Concentration and Monopoly Pricing: What Economics Tells Us

The US has entered one of its reoccurring eras of concern over concentrated markets and what economists call monopoly pricing, a firm’s ability to sustain its price above its cost of production, as illustrated by these recent farmdoc posts: “Consolidation Trends in the U.S. Nitrogen Fertilizer Industry” (farmdoc daily, May 26, 2026), “Lawmakers Target Meatpacker Consolidation Amid High Prices” (Farm Policy News Update, May 27, 2026), and “FTC Confirms Probe of Rising Fertilizer Prices” (Farm Policy News Update, May 29, 2026). Three intertwined lessons from the long history of market concentration and monopoly pricing in public policy and economic thought are discussed: (1) monopoly pricing depends on barriers to market entry not number and size of firms, (2) entry barriers come in many forms, often willingly enacted by government to address other concerns, and (3) reducing monopoly pricing can lead to higher prices and less production.

Monopoly Pricing

Sustained ability to set price above the cost of production depends on a barrier that prevents entry of new firms into a market. Because entry is difficult, existing firms in the market can raise their price to capture sustained returns above their cost of production, which economists call abnormal profits.

A single firm with 100% market share will not price above the cost of production if other firms can easily enter. To do so is to invite other firms to enter. Similarly, a market with many firms can capture abnormal profits if an entry barrier prevents new firms from entering the market.

Entry barriers, not market share concentration, prevent competition, thus allowing pricing to earn sustained abnormal profits. Size and market concentration can interact with entry barriers to facilitate abnormal profits, but the barrier to entry must exist for them to have an impact. Stated alternatively, addressing size and market concentration without addressing the barrier to entry will have little to no impact on the existence of sustained abnormal profits.

Many Forms of Entry Barriers

Production entry barriers arise out of a firm’s technology or marketing channel. Startup costs to begin production, including acquisition of specialized knowledge, may be so high to restrict entry. A key input may have no close substitute. Often the only policy responses to production barriers are subsidized loans and funding research to develop competing technology or marketing channels.

Public policy can willingly create entry barriers to encourage actions viewed as enhancing societal well-being. Patents encourage creative work by insuring income can be earned from them. Qualifying standards set minimum competencies for some professions such as doctors, financial advisors, teachers, beauticians, etc., meant to increase the likelihood of competent service. International trade restrictions, including tariffs, are imposed to mitigate unfair international competition but reduce domestic supply, thus raising prices for domestic users. Environmental regulations to mitigate real and perceived pollutants can raise the costs of building and maintaining a plant, and thus entry into the market.

But the entry barrier most think of is firm behavioral barriers. They are intentional manipulations of the market to limit entry or raise prices. Often behavioral entry barriers are actions that build upon a production or public policy entry barrier.

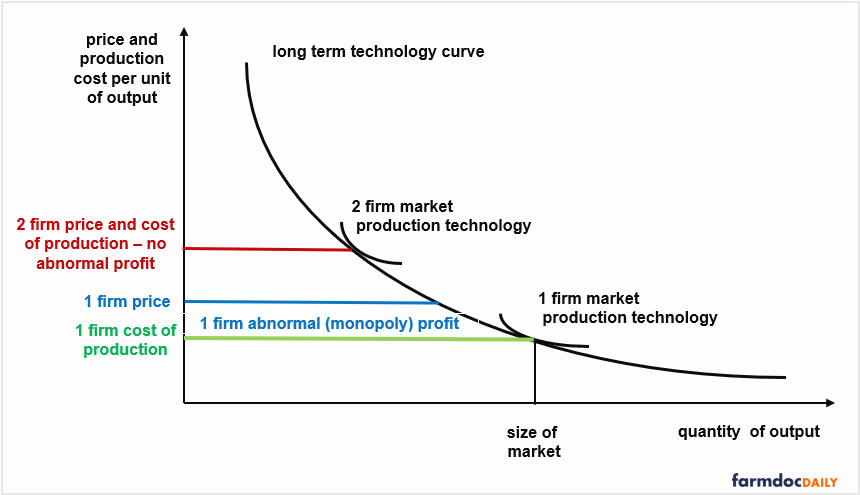

Economies of Production

Even if monopoly pricing exists, inducing more competition to eliminate abnormal profits may make users worse off. The reason is economies of production, i.e. steep declines in cost of production as a firm increases output. To illustrate, the steeply declining long run technology curve in the figure below results in users paying a lower price with 1 instead of 2 firms (i.e. more competition). The single firm earns an abnormal profit. Price exceeds its cost of production (area bounded by blue and green horizontal lines). But users pay a lower price than if the market has 2 firms earning no abnormal profit (red line where price equals cost). While the figure is drawn so that market output is the same with 1 and 2 firms, output can be less with 1 than 2 firms, resulting in users paying more for less. Economies of production also are often necessary for US production to be economically competitive.

Summary

Public policy must and should monitor firm behavior and pursue appropriate action when monopoly pricing is abused, but it is also far easier to raise charges of monopoly pricing than to document its existence let alone address it in ways that improve user well-being. Specifically,

- Neither few firms nor high market concentration are sufficient to conclude monopoly pricing exists.

- Monopoly pricing exists when barriers prevent firms from entering a market.

- Entry barriers are often willingly created by public policy to address other concerns.

- Economies of production can be so large that users are better off with monopoly pricing.

- Imports or lower tariffs are often the only viable short-term policy to reduce monopoly pricing.

- Often, the only viable long-term policy is to fund research on alternative production technologies, substitute products, or higher production efficiency.

- Charges of monopoly pricing often divert attention from the underlying cause of higher price.

Taking a broader view, while monopoly pricing is receiving lots of attention, it is only one of several issues potentially associated with market consolidation and power. They include the impact on rate and type of technological change, disproportionate impact on the poor, and access to production inputs. These other potential issues should be assessed and discussed.

These economic ideas and concepts are discussed in the context of the US fertilizer market in

Zulauf, C., G. Schnitkey, K. Swanson and N. Paulson. “Monopoly Pricing Power and Fertilizer Prices.” farmdoc daily (12):50, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 13, 2022.

References

Monaco, H., N. Paulson, G. Schnitkey and C. Zulauf. "Consolidation Trends in the U.S. Nitrogen Fertilizer Industry." farmdoc daily (16):91, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, May 26, 2026.

Hanrahan, R. “FTC Confirms Probe of Rising Fertilizer Prices.” Farm Policy News Summary, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, May 29, 2026.

Hanrahan, R. “Lawmakers Target Meatpacker Consolidation Amid High Prices.” Farm Policy News Summary, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, May 27, 2026.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.