Revisiting Ukraine, Russia, and Agricultural Commodity Markets

Ukraine and Russia have become an important source for global supplies of major agricultural commodities in the past 25 years (farmdoc daily, October 11, 2012). These countries, often collectively referred to along with various other Eastern European and Central Asian nations as the Black Sea region, play an important role in the production and export of major grains (corn, wheat, and barley) and oilseeds (especially sunflower and sunflower oil) (Glauber and Laborde, 2022). In addition to the direct toll it will take on the people of the region, the Russian invasion of Ukraine last week introduces many economic concerns including the impact of the conflict on global agricultural markets.

This article summarizes the role of Ukraine and Russia in production and exports of corn, wheat, barley, soybeans, and sunflower oil. The production and export share data provided in all figures is calculated from the USDA Foreign Agricultural Service’s Production, Supply and Distribution database (USDA-FAS PSD). Note that we’ve chosen to consider the members of the European Union (EU) as a single unit in considering production and export shares and comparing them with other countries.

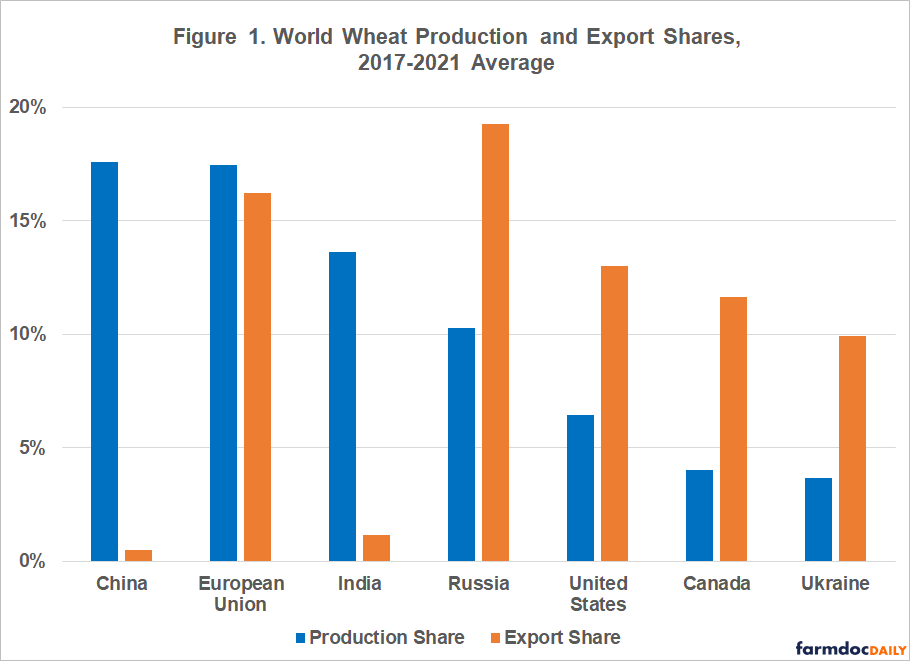

Wheat

Global production and export shares for wheat, averaged from 2017 to 2021, are reported for the top 7 wheat producing countries in Figure 1. Russia and Ukraine account for 14% of global wheat production and rank 1st and 5th, respectively. Both countries are prominent exporters, providing nearly 30% of global wheat exports. The EU, U.S., and Canada are also major producers and exporters of wheat. China and India are major wheat producers, but are net importers and provide relatively small shares of global wheat exports. Other countries with fairly large wheat export shares include Australia (8.4%), Argentina (6.6%), Kazakhstan (4.1%), and Turkey (3.4%).

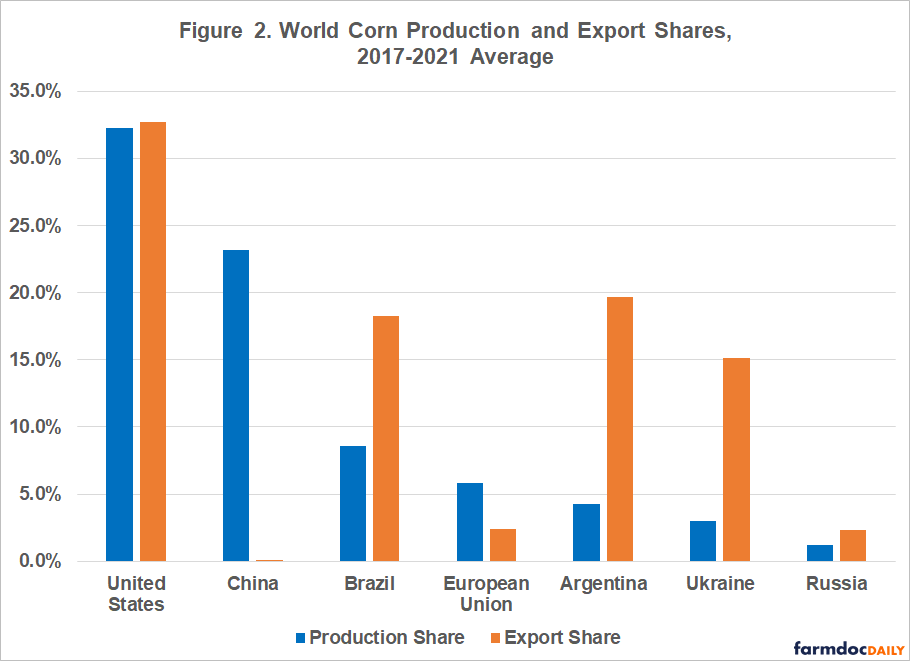

Corn

Production and export shares for corn across selected countries are reported in Figure 2. The U.S. remains the dominant global producer (32%) and exporter (33%) for corn. Brazil (18.3%) and Argentina (20%) rank 2nd and 3rd in corn exports. Ukraine now ranks 4th, contributing over 15% of world corn exports. Russia ranks 6th with a 2.3% share of corn exports. Notably, Ukraine has been the dominant supplier of corn to China. A shift towards import of more U.S. corn to China began in 2020 following a poor Ukrainian crop (He, Hayes, and Zhang 2021).

Growth in the share of world corn production and exports from the Black Sea region (Russia, Ukraine, and Kazakhstan) has been substantial, rivaling that of the increase in production in China and both production in and exports from South America over the past twenty years (farmdoc daily, June 2, 2017 and November 18, 2020). Corn production in India, Mexico, and South Africa exceeds that in Russia, but account for smaller world export shares.

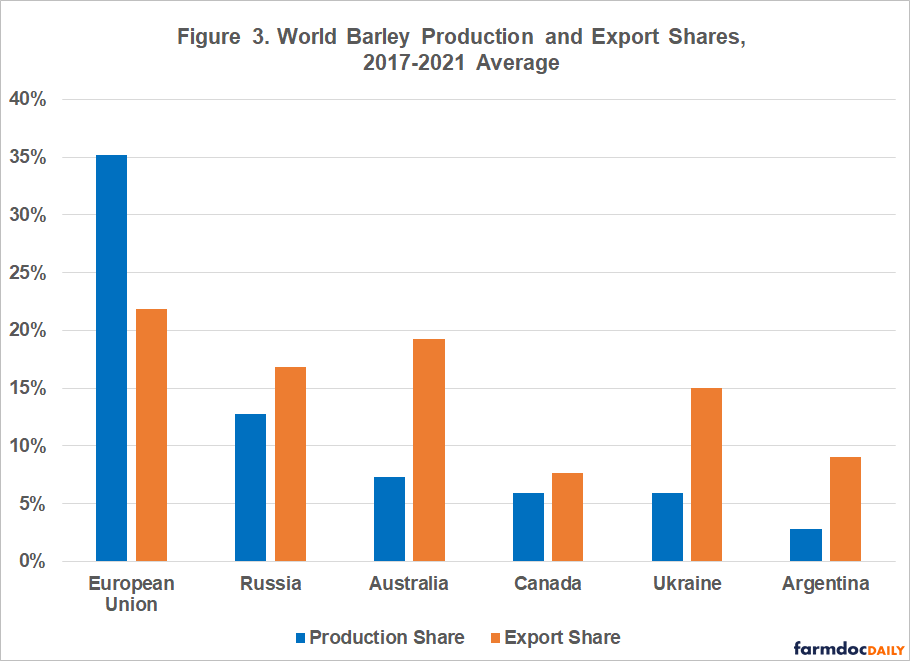

Barley

While the EU holds the dominant production share and is the leading region for world barley exports, Russia and Ukraine account for about 19% of barley production and nearly 32% of barley exports. Australia, Canada, and Argentina are the other major contributors to world barley production and exports.

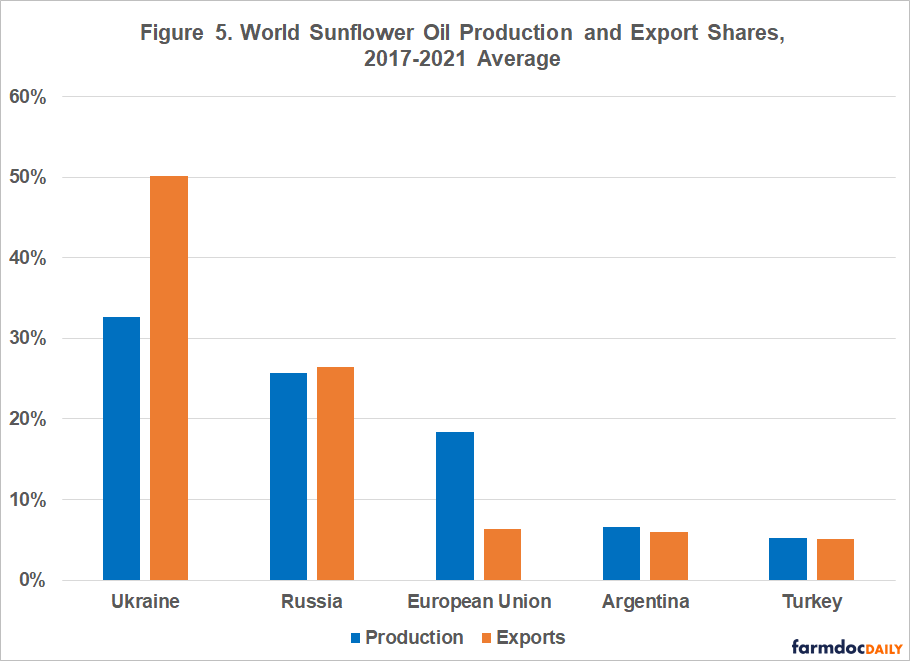

Soybeans and Vegetable Oil

The global soybean market continues to be dominated by the U.S. and South America. Over 82% of world soybean production and nearly 90% of soybean exports come from the U.S., Brazil, and Argentina. Both Russia and Ukraine rank in the top 10 for soybean production and exports, but represent just 2.3% of world production and 2.1% of world exports.

However, Ukraine and Russia are the leading producers and exporters of sunflower oil which comprises a 9% production share and nearly a 2% export share for the world vegetable oil market. Nearly 60% of world sunflower oil production occurs in Ukraine and Russia, and the two countries account for over 75% of world exports.

Discussion

The broad economic implications of last week’s Russian invasion of Ukraine, and the resulting sanctions imposed on Russia by the international community, could include disruption of trade flows, greater inflationary pressures, and an increase in volatility across a wide range of global markets.

The invasion is likely to impact the spring planting season for Ukrainian farmers, the magnitude of which will depend on the length and severity of the conflict. Diversion in trade flows will lead to price pressures and increased volatility for the agricultural commodities for which Russia and Ukraine play relatively large roles in terms of global production and trade. This increased volatility was seen in trading activity last week in wheat and corn futures which included limit (maximum) price moves both up and down across multiple days.

The inability for Ukrainian and Russian agricultural commodities to reach global markets may result in higher prices than would have otherwise occurred to the benefit of grain and oilseed producers in other major producing and exporting countries such as the U.S. However, the market disruptions stemming from the conflict and Russian sanctions will also result in major economic costs. Higher agricultural commodity prices will hurt net agricultural importers, particularly in developing parts of the world.

Other costs of the conflict may also hit U.S. agriculture: Increased volatility introduces both opportunities and challenges from a risk management standpoint. Higher prices for agricultural inputs would offset the benefit of higher corn, soybean, and wheat prices for U.S. farmers to some as yet unknown degree. Russia and its ally Belarus are major world suppliers of energy and fertilizer products which could be severely impacted by sanctions (Glauber and Laborde, 2022). With energy and fertilizer prices and volatility already at high levels, the invasion of Ukraine creates additional uncertainty regarding input costs and availability that still might impact the 2022 crop year and also extend to future crop years.

References

Glauber, J. and D. Laborde. “How will Russia’s invasion of Ukraine affect global food security?” International Food Policy Research Institute (IFPRI) Blog: Issue Post. February 24, 2022.

He, X., D.J. Hayes, and W. Zhang. 2021. “China’s Agricultural Imports under the Phase One Deal: Is Success Possible?” CARD Policy Brief 20-PB 29, Iowa State University.

Zulauf, C. "The Changing Distribution of World Corn Production in the 21st Century." farmdoc daily (10):199, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, November 18, 2020.

Zulauf, C. "Kazakhstan, Russia, Ukraine (KRU) and World Grain Markets." farmdoc daily (2):197, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 11, 2012.

Zulauf, C., A. Lines and N. Pryshliak. "Spanning the Globe – Corn, Soybean, and Wheat Production and Exports since 2000: Focus on the Black Sea Area and the U.S.." farmdoc daily (7):102, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, June 2, 2017.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.