Impacts of Consolidation in Ag Inputs: Evidence from a Farmer Survey

Farmers were surveyed in the fall of 2024 on their concerns of consolidation within the fertilizer, crop protection, seed, and machinery sectors. Results suggest that farmers are concerned that consolidation at the manufacturing and retail levels will lead to higher input prices and reduce the customer service received. Concerns didn’t vary significantly across the different input sectors but concerns were greater that consolidation will increase prices than reduce customer service.

Farmer Survey

In the fall of 2024, we conducted an online survey of farmers as part of a research project supported by the Illinois Corn Growers’ Association. The purpose of the study was to assess the state of local markets for fertilizers and other inputs for agricultural producers (results from other aspects of the survey were summarized in the farmdoc daily article from July 22, 2025). The survey included questions that asked respondents their opinions on how consolidation at the manufacturing and retail levels for various inputs (fertilizers, crop protection, seed, and machinery) would impact the prices they paid for those inputs and the customer service that they would receive. Consolidation was defined as the trend towards fewer, and usually larger, firms offering products and services.

Each input question had at least 220 responses to the questions related to consolidation impacts. Farmers from 25 different US states responded to the consolidation questions, with an average of 43% of the responses coming from farmers in Illinois.

The questions asked respondents to rate the impact of consolidation on a scale from 1 to 5. Negative consequences of consolidation (i.e. higher prices, reduced customer service) were associated with lower rating values while benefits associated with consolidation (i.e. lower prices, improved customer service) were associated with higher rating values. For the impact on prices, a rating of 1 or 2 meant consolidation would lead to significant increases (1) or increases (2) in prices, respectively. A rating of 3 meant no impact of consolidation on prices. Ratings of 4 or 5 indicated reductions (4) or significant reductions (5) in input prices due to consolidation. Impacts on customer service were measured in a similar way with the following options: significantly reduce (1), reduce (2), no impact (3), increase (4), and significantly increase (5).

The survey results are summarized in the sections below by input sector (fertilizer, crop protection, seed, machinery) and the level, or supply chain stage, at which consolidation may occur (manufacturing versus retail).

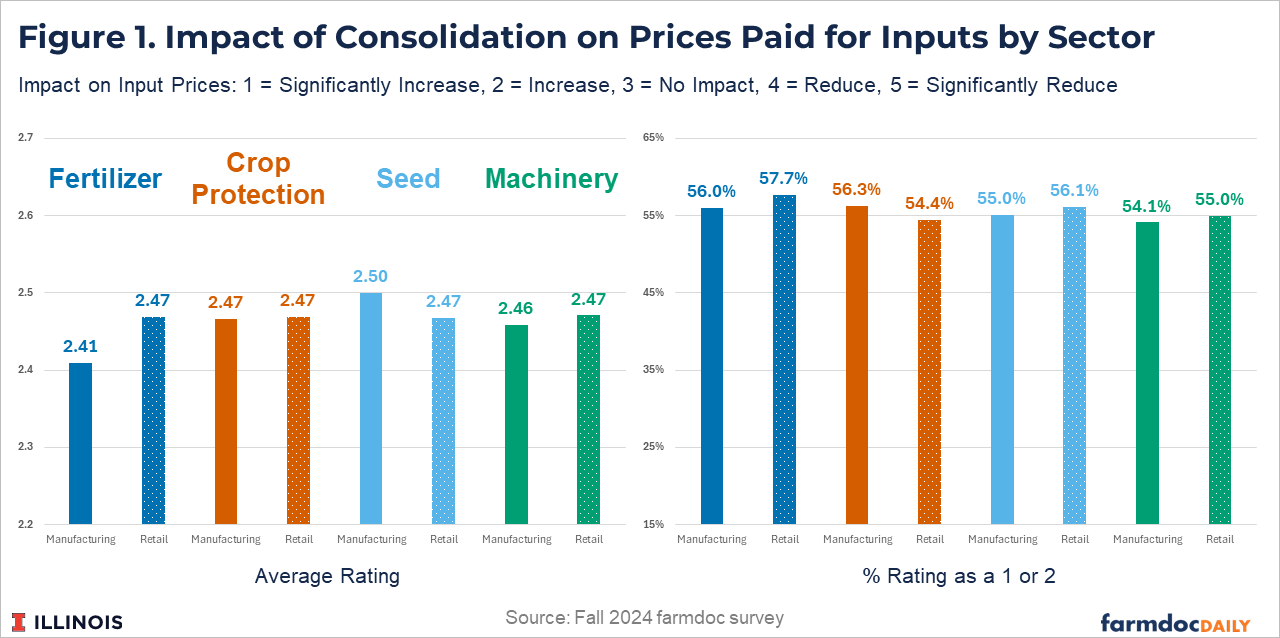

Consolidation and Input Prices

Figure 1 summarizes the farmer respondents’ opinions as to how consolidation might impact input prices. The left panel of Figure 1 provides the average rating for each input sector and level of consolidation. The average ratings do not vary considerably across sectors or level of consolidation. Average ratings range from 2.41 (fertilizer manufacturing) to 2.50 (seed manufacturing). These averages suggest most farmers expect consolidation to increase input prices across all sectors and levels of consolidation considered.

The right panel of Figure 1 provides the percentage of farmer respondents who indicated that consolidation would increase or significantly increase input prices. This represents the proportion of respondents who think consolidation would have negative consequences on input prices. Similar to the average ratings, these percentages do not vary considerably across input sector or the level at which consolidation occurs. A slightly larger share of farmers feel higher prices will occur due to consolidation at the retail level rather than at the manufacturing level for fertilizers, seed, and machinery while the opposite is true for crop protection inputs. However, the differences between manufacturing and retail consolidation are not large for any of the input sectors.

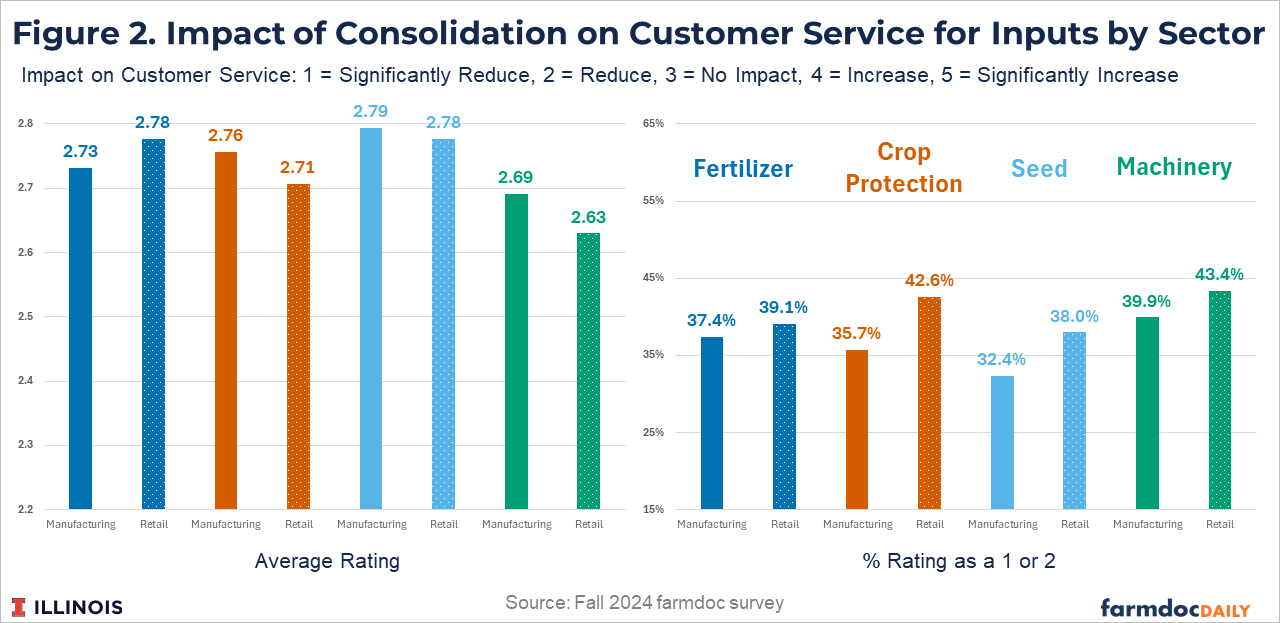

Consolidation and Customer Service

Figure 2 provides a similar summary of the results related to consolidation’s impact on customer service received across input sectors. The average responses from farmers suggest consolidation will lead to reductions in customer service in all four of the input sections (average ratings are below 3 for all cases). The average ratings tend to be higher than those in Figure 1 implying that farmers think that the negative impacts of consolidation are more concerning in terms of increasing input prices compared with its negative impact on customer service.

The results in the right panel of Figure 2 tend to support the idea that higher prices are of greater concern than reductions in customer service. The proportion of respondents who thought customer service would be significantly reduced or reduced (i.e. rated a 1 or a 2) are lower for all input sectors compared with those expecting significantly higher or higher input prices (right panel of Figure 1). These percentages range from 32.4% expecting poorer customer service as a result of consolidation in seed manufacturing to 42.6% expecting poorer customer service as a result of consolidation at the retail level in crop protection. In addition, the perceived negative impact on retail relative to manufacturing is higher on customer service than it is on prices, indicating that customer service would be more impacted with consolidation at the retail level.

Discussion

The results from a survey suggest concerns exist among farmers that consolidation in major agricultural input sectors will lead to higher input prices paid, and poorer customer service received. The results did not show significant differences in the degree of concern over the impacts of consolidation across fertilizer, crop protection, seed, and machinery. Consolidation has occurred across all of these sectors over time, a topic discussed – with particular focus on the nitrogen fertilizer industry – in previous farmdoc daily articles (see farmdoc daily articles from May 26, 2026 and April 5, 2022 as examples).

The impacts and consequences of consolidation for agricultural producers have seen renewed interest in recent months, as rising input costs have intensified concerns about market concentration and market power (see farmdoc daily article from June 1, 2026). In particular, consolidation in the fertilizer industry is receiving heightened attention as a result of the price increases that have occurred since the conflict between the U.S. and Iran began at the end of February (see farmdoc daily article from May 5, 2026).

We do note that the survey was conducted in the fall of 2024, and farmer sentiment is likely to vary through time. If the survey were to be repeated now, one might expect the responses to suggest even stronger opinions towards negative impacts from consolidation through higher input prices and, perhaps to a lesser extent, poorer customer service.

References

Monaco, H., N. Paulson and G. Schnitkey. "Factors Influencing Nitrogen Fertilizer Application Rates and Timing in Illinois." farmdoc daily (15):133, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, July 22, 2025.

Monaco, H., N. Paulson, G. Schnitkey and C. Zulauf. "Consolidation Trends in the U.S. Nitrogen Fertilizer Industry." farmdoc daily (16):91, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, May 26, 2026.

Schnitkey, G., C. Zulauf and N. Paulson. "Fertilizer Cost Increases Resulting from the Iran Conflict." farmdoc daily (16):78, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, May 5, 2026.

Schnitkey, G., N. Paulson, C. Zulauf, K. Swanson, J. Colussi and J. Baltz. "Nitrogen Fertilizer Prices and Supply in Light of the Ukraine-Russia Conflict." farmdoc daily (12):45, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 5, 2022.

Zulauf, C., J. Coppess, G. Schnitkey, N. Paulson and H. Monaco. "Concentration and Monopoly Pricing: What Economics Tells Us." farmdoc daily (16):95, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, June 1, 2026.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.