins a discussion of the 45Z tax credit with particular attention to the potential impacts for Midwest corn and soybean farmers.

Background

Congress created the Clean Fuel Production Credit in the Tax Code with Section 13704 of the Inflation Reduction Act of 2022 (P.L. 117-169; 26 U.S.C. §45Z) and subsequently amended it to restrict its applicability to foreign feedstocks, adding that such fuel must be “exclusively derived from a feedstock which was produced or grown in the United States, Mexico, or Canada” (P.L. 119-21, at Sec. 70521). Historically, 45Z joins a line of tax credits for ethanol and biofuels; before there was 45Z, there was the Volumetric Ethanol Excise Tax Credit (VEETC). It provided a $0.45 per gallon tax credit to gasoline suppliers who blended ethanol into the gasoline they sold. Congress enacted VEETC in the “American Jobs Creation Act of 2004” and allowed it to expire on December 31, 2011 (P.L. 108-357; Rept. 108-755; 26 U.S.C. §6426; Sautter, Furrey and Gresham, 2006; Diggs, 2012; Cunningham et al, February 26, 2019). Before there was VEETC there was the ethanol blending tax credit created in the Energy Tax Act of 1978, coinciding with the second oil crisis and the Iranian revolution (P.L. 95-618; Duffield, Xiarchos and Halbrock, 2008; farmdoc daily, March 12, 2026).

While they are both tax credits for biofuels production, 45Z differs significantly from VEETC. One key similarity, however, is that neither tax credit goes directly to the farmer. VEETC was a fixed tax credit for the entity blending ethanol with gasoline, while 45Z goes to the entity producing the biofuels. Importantly, the 45Z credit is flexible and adjusts based on the emissions factor for the fuel produced (IRS, updated March 16, 2026; 91 FR 5160 (February 3, 2026), proposed rule).

Despite its differences, research on VEETC provides useful perspectives for 45Z, including for setting expectations on the benefits to farmers. Researchers have concluded that about 5% of VEETC made its way to corn farmers (Gerveni et al., 2026). In general, the benefits from VEETC worked their way through the supply chain to the farmer via prices paid for ethanol and from ethanol production for the corn purchased. Researchers have estimated that VEETC’s tax credit may have been worth about $0.135 per bushel of corn (Bielen, Newell and Pizer, 2018). Notably, VEETC also overlapped with the Renewable Fuels Standard enacted in 2005 and expanded in 2007; combined, the two different policies (tax credit to blenders vs. mandate on them) raised the cost of the tax credit to about $5 billion per year. If 5% of that expenditure made its way to farmers, it was worth about $250 million per year.

Discussion

In the statute, Congress defined a qualified facility as “a facility used for the production of transportation fuels,” but not for clean hydrogen production. Congress defined transportation fuel as “suitable for use as a fuel in a highway vehicle or aircraft,” and “has an emissions rate which is not greater than 50 kilograms of CO2e per mmBTU,” or carbon dioxide equivalent for greenhouse gases per 1 million British thermal units. Congress also limited the definition for fuels, restricting those “[d]erived from coprocessing an applicable material . . . with a feedstock that is not biomass” (P.L. 117-169, at Sec. 13704; 26 U.S.C. §45Z(d)). Simply, 45Z is a tax credit for qualified biofuel producers, such as ethanol, biodiesel, and sustainable aviation fuel (SAF).

In 45Z, the tax credit is the amount that is equal to multiplying the emissions factor by the applicable amount per gallon (or gallon equivalent), that the taxpayer produces at a qualified facility and sells during the taxable year. Congress established a floor for the tax credit of $0.20 per gallon and a ceiling of $1.00 per gallon (26 U.S.C. §45Z(a) and (f)). The emissions factor is calculated as 50 kilograms of CO2e per mmBTU minus the emission rate for the fuel, divided by 50 kilograms of CO2e per mmBTU. Congress required the Secretary of the Treasury to annually publish a table of emissions rates “based on the amount of lifecycle greenhouse gas emissions” for the fuels. For non-aviation transportation fuels, the rate is based on what is known as the GREET model which stands for “Greenhouse gases, Regulated Emissions, and Energy use in Transportation” and was developed by the Argonne National Laboratory (26 U.S.C. §45Z(b)). Aviation fuel emission rates are to be calculated based on the “most recent Carbon Offsetting and Reduction Scheme for International Aviation which has been adopted by the International Civil Aviation Organization with the agreement of the United States,” known as CORSIA, or a similar methodology that satisfies the Clean Air Act. Treasury is also to provide a “distinct emissions rate” for fuels derived from animal manure. Emissions rates “shall be adjusted as necessary to exclude any emissions attributed to indirect land use change,” (ILUC) and to be adjusted for inflation after 2024 (26 U.S.C. §45Z(b)).

Based on the statute, the maximum 45Z tax credit can be as high as $1 per gallon for ethanol and $1.75 for SAF, but the actual amount depends on how low the carbon intensity score of the fuel is relative to the policy benchmark (50 kilograms of CO2e per mmBTU). This is the central feature of 45Z that the size of the tax credit is tied to the carbon intensity score of the biofuel produced and sold. The basic idea is that a biofuel producer can claim a tax credit for each gallon of fuel produced if that fuel meets the policy’s carbon intensity standard. As a result, the policy creates a direct financial incentive for biofuel producers to lower the carbon intensity of the fuel they sell.

How would any benefits make their way to the farmers growing and selling the corn or soybean feedstock? The short answer is indirectly. Benefits would reach the farmer through the potential that biofuel producers will seek lower-carbon feedstocks to reduce the total carbon intensity score for the fuels they produce; lower-carbon corn or soybeans, in turn, would increase the amount of tax credit per gallon the biofuel producer can claim. Because the value of the tax credit rises as carbon intensity falls, biofuel producers have incentives to look for ways to reduce the total carbon intensity of their fuels. Although farmers do not receive the tax credit themselves, 45Z could still matter to them by impacting the incentives for biofuel producers.

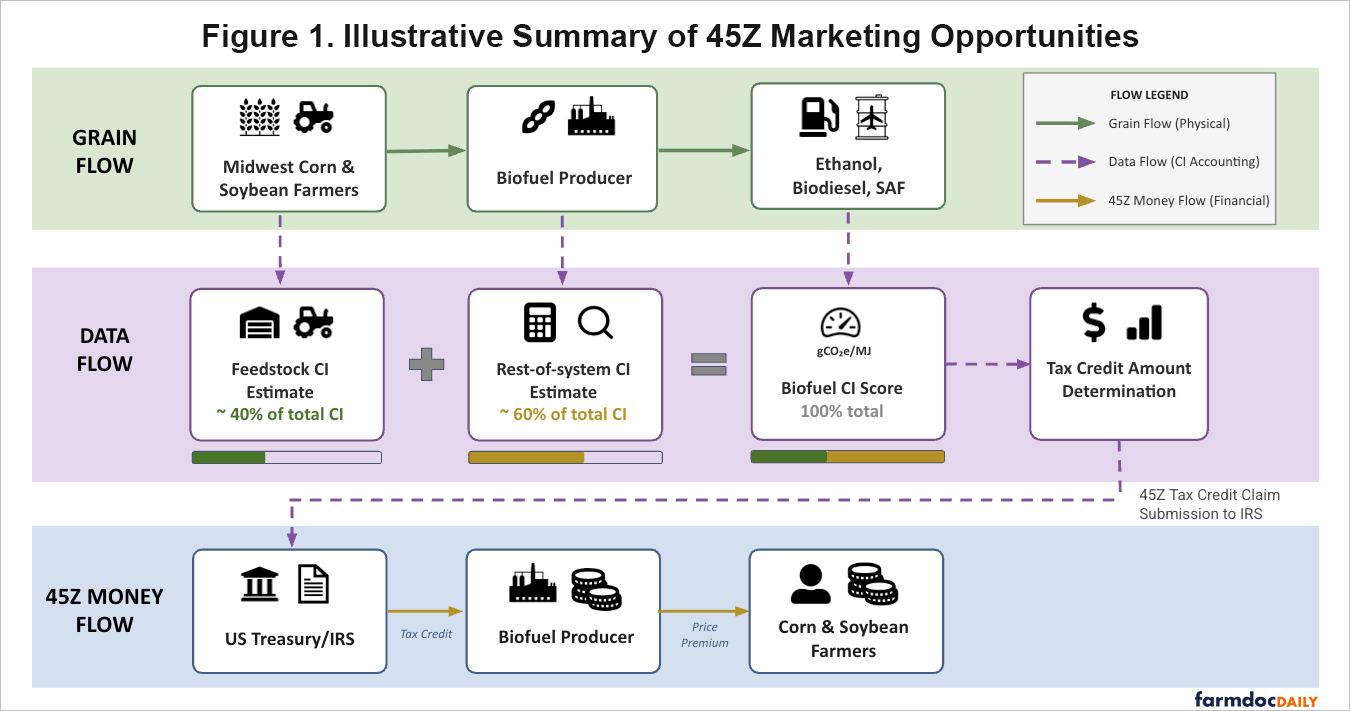

Scientific research suggests that feedstock production contributes at least 40% and up to 60% of total biofuel lifecycle carbon intensity (Rosenfeld et al., 2018, Scully et al., 2021 ; Lee et al., 2021; Xu et al., 2022). A biofuel producer seeking to lower its total fuel carbon intensity could source grains with lower carbon intensity scores. This could result in product differentiation in grain markets, where some bushels are viewed as more attractive than others because of their low carbon scores. In turn, producers with lower-carbon grain may find themselves better positioned under this new market demand. Figure 1 illustrates this concept and the potential opportunities for corn and soybeans. Green, purple dashed, and gold arrows represent grain flow, CI data flow, and financial value flow, respectively.

Figure 1 summarizes the relationship between physical grain movement, carbon-intensity accounting, and potential financial value under 45Z. Farmers supply feedstocks to biofuel producers, who convert them into eligible biofuels. Farm-level feedstock carbon intensity (CI) estimates are combined with rest-of-system CI estimates to calculate the final biofuel CI score, which determines the tax credit amount available to the biofuel producer. Figure 1 uses an illustrative split in which feedstock CI contributes about 40% of total biofuel CI and the rest-of-system CI contributes about 60%. This split is broadly consistent with ballpark estimates for corn ethanol reported in the scientific literature, although actual shares will vary by feedstock sourcing, biofuel production pathway and technology, and accounting assumptions (Rosenfeld et al., 2018, Scully et al., 2021 ; Lee et al., 2021; Xu et al., 2022).

Concluding Thoughts

Congress created the Clean Fuel Production Credit to incentivize the production and sale of biofuels with lower carbon intensity, or greenhouse gas emissions. Importantly, the direct recipient of the 45Z tax credit is the biofuel producers not farmers. The policy will affect farmers indirectly, mostly through the potential that biofuel producers will seek lower-carbon feedstocks to reduce the total carbon intensity score for the fuels they produce. The policy may increase the value of lower-carbon grain, but only indirectly and under specific market conditions. Producers with lower-carbon grain may find themselves better positioned under this new market condition.

As they consider this policy further, producers should not assume that having a lower carbon intensity score will automatically guarantee a higher grain price or any further capturing of a share of the 45Z tax credit. Lower-carbon grain may create a marketing opportunity, but that opportunity only has value if a biofuel producer is willing to recognize that difference and offer a premium in the market or through a contract. 45Z may make low-carbon grain look like a “higher quality” feedstock from the perspective of a biofuel producer, but the existence of this quality difference does not automatically create a quality premium for the sellers. Whether value actually reaches the farmer will depend on the willingness of biofuel producers to pass through tax credit benefits, which in turn depends on local grain market conditions; competition among biofuel producers for low-carbon feedstock; and the cost of verification for fulfilling IRS requirements, which also plays a role. The practical takeaway is that 45Z creates a potential market opportunity for some Midwest grain producers, but not a guaranteed increase in farm income. The policy could make farm-level carbon intensity more economically relevant than it has been in the past, especially if ethanol plants begin to compete for lower-carbon feedstocks. If so, this also will put a premium on the practices farmers implement to produce the crops, with value attached to those practices that reduce carbon intensity or greenhouse gas emissions.

Future articles will review these matters further, as well as take a deeper look at carbon intensity. This will include reviewing what a feedstock carbon intensity score means, how it may be calculated for an individual farm, and what management choices can affect it. Other articles will also review farm-level economics with simple scenario analysis to show how much per-bushel or per-acre value a grower might plausibly receive under different carbon intensity and market pass-through assumptions.

References

Ayoub, Samantha and Faith Parum. “Ag-Powered Fuels: 45Z Clean Fuel Production Credit.” American Farm Bureau Federation, Market Intel. July 24, 2025. https://www.fb.org/market-intel/45z-clean-fuel-production-credit.

Bausch, Natalina Sents and Mariah Squire. “45Z Clean Fuel Credit Updates Draw Praise From Farm and Biofuel Groups.” Successful Farming, agriculture.com. February 5, 2026. https://www.agriculture.com/45z-clean-fuel-credit-updates-draw-praise-from-farm-and-biofuel-groups-11898411.

Bielen, David A., Richard G. Newell, and William A. Pizer. "Who did the ethanol tax credit benefit? An event analysis of subsidy incidence." Journal of Public Economics 161 (2018): 1-14. https://doi.org/10.1016/j.jpubeco.2018.03.005.

Brooks, Rhonda. “Tow Ways 45Z Will Help Farmers Capture Dollars.” Farm Journal/AgWeb. February 11, 2026. https://www.agweb.com/news/business/two-ways-45z-will-help-farmers-capture-dollars.

Coppess, J. "Flashback, 1979: What the Previous Cliff Might Tell Us About the Potential One Ahead." farmdoc daily (16):42, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 12, 2026.

Cunningham, L.J., B. Canis, D.A. Arostegui, and B.D. Yacobucci. “Alternative Fuel and Advanced Vehicle Technology Incentives: A Summary of Federal Programs.” Congressional Research Service, R42566. February 26, 2019. https://www.congress.gov/crs_external_products/R/PDF/R42566/R42566.18.pdf.

Diggs, Amy. "The Expiration of the Ethanol Tax Credit: An Analysis of Costs and Benefits." Pol'y Persp. 19 (2012): 47. https://journal.policy-perspectives.org/articles/volume_19/10_4079_pp_v19i0_10425.pdf.

Duffield, James A., Irene M. Xiarchos, and Steve A. Halbrock. "Ethanol policy: past, present, and future." SDL Rev. 53 (2008): 425. https://red.library.usd.edu/cgi/viewcontent.cgi?article=1633&context=sdlrev.

Gerveni, Maria, Todd Hubbs, Scott H. Irwin, and James H. Stock. "The Biofuels Blueprint: Understanding the US Renewable Fuel Standard." Applied Economic Perspectives and Policy (2026). https://doi.org/10.1002/aepp.70083.

Lee, U., H. Kwon, M. Wu, and M. Wang. “Retrospective analysis of the U.S. corn ethanol industry for 2005-2019: implications for greenhouse gas emission reductions.” Biofuels, Bioproducts and Biorefining 15(5): 1318-1331, 2021. https://scijournals.onlinelibrary.wiley.com/doi/10.1002/bbb.2225.

McNaughton-Peterson, Sarah. “What is 45z, and how can your farm benefit?” FarmProgress.com. October 14, 2025. https://www.farmprogress.com/farm-policy/what-is-45z-and-how-can-your-farm-benefit-.

Rosenfeld, J., J. Lewandrowski, T. Hendrickson, K. Jaglo, K. Moffroid, and D. Pape. “A Life-Cycle Analysis of the Greenhouse Gas Emissions from Corn-Based Ethanol.” U.S. Department of Agriculture, September 5, 2018. https://www.usda.gov/sites/default/files/documents/LCA_of_Corn_Ethanol_2018_Report.pdf.

Sautter, John A., Laura Furrey, and R. Lee Gresham. "Construction of a Fool's Paradise: Ethanol Subsidies in America." Sustainable Dev. L. & Pol'y 7 (2006): 26. https://digitalcommons.wcl.american.edu/cgi/viewcontent.cgi?article=1300&context=sdlp.

Scully, M.J., G.A. Norris, T.M.A. Falconi, and D.L. MacIntosh. “Carbon intensity of corn ethanol in the United States: state of the science.” Environmental Research Letters 16(4): 043001, 2021. https://iopscience.iop.org/article/10.1088/1748-9326/abde08.

Warnes, Bryce. “How Can Ag Producers Prepare for the 45z Tax Credit?” Ambrook.com. November 1, 2025. https://ambrook.com/education/taxes/45z-tax-credit-guide.

Xu, H., U. Lee, and M. Wang. “Life-cycle greenhouse gas emissions reduction potential for corn ethanol refining in the USA.” Biofuels, Bioproducts and Biorefining 16: 671-681, 2022. https://scijournals.onlinelibrary.wiley.com/doi/10.1002/bbb.2348.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.