Specialty Corn and Soybean Market Opportunities

Lower commodity prices and high production costs have led to a margin squeeze for grain producers in the Corn Belt since 2023. This has led to increased interest in crop production alternatives that may offer better returns. Specialty corn and soybean markets are one alternative which can offer similar but higher-value types of the crops they already grow. We show historic spot market premiums that have been available to producers for food grade and organic corn and soybeans in Illinois and the Corn Belt region. After accounting for typical yield drag, premiums on these alternative markets have offered significantly higher revenue potential than conventional corn and soybean production. But the higher revenues need to be weighed against their costs of production and risks specific to these markets.

Spot Market Price Premiums

Corn and soybeans have widely available benchmark prices such as the CME nearby futures price. Most local markets in the US Corn Belt have bids quoted basis (relative to) these global benchmarks. The cash prices for specialty types of corn and soybeans can also be stated relative to widely available commodity price benchmarks but the linkages aren’t as strong and exhibit greater basis variability.

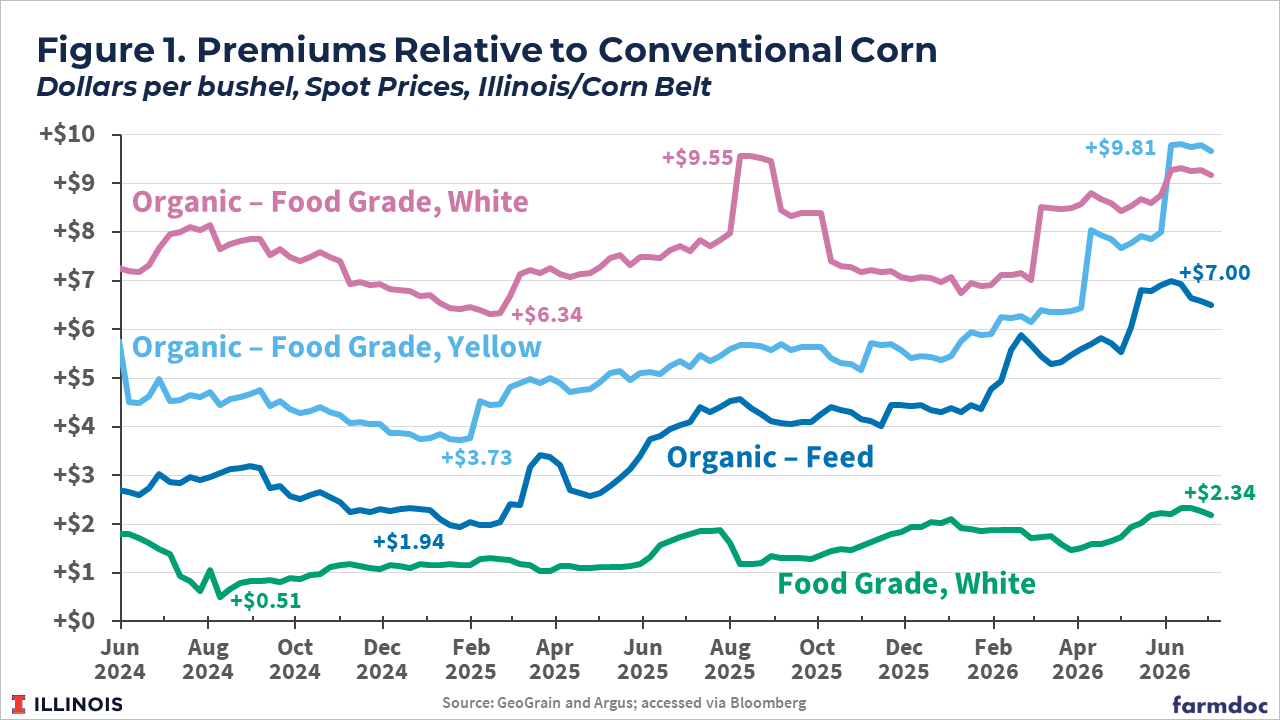

Figure 1 shows spot market price premiums over the past two years for 4 different types of specialty corn: food grade white corn, feed grade organic corn, food grade organic corn, and food grade white corn, relative to the average spot price for conventional yellow corn at local elevators throughout the state of Illinois. The high and low premiums over the two year period are labeled for each type.

Food grade white corn premiums have varied between $1 and $2 per bushel above the price for conventional (yellow) corn, averaging $1.44 per bushel over the past two years. Premiums during the harvest marketing period (mid-September to mid-November) have averaged $1.22 per bushel above conventional corn.

Organic feed (yellow) corn premiums have averaged $3.83 above conventional, with harvest time averages around $3.36 per bushel. Organic food grade corn premiums have averaged $5.45 (yellow) and $7.63 (white) above conventional corn, with harvest time averages being slightly lower for organic food grade yellow corn ($4.90).

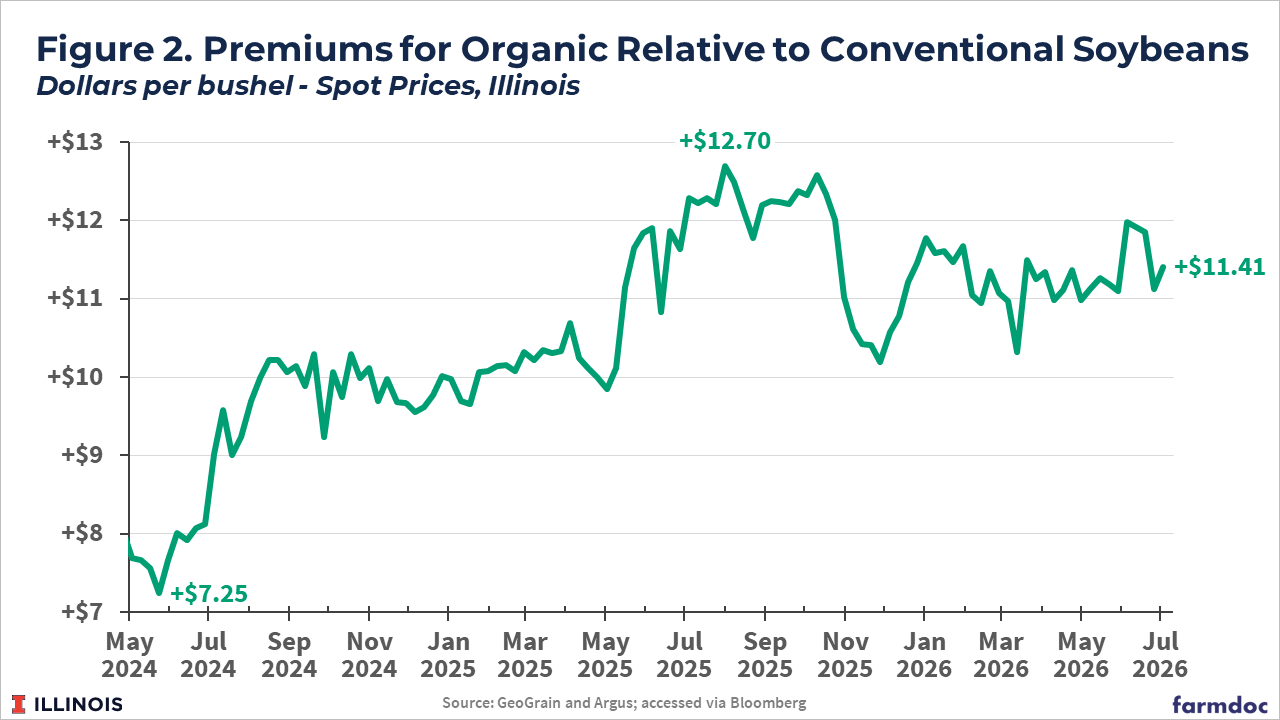

Figure 2 shows average spot premiums for organic soybeans relative to conventional. Organic soybean premiums in Illinois have range from +$7.25 to +$12.70 over the past two years, averaging +$10.58. The average harvest time premium during the 2024 and 2025 crop years was +$10.87 per bushel.

Specialty corn and soybean price premiums are larger and more variable than those observed for conventional corn. For instance, Figures 1 and 2 show changes in price premiums of $1-2 per bushel or more are relatively common for organic corn and soybeans. Similar changes would be considered extraordinary basis volatility in conventional markets.

Potential Revenue Implications

The spot price premiums illustrated in the previous section imply greater revenue potential for specialty corn and soybeans even after accounting for typical yield drag, the lower yield for specialty types relative to conventional production. For our purposes conventional refers to the hybrids and varieties, typically with genetic modification, producers select for commodity corn and soybean production.

A recent farmdoc webinar focused on Premium Crop Market Opportunities discussed typical ranges for yield drags for specialty crops in Illinois. For corn these range from a minimal yield drag for white food grade corn to 30-50 bushels per acre for organic feed or food grade corn. For soybeans, the yield drag for organic is typically in the range of 10-15 bushels per acre.

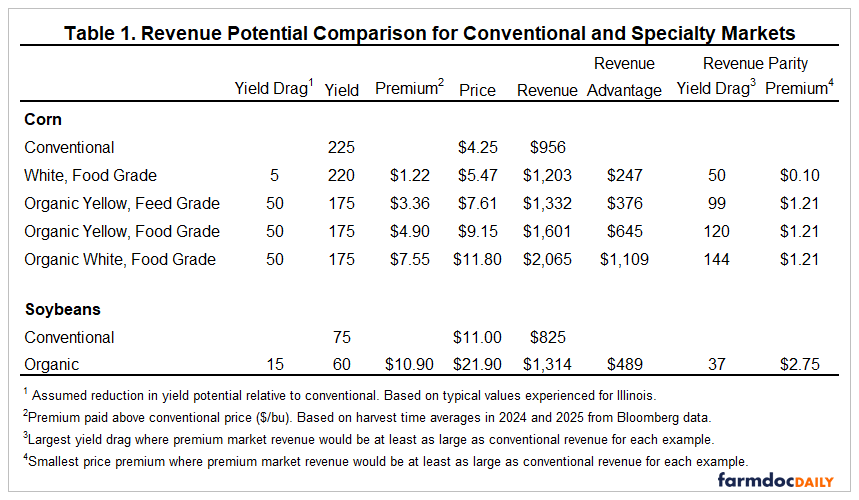

Table 1 provides some revenue comparisons between conventional corn and soybeans to some of the premium market specialty types. A 5 bushel per acre yield drag was assumed for white food grade corn while the upper end of the typical ranges were used for organic corn and soybeans. Conventional corn and soybean prices were set at $4.25 and $11 per bushel, respectively, with premiums for the alternatives set at harvest time averages over the last two crop years.

Average revenue advantages for specialty corn range from +$247 per acre for white food grade to +$1,109 per acre for organic white food grade. The average revenue advantage for organic soybeans is +$489 per acre.

The last two columns of table 1 calculate the yield drag and price premium that would make per acre revenues equal between the conventional and specialty alternative. We call these the “revenue parity” yield drag and price premium. At the average conventional price and premium levels, the yield drag on food grade white corn could be as large as 50 bushels per acre compared to 225 bushel per acre conventional corn yield. This increases to 99 bushels per acre for organic feed corn, and to 120 and 144 bushels per acre for organic food grade yellow and white corn, respectively. The premium for white food grade corn could be as low as $0.10 per bushel with the 5 bushel yield drag when comparing to average conventional yields and prices. The organic premiums could be as low as $1.21 per bushel with a 50 bushel yield drag compared to 225 bushel per acre conventional corn at $4.25 per bushel.

The yield drag on organic soybeans could be as high as 37 bushels per acre before revenue would fall below that for conventional soybeans. The premium for organic soybeans could be as low as $2.75 per bushel.

The revenue parity yield drags and price premiums indicate substantial revenue advantages for specialty crop production. The revenue parity yield generally exceeds realized yield drags. Price premiums observed in Figures 1 and 2 are substantially greater than the revenue parity levels.

Other Considerations

While spot price premiums over the past two years show clear revenue advantages for specialty corn and soybean markets relative to conventional, a number of other important factors need to be considered.

Premium markets typically involve a different set of management activities and requirements relative to their conventional commodity counterparts, which can result in higher production costs as well as additional management challenges. Many of these challenges are specific to the type of specialty production. For example, a recent farmdoc daily article (June 30, 2026) discussed some of the management practice and cost differences between non-GMO and GMO soybeans. More generally, producers may consider the following:

- Segregation requirements are a factor for all specialty markets. At a minimum this will involve careful planning and approaches to planting to avoid cross-pollination in the case of specialty corn types. Equipment must be thoroughly cleaned during planting, harvest, and transport particularly if the operation is switching between specialty and conventional varieties during the crop year.

- Sufficient on-farm storage may be needed if the producer wants the ability to market and deliver outside of the harvest window. Contracted specialty production may require on-farm storage, particularly if delivery is staggered at different points of the year.

- Organic corn and soybeans, while typically offering larger premiums compared with other specialty markets, involve even larger management adjustments as well as a three-year transition period and annual audits to maintain organic certification.

- The ability to sell into premium markets may also require more thorough records be provided for documentation and verification compared with conventional commodities.

- Selling into spot specialty markets can be risky as premiums and demand can be volatile. Spot market buyers may not offer premiums or even the ability to deliver, forcing the producer to identify alternative markets. Importantly, not all specialty hybrids or varieties may be able to be sold into conventional markets if a premium market is not available. Identifying contracting opportunities with premium market buyers can help to manage this risk.

- Many of the costs of specialty crop production and marketing come from additional management and labor requirements which are difficult to estimate precisely on a per acre basis and can vary widely across farm operations. This complicates profitability comparisons between conventional and specialty crop production.

Conclusions

Price premiums for specialty corn and soybeans are sufficient to generate higher revenues per acre and offset the yield drag associated with specialty crop production. However, price premiums are variable, and the higher costs and management requirements associated with specialty production must be considered at the farm-level to determine if pursuing specialty market production makes sense for the operation.

Readers are encouraged to view the recording of our recent Premium Crop Market Opportunities webinar which includes resources for those who might be interested in learning more about specialty market and contracting opportunities.

References

Schnitkey, G., L. Gentry, N. Paulson and C. Zulauf. "Non-GMO Soybeans Profitability: Experience from PCM." farmdoc daily (16):114, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, June 30, 2026.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.