The Iran Conflict and Fertilizer Markets: Why Brazil Faces Greater Near-Term Risk than the U.S.

Latest developments in the Middle East, including the Strait of Hormuz closure, have repercussions on energy, fertilizers, and commodity markets (see farmdoc daily, March 23, 2026; March 24, 2026, and March 27, 2026). Fertilizer prices have soared well above historical averages. For U.S. farmers, these price movements, along with supply risks, could have large impacts on the 2027 crop year, especially if conflict persists through fall fertilizer purchase decisions. For Brazilian farmers, the impact on the 2026/27 crop will be felt sooner as planting the first crop will begin in September and usual soybean fertilizer decisions are happening now. Moreover, Brazil has a higher exposure to fertilizer imports than does the U.S. Hence, the conflict could impact fertilizer purchase decisions, and ultimately Brazil’s soybean global competitiveness.

Background on the Conflict

On February 28, the United States and Israel launched military strikes against Iran, triggering an escalation that has since disrupted global commodities and input markets. The Middle East is both a major production hub and critical logistics channel for fertilizers (see farmdoc daily, March 23, 2026 and March 27, 2026). As a result of the conflict, the Strait of Hormuz, which is responsible for moving roughly one-third of seaborne traded fertilizer, has often been closed while negotiations happen.

As of April 10, tentative signs of de-escalation between the U.S. and Iran briefly improved financial market sentiment, but conditions in the Strait of Hormuz remain disrupted. As a result, concerns over global fertilizer and oil supply disruptions, along with elevated prices, continue to weigh on cropping decisions in both the U.S. and Brazil.

Brazil and U.S. Exposure to Fertilizer Supply Shocks

Despite both being major fertilizer consumers (see farmdoc daily July 29, 2025), Brazil and the U.S. face different exposure to global markets. In Mato Grosso (Brazilian Center-West), soybeans are typically planted in the Southern Hemisphere spring (October-November) and harvested in the Southern Hemisphere summer (January-March). A second corn crop (known as “safrinha”) follows, where planting occurs with or right after soy harvesting. Corn is then harvested in June-July. This translates into different fertilizer decision windows. While in the U.S. Midwest, the bulk of fertilizer pricing usually happens during the fall to early spring, decisions for Brazilian farmers are usually concentrated from February to May for soybeans and July-November for corn.

Soybeans’ main applied crop nutrients are phosphate and potash, while corn is the main consumer of nitrogen. In general, Brazil is much more dependent on imports. The share of consumption met by imports of Nitrogen, Phosphate, and Potash (NPK) between 2020 and 2023 was about 90%, reaching about 99% in 2023 (Pereira and Cardoso, 2025).

The U.S. has a greater nitrogen production capacity domestically (see farmdoc daily, July 29, 2025), which decreases risks for nutrient shortages, although prices are still impacted. For nitrogen, Brazil relies on urea as the main nitrogen fertilizer, primarily from Russia and China, while the U.S. has a more mixed profile.

Similar to nitrogen, phosphate fertilizers production in the United States is largely domestic. Net import reliance for phosphate rock – the key mineral in phosphate fertilizers – reached 13% in 2024 (see farmdoc daily, July 29, 2025). Still, imports are important to the U.S. market, and nearly all phosphate rock imports are from Peru. Despite low reliance on phosphate rock, the U.S. imports about one-third of finished phosphate products – half of that from Saudi Arabia (see farmdoc daily, March 23, 2026). Brazil relies on imports mainly from Morocco and Russia.

For potash, both Brazil and the U.S. rely heavily on imports. Nevertheless, U.S. potash comes primarily from Canada, while Brazil also relies on Russia and Belarus, regions that were not materially affected by the recent conflict, though existing sanctions still pose risks.

Grain-to-Fertilizer Exchange Ratios

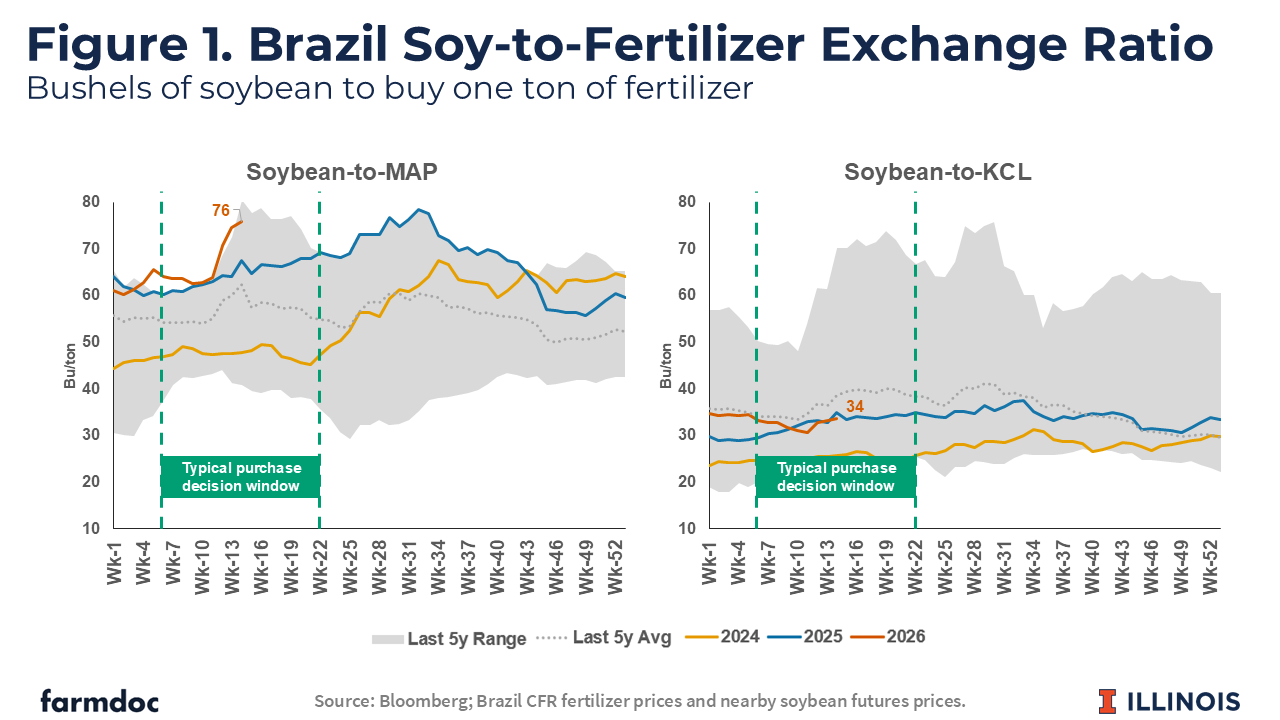

The uncertainty and physical closure of the Strait of Hormuz have resulted in increased fertilizer prices. However, it has not impacted corn and soybeans equally. To assess the effect on producer purchasing power, we utilize the ratio between fertilizer prices and commodity prices. The grain-to-fertilizer exchange ratio shows fertilizer prices relative to grain prices. In other words, how many units of output (i.e., bushels of grain) are necessary to purchase one ton of fertilizer. A higher ratio means producers’ purchasing power decreased, as more output is necessary to buy the same amount of fertilizer. A lower ratio means greater purchasing power. Soy-to-fertilizer exchange ratio for Brazil is shown in Figure 1.

Compared to the range of the last five years (shaded in gray), the story is different for potash (KCL) in comparison to other nutrients. Potash price ratios are very much in line with last year, and below the average over the last five years (dotted line). In contrast, the soy-to-fertilizer exchange ratio for phosphate (monoammonium phosphate (MAP)) has reached 76 bushels per ton by April 3. This is in line with the upper range observed in the last five years. Moreover, Brazil is in the purchase decision window for the 2026/27 soybean crop, an unfavorable timing for decision-making.

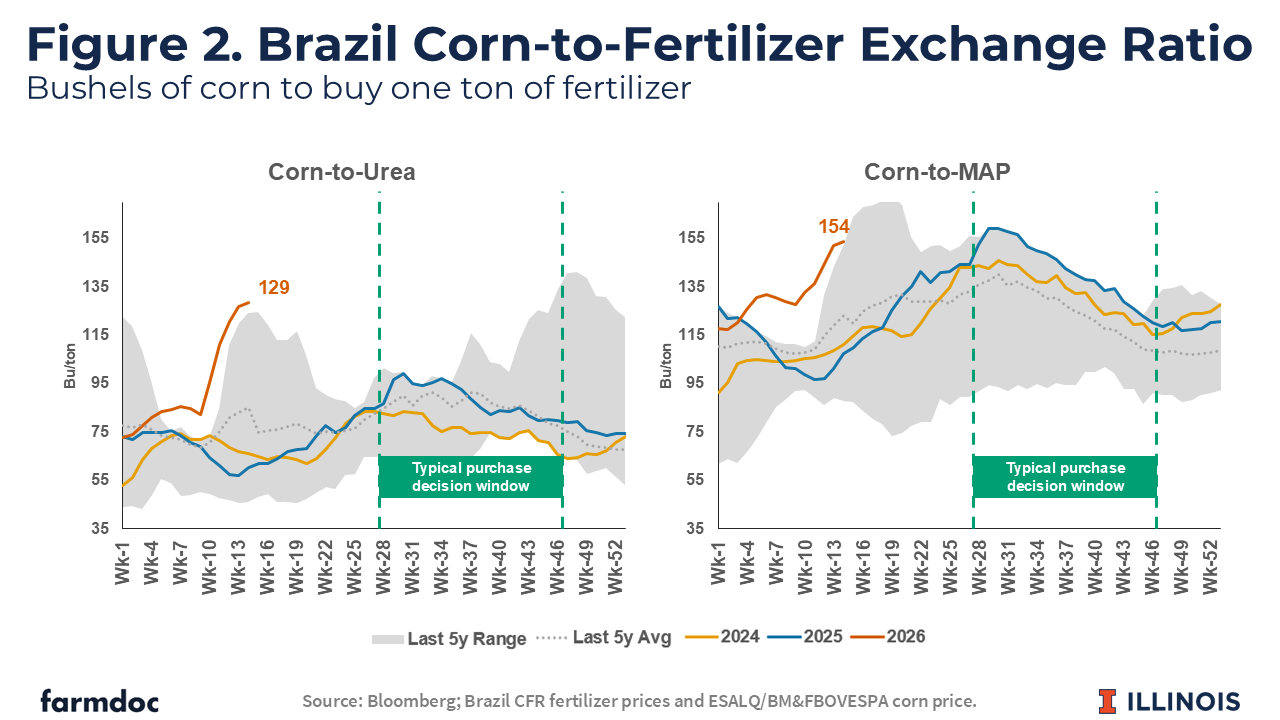

Figure 2 shows corn-to-fertilizer exchange ratio for urea and MAP. For phosphate, the relative cost of MAP for corn production is well above the last two crop years and is approaching the peak of the last five years.

Urea has reached its highest corn-to-fertilizer exchange ratio for this time of year in the past five years, approaching the five-year peak recorded in 2022 (the peak of the shaded area). Brazil’s 2026 corn crop is already planted, and fertilizers were likely already applied. Fertilizer decisions for the 2027 corn crop in Brazil typically do not happen until later in the year, giving farmers some time to make adjustments if prices continue to remain high as the conflict evolves.

Discussion

Grain-to-fertilizer exchange ratios, or relative fertilizer prices, have remained near multi-year highs since 2022, particularly for nitrogen and phosphorus, both for Brazil and the United States. While the timing may limit the overall impact on the 2026 crop in both countries, they face differing exposure and implications for the upcoming 2026/27 crop year.

U.S. farmers face lower overall supply risk than Brazilian farmers. The U.S. sources a larger share of fertilizer domestically (nitrogen and phosphate) and nearby partners for potash (Canada), limiting exposure to Middle East disruptions. Moreover, much of the fertilizer for the 2026 crop was already purchased and/or applied last fall, before the conflict began (see farmdoc daily March 17, 2026). For the remaining spring fertilizer needs, application rates can also be adjusted. For nitrogen, optimal application rates suggest that a slight reduction in quantity applied is an option (see farmdoc daily March 31, 2026). For potassium and phosphorus, soil testing can identify fields where reducing application rates won’t result in near-term yield loss (see farmdoc daily September 27, 2022 and October 21, 2022). Input decisions for the 2027 crop are still a few months away, providing U.S. farmers with greater flexibility to monitor how markets evolve before committing expenditures.

Brazilian soybean farmers are more constrained on both fronts. First, Brazil’s import dependency is high for all nutrients, resulting in limited isolation from global supply shocks. Agronomically, most of the Cerrado’s (main Brazilian soybean-producing region) soils are naturally deficient in P and K and have low capacity to buffer against application reductions (see farmdoc daily October 6, 2025 and Roy et al., 2016). Older soils with P banks might offer that option, but soils recently converted to crop production (primarily from degraded pastureland) might lack phosphorus reserves.

Critically, Brazil’s soybean fertilizer purchase window for the 2026/27 crop is happening now. By April 3, only about 30% of the estimated fertilizer volumes for the 2026/27 crop have been purchased, below the average of recent years (about 40%) (Itaú BBA, 2026). High relative prices are the primary driver of the low pace. Further, approximately 70% of the annual fertilizer imports occur between April and September (CNA, 2025). If the conflict persists, physical supply might be severely affected in addition to high prices, directly impacting management decisions, including optimal application windows. The 2027 corn crop decision is still a few months away, so it is hard to predict any impact as of now.

Lastly, the conflict has severely impacted oil and fuel prices (see farmdoc daily March 23, 2026 and March 17, 2026). Most of Brazil’s transportation is based on trucks, both to bring inputs from the ports to Mato Grosso, and also to take soybeans to the ports. An increase in diesel prices not only increase production costs but puts pressure on logistics costs, ultimately impacting farmers’ margins, and impacting Brazil’s soybean global competitiveness.

References

Arita, S., R. Chakravorty, J. Kim, W. Lwin and S. Steinbach. "Strait of Hormuz Closure and Fertilizer Supply Risks for U.S. Agriculture." farmdoc daily (16):48, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 23, 2026.

Confederação da Agricultura e Pecuária do Brasil (CNA). "Insumos CNA — Edição Novembro de 2025." Publicações CNA, November 2025. Available at: https://www.cnabrasil.org.br/publicacoes/insumos-cna-edicao-novembro-de-2025

Fontes, G. "Fertilizing with High-Priced P and K." Department of Crop Sciences, University of Illinois, October 21, 2022.

Itaú BBA Consultoria Agro. "Conflito EUA–Irã, instabilidade no Oriente Médio e impactos para o agronegócio brasileiro." Radar Agro, March 2026. Available at: https://www.itau.com.br/media/dam/m/672df6ac585bd451/original/Conflito-EUA-e-Ira_ItauBBA.pdf

Mashange, G. "The Strait of Hormuz: Why Global Trade Dependency Turns a Localized Conflict into a Global Crisis." farmdoc daily (16):52, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 27, 2026.

Monaco, H., G. Schnitkey and N. Paulson. "U.S. Fertilizer Industry in Global Markets: Structure and Supply Risks." farmdoc daily (15):137, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, July 29, 2025.

Paulson, N., G. Schnitkey, H. Monaco and C. Zulauf. "Nitrogen Prices Remain in Focus After Iran Conflict." farmdoc daily (16):49, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 24, 2026.

Paulson, N., G. Schnitkey, C. Zulauf and L. Gentry. "High Fertilizer Prices Suggest Reconsidering Application Rates." farmdoc daily (16):54, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 31, 2026.

Pereira, L.A.C. and V.M. Cardoso. "Qual é a dependência do agro brasileiro das importações de fertilizantes?" Insper Agro in Data, August 7, 2025. Available at: https://agro.insper.edu.br/agro-in-data/artigos/qual-e-a-dependencia-do-agro-brasileiro-das-importacoes-de-fertilizantes

Richards, P. and S. Meyer. "Comparative Cost Advantages for U.S. Corn and Soybean Production, and a Seed Cost Disadvantage in Soybeans." farmdoc daily (15):183, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 6, 2025.

Roy, E.D. et al. (2016) “The phosphorus cost of agricultural intensification in the tropics,” Nature Plants, 2(5). Available at: https://doi.org/10.1038/NPLANTS.2016.43.

Schnitkey, G., C. Zulauf, N. Paulson and J. Baltz. "The Iran Conflict: Potential Impacts on 2026 Corn and Soybean Returns." farmdoc daily (16):45, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 17, 2026.

Schnitkey, G., N. Paulson, C. Zulauf, K. Swanson and J. Baltz. "Fertilizer Prices, Rates, and Costs for 2023." farmdoc daily (12):148, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, September 27, 2022.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.