Fertilizer Cost Increases Resulting from the Iran Conflict

Fertilizer costs in central Illinois have risen significantly following the onset of conflict involving Iran. Based on April pricing compared to the six months prior to the conflict, costs have increased by more than $20 per acre. While many producers may see smaller impacts in 2026 due to pre-purchased inputs, the full effect of these price increases will be felt in 2027. These developments highlight the importance of actively managing fertilizer costs.

Fertilizer Price Increases

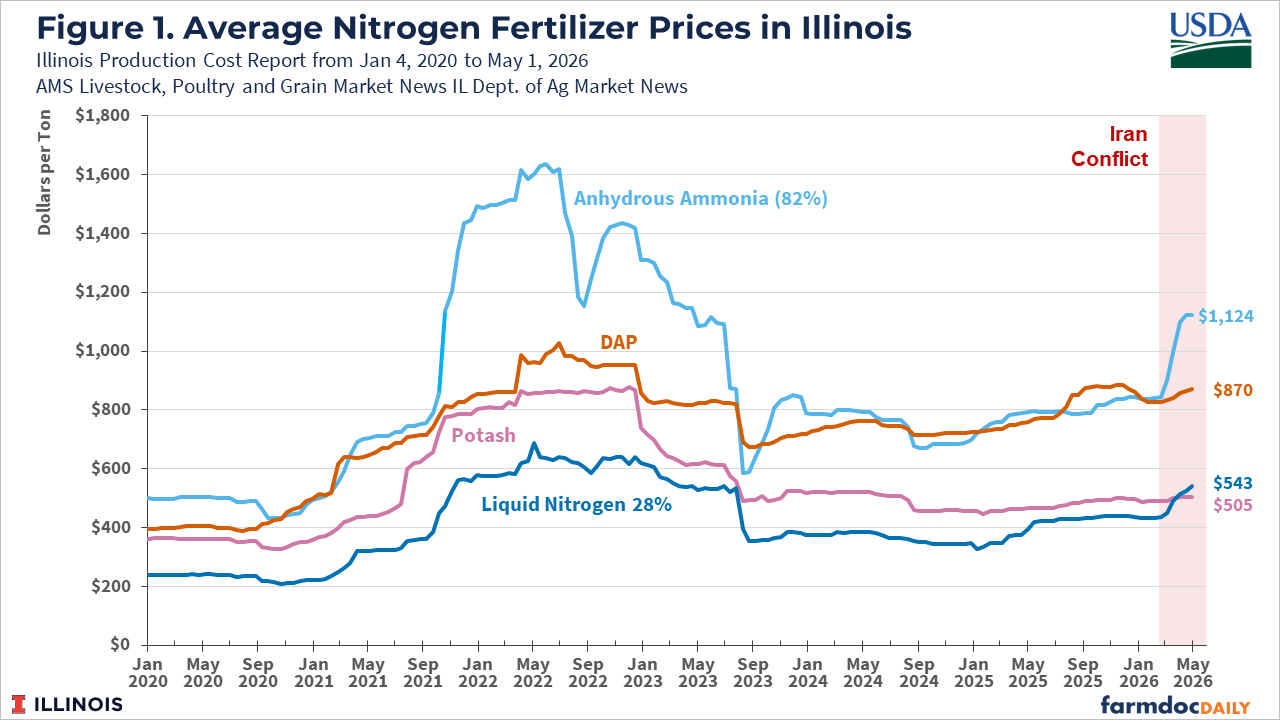

Nitrogen fertilizer prices have increased sharply since February 28, 2026, when hostilities began between Iran, the United States, and Israel. Prices rose further as the conflict escalated and the Strait of Hormuz—a critical shipping route for energy and nitrogen fertilizers—was closed. Prior to the conflict, anhydrous ammonia averaged $828 per ton from September 2025 through February 2026, a period during which many farmers made fertilizer purchases for the 2026 crop. By April 17, 2026, the USDA Agricultural Marketing Service reported a price of $1,123 per ton in its Illinois Production Cost Report, representing a substantial increase over the pre-conflict average (see Figure 1). Similarly, 28% nitrogen solution prices rose significantly over the same period, increasing from $436 for September-to-February to $543 per ton as of May 1st, an increase of 25%.

In contrast, phosphate (DAP) and potash prices have increased much less. DAP increased from $862 pre conflict to $870 in the May 1st report. Potash increased 2% from $493 per ton to $505 per ton. Current demand for DAP and potash is relatively low because most applications occur in the fall and early spring, and much of that fertilizer had already been applied before the conflict began. Moreover, the Middle East is a major supplier of nitrogen fertilizers—particularly urea (see farmdoc daily, March 17, 2026). The Middle East provides relatively less finished DAP and potash fertilizer products. However, the Middle East does supply sulfuric acid, which is used to make phosphate fertilizers. Extended supply disruptions could lead to higher phosphate fertilizer prices (see farmdoc daily, April 29, 2026).

Impact on Fertilizer Costs on Midwest Farms

The impact of higher fertilizer prices varies across farms depending on the timing of fertilizer purchases and the type of nitrogen fertilizer used. Farms that purchased fertilizer prior to February will see limited impacts on 2026 production costs. In contrast, farms that delayed nitrogen purchases are exposed to recent price increases. Anhydrous ammonia is typically the lower-cost nitrogen source compared to nitrogen solutions. All farms are expected to face significantly higher costs for the 2027 crop.

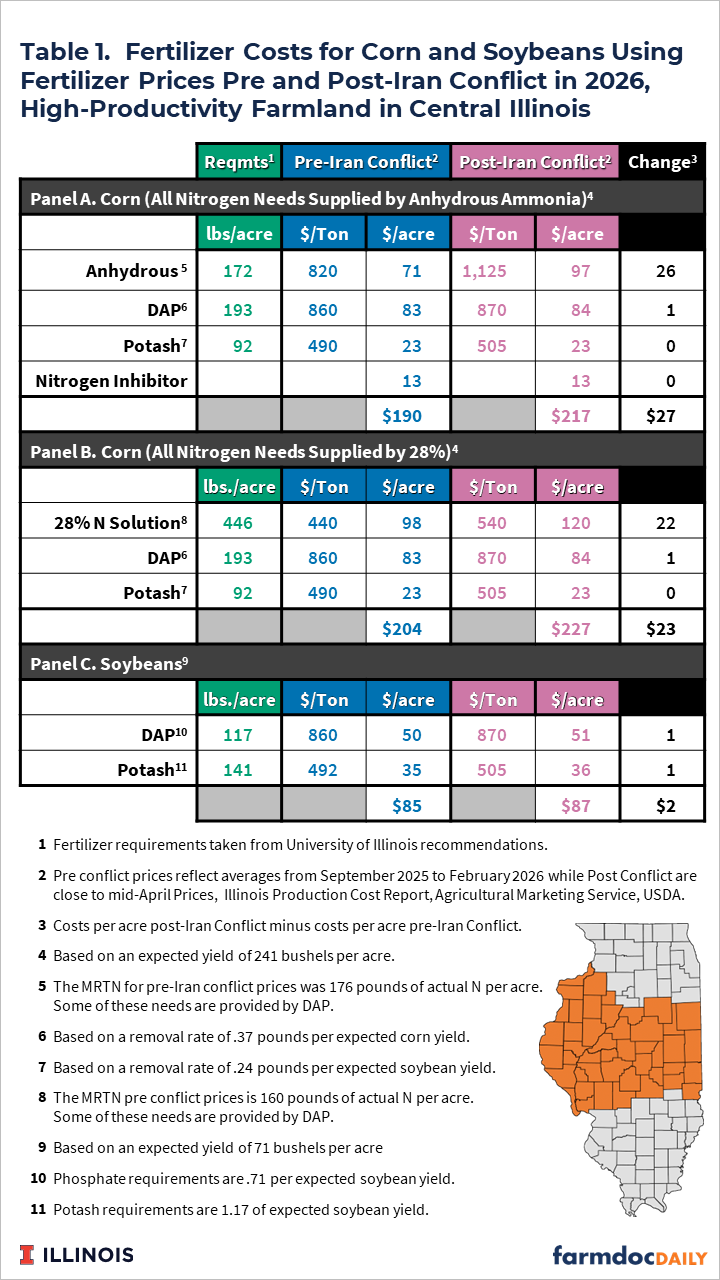

The effects of fertilizer type and timing are illustrated in Table 1, which presents estimated fertilizer costs for corn and soybeans. Fertilizer requirements are based on University of Illinois recommendations, using the Maximum Return to Nitrogen (MRTN) framework. Because MRTN rates changed little despite higher prices, pre-increase application rates are used for both pricing scenarios. Phosphorus and potassium are applied at removal rates, assuming soil test levels are at or above recommended levels.

Corn Fertilizer Costs: When anhydrous ammonia is used as the primary nitrogen source for corn, total fertilizer costs increase from approximately $190 to $217 per acre, a $27 per acre increase (see Panel A of Table 1). Most of this increase is driven by ammonia, with costs rising from about $71 to $97 per acre.

However, much of the application of anhydrous ammonia occurs in late fall or early spring. As a result, many farmers who rely on ammonia likely secured fertilizer before the conflict and will face costs closer to pre-conflict levels in 2026.

When a 28% nitrogen solution is used as the primary nitrogen source, fertilizer costs increase from approximately $205 per acre to $227 per acre, a $23-per-acre increase (see Panel B of Table 1). Nitrogen solutions typically have higher nitrogen costs than anhydrous ammonia. In Table 1, under post-Iran conflict prices, fertilizer costs are $217 per acre for anhydrous ammonia, $10 per acre lower than $227 per acre for nitrogen solutions. Many farmers prefer nitrogen solutions due to safety considerations and ease of handling. In addition, nitrogen solutions are more commonly applied after planting, meaning a larger share of these inputs may not have been priced before the conflict. As a result, farms relying on nitrogen solutions may be more exposed to recent price increases.

Soybean Fertilizer Costs: Fertilizer costs for soybeans have changed little. Because DAP and potash price increases have been modest, total DAP and potash fertilizer costs rose only slightly—from about $85 to $87 per acre (see Panel C of Table 1). This limited change reflects the small price increases.

Implications for 2026 Decision-Making

The Iran conflict occurred relatively late in the 2026 planning cycle. Most farmers had already made production decisions and purchased a significant portion of their inputs. Farmers who had not yet priced nitrogen inputs will face a cost disadvantage relative to those who purchased earlier. As a result, the overall impact of the 2026 price increases will be uneven.

Some farmers with unpriced nitrogen may consider switching acreage from corn to soybeans to reduce nitrogen costs. At that point, changes in corn and soybean prices may enter into decisions as well

- Corn: For central Illinois, forward prices for 2026 fall delivery during February averaged $4.25 per bushel. This week, fall delivery prices were $4.60. Given an expected corn yield of 241 per acre, the higher corn price has increased expected revenue by $96 per acre. The $96 revenue increase is $73 per acre more than the $23 per acre increase in fertilizer costs

- Soybeans: For central Illinois, forward prices for 2027 fall delivery averaged $10.70 during the month of February. The forward price this week is $12 per bushel. That price increase resulted in a $72 increase in expected revenue. Soybean fertilizer costs have increased only $2 per acre.

Even given fertilizer cost increases, expected revenue above fertilizer costs has increased for both corn and soybeans: $73 per acre for corn and $70 per acre for soybeans. Those increases are similar, suggesting that the relative profitability of the two crops has not changed much. Overall, soybeans had been projected to be more profitable than corn under pre-conflict conditions (see farmdoc daily, January 13, 2026). Therefore, relative profitability has not changed to an extent that would be expected to significantly impact late acreage adjustments.

Anhydrous ammonia continues to offer a cost advantage over nitrogen solutions, consistent with historical patterns. Farmers may consider expanding ammonia use in future years to reduce costs. However, this shift involves tradeoffs, including slower application speeds, safety considerations, and increased management requirements—particularly for post-plant applications.

Also, farmers should consider lowering rates, particularly if the current rates are above Maximum Return to Nitrogen rates (see farmdoc daily, March 31, 2026).

Implications for 2027 Decision-Making

The planning season for the 2027 crop will get underway in earnest in September, when many inputs will be available for purchase and pricing. It is unlikely that nitrogen fertilizer prices will return to pre-conflict levels (see farmdoc daily, March 24, 2026). There will be lags in fertilizer prices (see farmdoc daily, April 24, 2026, and the status of the conflict will impact price levels (see farmdoc daily, April 29, 2026). Anhydrous ammonia prices will likely be significantly above $1,000 per ton. Moreover, DAP supplies are reportedly tight, increasing the likelihood of higher phosphate prices as well, perhaps near $1,000 per ton.

Given these conditions, farmers may need to adjust fertilizer strategies. We suggest three considerations:

Lower Rates: Many farmers apply nitrogen at rates above university-based recommendations, and soil test levels for phosphorus and potassium are above maintenance levels. In these cases, lowering rates will increase profitability, as university-based rates are set with economic considerations in mind. The reduction in returns associated with applying above economically optimal rates will be greater with high nitrogen and DAP prices (see farmdoc daily, March 31, 2026).

Switch to Anhydrous Ammonia: Ammonia is the least-cost nitrogen source. Moving to anhydrous ammonia will reduce fertilizer costs.

Move Anhydrous Ammonia Applications to Post-Plant: Moving ammonia from fall to post-plant eliminates the need for nitrogen inhibitors. That $13 expense represents a significant cost savings. That move may require additional planning, and the risk of not being able to apply nitrogen becomes a concern. PACE — an insurance policy which pays in the event of not being able to apply nitrogen (see farmdoc daily, October 11, 2022) — may be a strategy for reducing risks,

In addition, it may be difficult, from a psychological standpoint, to pre-price nitrogen in the fall at very high price levels. Hopes may exist that prices fall going into spring, as may be predicted by models of the fertilizer market (see farmdoc daily, April 29, 2026). How that plays out will depend on the stage of the Iran conflict and whether a resolution has been achieved by the fall.

Higher nitrogen prices also suggest examining crop rotation decisions for 2027. Higher nitrogen fertilizer prices make corn less profitable relative to soybeans. However, there may be relative price changes between corn and soybeans to consider. Cropping decisions in Brazil will come into play. Brazil has a much higher dependence on imported fertilizers (see farmdoc daily, April 20, 2026). As a result, cropping decisions will become more complicated in Brazil (see farmdoc daily, April 10, 2026), potentially leading to acreage responses that will impact corn and soybean prices.

Events in the Middle East will likely cause another wave of general inflation, as higher energy prices tend to have widespread, economy-wide impacts. The FED appears to be preparing for such an event by announcing that interest rate hikes could occur in the future (see Timiraos). The first energy price crisis in the U.S. during the 1970s contributed to higher inflation throughout the 1970s, leading to the battle against inflation led by Paul Volcker in the early 1980s. Inflation rates of the magnitude of the 1970s should not be anticipated, but they can not be entirely ruled out either. In any case, higher farm input costs other than fertilizer should be anticipated for 2027 (see farmdoc Daily, April 30, 2025).

Summary

Higher fertilizer prices caused by the Iran Conflict will have impacts in 2026, particularly on farms that had not purchased as much of their nitrogen needs prior to March. Those farms will likely have much higher costs than those farms that pre-priced nitrogen. All farms will face the brunt of higher prices in 2027, leading to consideration of adjustments such as lowering application rates, switching to anhydrous ammonia, and moving applications to post-plant. Moreover, another round of inflation in all farm inputs should be anticipated.

References

Arita, S., M. Wang, J. Kim, R. Chakravorty and S. Steinbach. "Strait of Hormuz Disruption Scenarios and Fertilizer Purchasing Risks for U.S. Crop Producers." farmdoc daily (16):75, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 29, 2026.

Colussi, J. and M. Langemeier. "Middle East Conflict Revives Concerns Over Fertilizer Dependence in the U.S. and Brazil." farmdoc daily (16):68, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 20, 2026.

Mashange, G. and G. Gardner. "Middle East Ceasefire Fails to Ease U.S. Fertilizer Price Pressure on Farmers." farmdoc daily (16):72, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 24, 2026.

Monaco, H., J. Colussi, G. N. Schnitkey, N. Paulson, A. V. Lobo and J. A. Caregnato. "The Iran Conflict and Fertilizer Markets: Why Brazil Faces Greater Near-Term Risk than the U.S." farmdoc daily (16):62, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 10, 2026.

Paulson, N., G. Schnitkey, B. Zwilling and C. Zulauf. "Revised Illinois Crop Budgets for 2026." farmdoc daily (16):6, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, January 13, 2026.

Paulson, N., G. Schnitkey, C. Zulauf and L. Gentry. "High Fertilizer Prices Suggest Reconsidering Application Rates." farmdoc daily (16):54, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 31, 2026.

Paulson, N., G. Schnitkey, H. Monaco and C. Zulauf. "Nitrogen Prices Remain in Focus After Iran Conflict." farmdoc daily (16):49, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 24, 2026.

Schnitkey, G., C. Zulauf, K. Swanson, N. Paulson and J. Baltz. "PACE and Nitrogen Fertilizer Strategies for 2023." farmdoc daily (12):154, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, October 11, 2022.

Schnitkey, G., C. Zulauf, N. Paulson and J. Baltz. "The Iran Conflict: Potential Impacts on 2026 Corn and Soybean Returns." farmdoc daily (16):45, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 17, 2026.

Timiraos, N., “After Months of Debating Rate Cuts, Fed Shifts Toward Mapping Out Hikes.” Wall Street Journal. May 1, 2026. https://www.wsj.com/economy/central-banking/after-months-of-debating-rate-cuts-fed-shifts-toward-mapping-out-hikes-db850f74

Zulauf, C., G. Schnitkey, J. Coppess and N. Paulson. "Are US Crop Production Costs High?" farmdoc daily (15):81, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 30, 2025.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.